Michael Burry's latest dot-com warning is the headline. Crowding is the tradable issue. Momentum can stay expensive for longer than valuation skeptics expect, but the AI chip rally has stopped being only a demand story and has become a position-management story.

By Monday's close, the S&P 500 and Nasdaq were still at records even as Brent crude pushed above $104. That matters mainly as a trigger set: oil, CPI and yields can tighten valuation tolerance for a crowded growth trade even if semiconductor demand remains intact.

The Warning Is About Crowding, Not Prophecy

Burry's comparison with the final stage of the 1999 to 2000 bubble is useful as a stress test, not as a sell signal by itself. A bubble analogy can be directionally right and still be early, especially when the fundamental catalyst, AI infrastructure spending, continues to show up in revenue, memory pricing and data-center capex plans.

The cleaner evidence is positioning. JPMorgan positioning data cited by Bloomberg showed individual investors lifting technology purchases to the highest level in a year, with hardware companies posting their second-largest inflow on record. Retail participation is not automatically bearish. It becomes a risk when it arrives after the price move has already compressed the margin for disappointment.

Source: Bloomberg via Gulf Times, citing JPMorgan, Strategas, Newedge Wealth and Macro Risk Advisors. Figures are source-reported and not independently recalculated.

Semis Still Have a Real Earnings Case

A crowded trade is not the same as a broken trade. Recent chip leadership has been powered by more than Nvidia alone. Reuters market data showed Nvidia, Micron and SanDisk participating in the May hardware rebound, a useful sign that investors are treating AI as a broader data-center supply-chain cycle rather than a single-stock story.

Memory and storage strength matter because they tie the rally to server builds, HBM demand and capacity constraints, not only to GPU scarcity. A vertical chart alone is not enough to say the earnings cycle has broken. The bull case still has revision support, and a narrow but powerful leadership group can carry an index while the rest of the market waits for clearer macro data.

Multiple Compression Is the Real Risk

The vulnerability is not that one warning disproves AI demand. It is that a parabolic chart leaves less room for a higher discount rate, a slower revision cycle or a capex-margin scare. If the trade is already priced for perfection, unchanged fundamentals can still produce a lower stock price when the multiple investors are willing to pay falls.

Oil, CPI and yields are not the main story here. They are the most obvious trigger set. Higher crude can lift headline inflation risk, inflation expectations can keep Treasury yields firmer, and long-duration growth multiples can become less forgiving. In that setup, semiconductor earnings can remain strong while the stocks stop getting paid for every incremental AI headline.

Watch Which Failure Mode Appears First

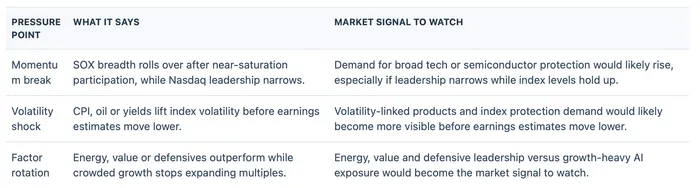

Crowding does not require an all-or-nothing bearish call. A more useful framework is to identify which part of the trade would weaken first: price momentum, volatility, factor exposure or end-demand breadth. Each path points to a different market signal, and none requires a deterministic view that chip stocks must fall immediately.

Those signals are a framework, not a recommendation. A macro yield shock is not the same as an Nvidia earnings miss, and a retail-flow unwind is not the same as a collapse in AI capex. Treating all three as one bearish semiconductor call would make the read less precise.

What Would Confirm or Break the Move

For the rally to keep working, semiconductor breadth needs to become less dependent on price momentum and more dependent on continued upward earnings revisions. Confirmation would look like strong order commentary, memory pricing power, data-center capex that remains funded, and yields that fail to extend after inflation data.

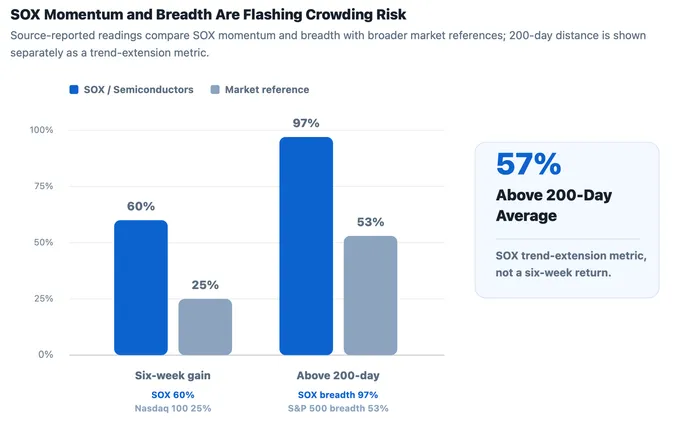

Failure would look more mechanical than dramatic. Breadth could slip from extreme levels, call demand could fade, and high-multiple chip winners could give back gains even without a negative AI headline. When a sector is reported to be 57% above its 200-day average and retail has arrived late, the next risk is not necessarily a collapse in AI demand. It is smaller but still tradable: fewer buyers willing to pay peak multiples for the same earnings story.