After nine consecutive weeks of gains, Wall Street finally hit a wall.

On Friday, the Nasdaq Composite plunged 4.2%, while the S&P 500 dropped 2.6%, marking their worst performances of the year. Semiconductor stocks led the decline, with AI-related names suffering particularly heavy losses. Nvidia fell more than 6%, Broadcom nearly 8%, while several other AI-linked chipmakers lost double-digit percentages in a single session. The PHLX Semiconductor Index (SOX) tumbled more than 10%, its worst day since the pandemic-era selloff in 2020.

The immediate trigger appeared obvious: a much stronger-than-expected U.S. jobs report. But beneath the surface, the selloff exposed a deeper tension that has been building for months—a market simultaneously driven by extraordinary AI optimism and increasingly vulnerable to higher interest rates.

The key question for investors is whether Friday's decline represents the beginning of a larger correction or merely a healthy reset within an ongoing bull market.

What Triggered the Selloff?

The catalyst was May's nonfarm payrolls report.

The U.S. economy added 172,000 jobs during the month, more than double consensus expectations. Unemployment remained at 4.3%, while wage growth stayed firm. Instead of confirming a cooling economy, the report suggested that economic activity remains resilient despite restrictive monetary policy.

For investors, that created a problem.

For most of 2026, markets had been pricing a relatively straightforward narrative: slower growth would eventually allow the Federal Reserve to cut rates. Friday's employment report challenged that assumption.

Treasury yields surged immediately after the release. The 10-year Treasury yield moved above 4.5%, while the two-year yield climbed to its highest level in roughly a year. Traders sharply increased expectations that the Fed could remain restrictive for longer and potentially raise rates again before year-end.

That shift matters enormously for growth stocks.

High-growth technology companies derive much of their valuation from earnings expected years into the future. When bond yields rise, the present value of those future cash flows declines. In other words, higher rates compress valuations—even if the underlying business outlook remains unchanged.

That dynamic explains why AI stocks became the epicenter of the selloff.

Why AI Stocks Were Hit the Hardest

The jobs report alone does not fully explain the magnitude of Friday's decline.

The AI trade entered June after an extraordinary rally. Market leadership had become increasingly concentrated in a relatively small group of semiconductor and AI infrastructure companies. Investor positioning was heavily skewed toward the same winners.

In that environment, the market was already vulnerable to disappointment.

Broadcom's earnings report provided an additional spark. While the company delivered strong results, its forward AI revenue guidance failed to satisfy the market's most optimistic expectations. Investors who had become accustomed to continuous upward revisions suddenly faced the possibility that AI demand growth may normalize from its recent breakneck pace.

The result was a classic crowded-trade unwind.

Nvidia, Broadcom, Micron, AMD, Marvell, Qualcomm, and ARM Holdings all came under intense pressure. The selloff quickly spread throughout the semiconductor ecosystem, erasing more than $1 trillion in market value across the sector.

Importantly, however, there was little evidence that the long-term AI investment cycle itself has fundamentally changed.

Instead, investors appeared to be reassessing how much they are willing to pay for future growth in a higher-rate environment.

Is This a Panic—or a Correction?

The distinction matters.

Historically, true market panics are characterized by systemic stress: liquidity dries up, credit markets deteriorate, and investors rush to exit nearly every risk asset simultaneously.

Friday's selloff looked different.

The most severe damage was concentrated in technology and semiconductor shares. Defensive sectors held up considerably better, suggesting investors were rotating rather than indiscriminately fleeing risk. Meanwhile, the underlying economic backdrop remains relatively healthy, with employment growth still positive and recession indicators largely subdued.

Several strategists have described the move as a valuation reset rather than a fundamental reassessment of the AI story. Reuters reported that multiple institutional investors viewed the decline as a momentum unwind following an exceptionally strong rally rather than the start of a structural collapse in AI demand.

That interpretation is important because markets often experience sharp pullbacks during powerful bull cycles.

Not every violent decline signals the end of a trend.

What History Suggests

Investors naturally look for historical parallels after a selloff of this magnitude.

Three episodes stand out.

The first is the AI-driven correction of 2024, when concerns about valuations and rising Treasury yields triggered a sharp but temporary pullback in technology shares. Markets eventually recovered and moved to new highs.

The second is the volatility shock of early 2018. Then, as now, strong economic data pushed bond yields higher and forced investors to rethink the path of monetary policy. Stocks experienced a sudden and painful correction but ultimately recovered as economic growth remained intact.

The third is the 2022 Jackson Hole selloff, when markets were forced to abandon expectations for imminent policy easing. That decline proved more damaging because the Federal Reserve continued tightening and economic growth slowed significantly.

At the moment, the current environment appears closer to the first two cases than the third.

The critical difference is that today's selloff is being driven by concerns about rates rather than evidence of recession.

Historically, corrections caused by higher yields during periods of solid economic growth have often proven less destructive than declines associated with deteriorating fundamentals.

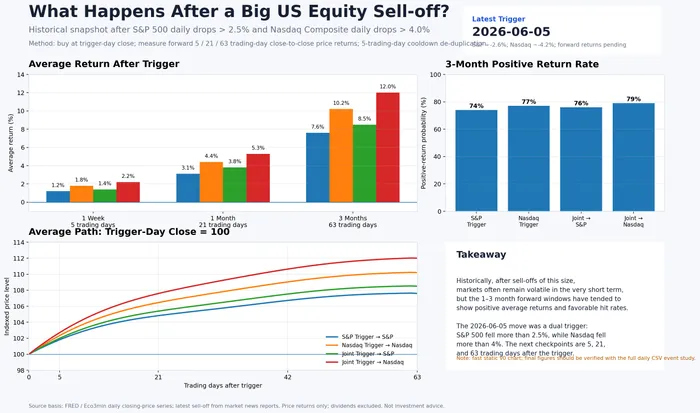

What Happens After a Selloff Like This?

Before assuming that Friday's decline marks the beginning of a larger downturn, it helps to examine how markets have behaved after similar one-day shocks in recent years.

The S&P 500 fell more than 2.5% in a single day

The Nasdaq Composite fell more than 4% in a single day

The past decade provides a useful testing ground, covering multiple market regimes—from the 2018 volatility shock and the pandemic crash to the 2022 rate-hiking cycle and the AI-driven rally of recent years.

While every selloff is unique, historical patterns can offer valuable context for investors trying to determine whether sharp declines have typically led to further losses—or created opportunities for recovery.

What Wall Street Is Watching Now

Going forward, investors should focus on three variables.

1. Treasury Yields

The most important question is whether Friday's move represents a temporary repricing or the beginning of a sustained rise in yields.

If the 10-year Treasury continues moving higher, valuation pressure on technology stocks could persist regardless of earnings strength.

2. Inflation Data

A strong labor market alone does not guarantee additional Fed tightening.

What matters is whether inflation begins accelerating again.

Upcoming CPI and PCE reports may ultimately determine whether Friday's selloff becomes a short-lived shock or the first stage of a deeper correction.

3. AI Capital Spending

Investors are increasingly scrutinizing whether massive AI infrastructure investments are translating into sustainable returns.

Any signs that enterprise demand is slowing could reinforce concerns that portions of the sector have become overextended.

For now, however, there is little evidence that major cloud providers or corporate customers are materially reducing AI spending plans.

The Bottom Line

Friday's selloff was undoubtedly painful. But the evidence so far suggests it was driven more by interest-rate repricing and crowded positioning than by a collapse in AI fundamentals.

The market suddenly realized that a stronger economy may not be entirely good news for stocks.

Higher growth can support corporate profits, but it can also delay monetary easing and push bond yields higher. For highly valued technology companies, that trade-off matters.

The coming weeks will determine whether investors view Friday as the start of a broader de-risking cycle or simply as a necessary correction after one of the strongest AI rallies in market history.

For now, the AI story appears bruised—but not broken.