A common market mistake is treating the latest MLCC price rebound as another smartphone-cycle call. AI servers and EVs are pulling the same capacitor supply chain toward higher-reliability parts, making the recovery more selective than a broad consumer electronics restock.

TrendForce's May 18 update said high-end demand and channel inventory building are pushing MLCC prices toward an upward turn, while its April 28 work described a split between robust AI-driven demand and soft consumer demand. Pricing power is returning where reliability, capacitance density and power stability matter, not across every consumer-grade part at once.

Price Recovery Is Forming, But Not Evenly

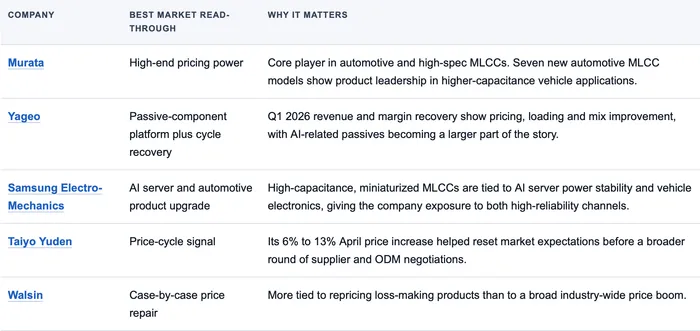

TrendForce reported that Taiyo Yuden raised prices for low-capacitance consumer and automotive MLCCs by 6% to 13% in April 2026. TrendForce also said Taiwan and mainland China agents began stocking X5R standard products even as actual ODM orders declined. Channel buying can tighten near-term availability, but it is not the same as ODMs lifting full-year end-demand assumptions.

YAGEO and Walsin were negotiating case-by-case adjustments for some loss-making products, without announcing broad price hikes. Supplier behavior therefore looks more like price-floor repair than a synchronized industry boom.

TrendForce also said the average decline in overall MLCC prices narrowed to less than 0.5%, the smallest in nearly three years. That is enough to change the pricing conversation, but it still leaves the recovery dependent on where capacity is being pulled.

That mix of price hikes, channel restocking and weak ODM orders is exactly why the rebound should be treated as selective pricing repair, not a full MLCC supercycle.

AI Servers Are Forcing A Better MLCC Mix

Samsung Electro-Mechanics' AI server MLCC materials point to the same market issue because higher GPU density is making power stability, noise suppression and board-space efficiency more valuable. Pricing implication is not just higher unit count. Higher-spec MLCCs can carry better pricing than commodity consumer capacitors when customers are buying stability and board efficiency.

A separate Samsung Electro-Mechanics note says power demand from AI servers and GPU modules is rising and that MLCC-centric architectures are expanding in AI server designs. Mix quality therefore improves when customers shift toward reliability and power architecture instead of low-end consumer unit volume.

TrendForce reported the matching supply signal on May 18. Japanese and Korean suppliers have been reallocating capacity from consumer-grade products toward high-end MLCCs for AI applications, which reduces the flexibility available to ordinary consumer electronics when channels try to rebuild inventory.

EVs Pull On The Same Reliability Capacity

Murata said on April 8 it began mass production of seven AEC-Q200-qualified automotive MLCCs with world-leading capacitance for their rated voltage and size. Those products target IC peripheral circuits in ADAS and autonomous-driving applications and medium-voltage in-vehicle power lines, tying the auto case to capacitance density, miniaturization and power-line stability.

Samsung Electro-Mechanics has also introduced ultra-high-voltage MLCCs for xEV high-voltage powertrains, including electric vehicle charging systems and 800V inverter systems. EVs add the market tension because vehicle electronics and AI servers both value reliability more than low-end consumer unit volume.

If high-end capacity is allocated to AI accelerators, ADAS and power electronics, ordinary consumer devices do not need to recover fully for top suppliers to gain better mix. Weak consumer demand still matters, but it no longer explains the whole price cycle.

Supplier Exposure Is Already Splitting

Company read-through is narrower than a generic MLCC basket. Product leadership, automotive qualification and AI server power exposure decide who benefits most from the mix shift.

High-End Mix Matters More Than A Full MLCC Supercycle

Bullish logic for MLCC suppliers is not simply more units. TrendForce's 6% to 13% Taiyo Yuden price signal and Yageo's 38.1% Q1 gross margin point to better mix, tighter high-end capacity, improving price discipline and customers that are less price-sensitive.

Failure conditions are equally clear. Channel restocking can outrun real ODM orders, consumer electronics can stay soft, and price increases may fail to broaden beyond selected products. YAGEO and Walsin's case-by-case approach is a useful warning against treating every capacitor category as tight.

The MLCC rebound is not about smartphones coming back in the old way. AI servers and EVs are turning a low-profile passive component into a higher-value supply-chain constraint, but confirmation still needs broader supplier negotiations, firmer ODM orders, sustained gross margin quality and more automotive or AI-server product ramps. The winners will not be every MLCC name. They will be the suppliers with high-end reliability capacity, automotive qualifications and real exposure to AI server power architecture.