Akamai Technologies turned into one of Friday's sharpest AI infrastructure trades after a $1.8 billion, seven-year cloud commitment from an unnamed U.S. frontier-model provider made investors rethink AKAM as more than a mature content-delivery and security stock.

Barron's reported AKAM rose 27% to $147.78, its highest level in 26 years, while the S&P 500 and Nasdaq closed at records after a stronger-than-expected April jobs report. The stock move still looked company-specific because the contract changed the market's view of Akamai's cloud strategy more than the quarterly beat did.

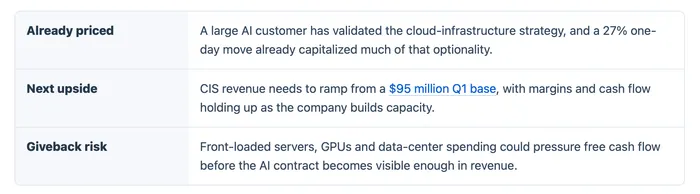

AKAM is no longer cheap AI optionality after that move. Further upside depends less on the headline contract size and more on whether Cloud Infrastructure Services revenue begins to show contract conversion without a deeper free-cash-flow hit.

The market is pricing AKAM like a validated AI infrastructure winner before the contract has fully shown up in reported revenue. That is the tension now: valuation moved first, and the financial proof still has to follow.

The deal changed Akamai's market category, but it also raised the hurdle

Management said the frontier-model provider committed $1.8 billion over seven years for Cloud Infrastructure Services. Spread evenly, that would be roughly $257 million a year, compared with Q1 CIS revenue of $95 million, or about $380 million annualized.

That rough comparison is why the contract mattered. If the revenue comes through cleanly, the commitment could equal roughly two-thirds of the current CIS annualized run rate. If recognition is slower, back-end loaded, or tied to heavy infrastructure spending, the stock may have moved faster than the financial model.

Quarterly earnings alone would not have forced the same move. Investing.com reported adjusted EPS of $1.61 against a $1.60 consensus and revenue of about $1.07 billion in line with estimates. The repricing came from the size and duration of the AI commitment, not from a conventional earnings surprise.

That distinction changes the trade. AKAM is now being judged on contract conversion and infrastructure economics, so the next report has to show more than another headline customer.

Capex and free cash flow are now the second side of the trade

AI demand validation is only half the story. The other half is whether the servers, GPUs and data-center commitments needed to serve that demand arrive before enough revenue does.

Investing.com cited Raymond James as estimating that the new deal could add around $800 million to Akamai's total capex over the next four quarters, including about $100 million in 2027, and could push FY2026 free cash flow negative.

Akamai has a better balance-sheet starting point than many smaller AI infrastructure companies. The Q1 release showed $313 million of operating cash flow, $1.733 billion of cash, cash equivalents and marketable securities, and $206 million of repurchases during the quarter. Still, the market is now asking whether AI infrastructure can become accretive quickly enough to offset the upfront investment cycle.

CIS growth is the signal, but the base is still small

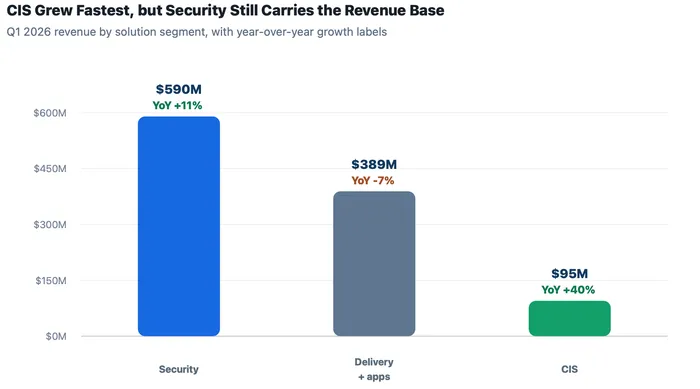

Akamai's own segment data show why the market reaction was powerful but not risk-free. Cloud Infrastructure Services revenue was $95 million in Q1, up 40% year over year, far faster than the rest of the company. Security revenue was much larger at $590 million and grew 11%, while delivery and other cloud applications revenue fell 7% to $389 million.

Viewed that way, CIS is the growth outlier inside Akamai, but it is not yet the earnings center of gravity. The new AI contract can change the mix over time if it ramps cleanly, but current reported revenue still leaves security carrying most of the scale.

Source: Akamai Q1 2026 financial release

The chart supports the core market question. Investors are not simply rewarding a better quarter; they are paying for the possibility that the fastest-growing segment can become large enough to alter Akamai's whole profile.

Security keeps this from becoming a pure compute trade

Akamai's advantage is not only that it can host AI workloads. The company pairs cloud infrastructure with a security franchise that still produced $590 million of Q1 revenue, more than six times CIS revenue. That mix gives the AI story a second route: model providers and enterprises may need both distributed compute and protection for the APIs, applications and data flows around AI systems.

Recent disclosures support that direction. In March, Akamai described a separate $200 million, four-year AI cluster service agreement involving a multi-thousand NVIDIA Blackwell GPU cluster and other cloud infrastructure services. The new $1.8 billion commitment is larger, but the earlier deal showed that the company had already begun turning its distributed-cloud pitch into customer contracts.

Legacy delivery remains the offset. Delivery and other cloud applications revenue fell 7% year over year in Q1, so Akamai cannot rely on all segments moving together. A cleaner bull case requires CIS to keep accelerating while security stays durable enough to fund the transition.

The next test is conversion, not another headline

Guidance gives investors the first checkpoint. Akamai projected Q2 revenue of $1.075 billion to $1.100 billion and full-year revenue of $4.445 billion to $4.550 billion, with non-GAAP operating margin at about 26% for the year. Those ranges do not yet imply a sudden company-wide growth breakout, which is why the revenue ramp from the AI commitment matters more than the announcement itself.

Useful confirmation would look specific: CIS revenue growing from the $95 million Q1 base, management narrowing the timing of AI contract recognition, non-GAAP margins holding near guidance, and capex not overwhelming operating cash flow for longer than investors expect. Weak confirmation would be a delay in customer ramp, further delivery erosion, or a clearer free-cash-flow drag without enough revenue visibility.

Friday's reaction says the market is willing to underwrite Akamai as an AI infrastructure option. From here, the stock has to earn that category change with conversion metrics, not just contract size. After a 27% move, AKAM no longer needs another AI headline. It needs evidence that the AI contract can move reported CIS revenue faster than capex moves cash flow lower.