U.S. stocks are entering the April CPI report with a contradiction that matters for the AI trade: record index levels, strong chip momentum and a renewed oil shock are all on the screen at once. The S&P 500 added 0.2% to its Friday record and the Nasdaq gained 0.1% to its own record on Monday, according to AP, even as investors prepared for a fresh inflation print.

Monday's move suggests the market is repricing AI-led equity leadership as durable enough to absorb higher oil, at least for now. The CPI print does not need to create a new AI bull case. It only needs to avoid breaking the one already working.

Record Highs Still Need a Yield Check

Record highs can make the setup look cleaner than it is. On May 11, stalled U.S.-Iran talks had lifted crude prices almost 3% and left investors focused on the next CPI release. That is not a side issue for a market whose leadership still depends heavily on long-duration growth stocks.

Technology and energy can both rise during the same session, but they tell different stories. Energy strength says headline inflation pressure has not gone away. Semiconductor strength says investors still believe AI capex, memory demand and earnings revisions can outrun that pressure. A market can hold both views for a while, but CPI will decide whether the combination remains stable.

For equity investors, the practical question is not whether oil is higher. It is whether higher oil stays a sector-specific cost shock or becomes a broader rates shock: higher headline CPI, possible inflation-expectation or core spillover, higher Treasury yields, and less tolerance for long-duration growth multiples.

CPI Is the Rate Check for the AI Trade

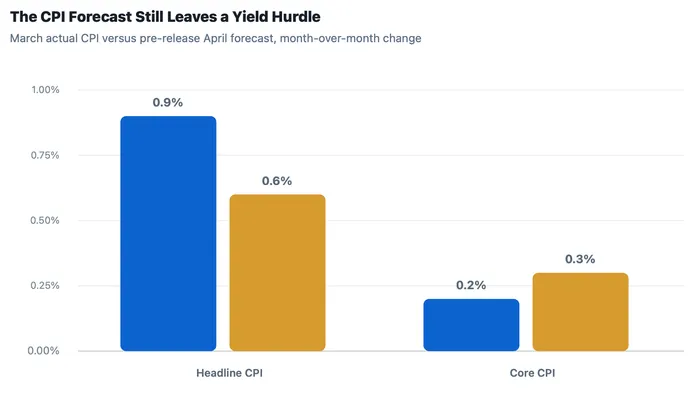

Official inflation data show why Tuesday's report has become a market checkpoint. The Bureau of Labor Statistics said March CPI rose 0.9% on a seasonally adjusted basis, while energy rose 10.9% and gasoline rose 21.2%. Core CPI increased a much milder 0.2%, which helped investors treat the move as an energy shock rather than a full inflation reset.

April expectations are still not soft. Kiplinger said headline CPI was expected to rise 0.6% month over month and 3.7% year over year, with core CPI forecast at 0.3% month over month and 2.7% year over year before the release. The BLS has scheduled the April release for 8:30 a.m. ET on May 12.

Source: BLS March CPI release for March actual CPI; Kiplinger April CPI preview for pre-release forecast values. Figures are monthly percentage changes; April values are forecasts, not actual results.

Even if headline CPI cools from March toward the 0.6% forecast, that would not be an easy all-clear. For AI and other high-multiple growth stocks, the cleaner signal would be a headline deceleration without a core pickup. A hot core number would challenge the idea that the oil shock is safely contained.

Oil Can Turn Rotation Into Multiple Compression

Higher oil can help energy stocks, but it also taxes consumers, transport margins and rate-sensitive valuations. AP said the 10-year Treasury yield rose to 4.40% from 4.38% late Friday, while Nvidia and Micron were among the strongest forces lifting the S&P 500. That split is exactly what makes the CPI print important.

Retail and transport pressure matter because they show where the energy shock can move from commodity screens into earnings assumptions. If gasoline and shipping costs keep lifting inflation expectations, consumer-facing equities may remain the first place investors cut exposure. The index can still rise if chip leadership is strong enough, but breadth becomes more fragile.

A sector rotation is not automatically bearish. Energy can offset some technology duration risk when oil rises. The problem starts when oil lifts yields, squeezes consumption and narrows the market in the same window. That would leave the AI trade carrying more of the index with less help from cyclicals and consumers.

Semiconductor Breadth Still Carries the Tape

Semiconductor leadership is why the market has been able to look past the oil problem so far. On Friday, Nvidia rose 1.8%, while Micron and SanDisk each rose more than 15%, according to Reuters. Reuters also reported that the Philadelphia semiconductor index had lifted its gain so far in the second quarter to 55%, an unusually large figure that should be read as a source-reported momentum signal rather than a fresh independent calculation.

Memory and storage strength matters because it shows the AI trade has broadened beyond Nvidia into the data-center supply chain. AI infrastructure demand, memory pricing and chip earnings revisions are still providing concrete support instead of only narrative heat. For investors, that means the CPI report does not need to create a new AI bull case. It only needs to avoid breaking the one already working.

Crowding is the vulnerability. When a leadership group has already run hard, a yield shock does not need to disprove AI demand to trigger profit-taking. It only has to reduce the valuation investors are willing to pay for the same earnings story.

After the Print, Watch Yields and Breadth

The immediate test after CPI is the Treasury market. A benign path would show headline inflation cooling from March, core inflation staying controlled and the 10-year yield failing to extend its move. That would let the market keep treating oil as a rotation variable rather than a broad risk-off trigger.

A harder path would look different: CPI comes in hot, yields rise, consumer and rate-sensitive shares keep lagging, and semiconductor gains become more isolated. That scenario would not mean the AI demand story is false. It would mean the market has to discount that story at a less generous multiple.

If CPI stays contained and yields fail to extend, AI leadership can keep carrying the index. If oil pressure leaks into core inflation or inflation expectations, investors do not have to abandon the AI story. They only have to discount it at a less generous multiple.