Advanced Micro Devices (AMD) delivered exactly the type of earnings report investors were hoping for — and arguably more. The company not only beat Wall Street expectations across nearly every major metric, but management also delivered an aggressively bullish tone around AI demand, server CPU growth, and long-term data center opportunity. Investors responded by sending the stock sharply higher, with shares breaking out from roughly $355 ahead of earnings to nearly $420 in early trading following the release. That move reflected more than just a quarterly beat. The market viewed the report as confirmation that AMD is becoming a legitimate second force in AI infrastructure behind NVIDIA Corporation (NVDA), with demand trends accelerating instead of slowing despite concerns the AI trade had become overcrowded.

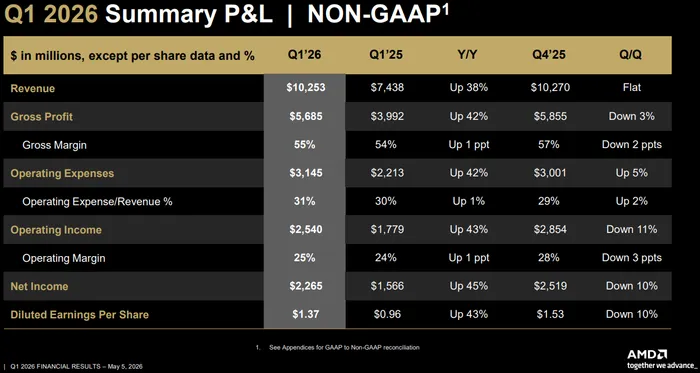

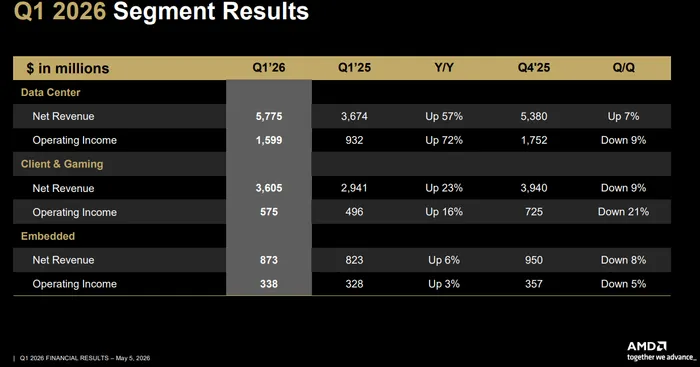

AMD reported first-quarter adjusted earnings per share of $1.37, comfortably above consensus expectations of roughly $1.29. Revenue came in at $10.25 billion versus expectations around $9.9 billion, representing 38% year-over-year growth. The most important number, however, was once again data center revenue. AMD’s data center segment generated $5.78 billion in sales, up 57% year-over-year and ahead of analyst expectations near $5.6 billion. Investors have increasingly treated AMD as an AI infrastructure company rather than a traditional semiconductor stock, and the quarter reinforced that shift. CEO Lisa Su repeatedly emphasized on the conference call that AI infrastructure is now the “primary driver” of both revenue and earnings growth.

The guidance was arguably the biggest driver behind the breakout in the stock. AMD projected second-quarter revenue of approximately $11.2 billion at the midpoint, well ahead of consensus expectations near $10.5 billion. The guide implies roughly 46% year-over-year growth and sequential growth of about 9%, which is impressive considering the company is already operating from a much larger revenue base than it was just a year ago. Gross margin guidance also came in ahead of expectations at roughly 56%, signaling that AI accelerator and server CPU mix continue improving profitability despite ongoing investment spending. Investors had worried the AI buildout cycle could begin slowing after multiple quarters of hyperscaler spending, but AMD’s outlook suggested the opposite is occurring.

The market also reacted strongly to management’s commentary around server CPU demand and the expanding AI opportunity. Lisa Su said AMD now expects the server CPU total addressable market to grow more than 35% annually, reaching over $120 billion by 2030. That was a substantial increase from prior expectations and reflected growing demand tied to inferencing and agentic AI workloads. Su explained that AI systems require far more CPU orchestration, data movement, and workload management than previously anticipated, creating a major tailwind for AMD’s EPYC processors. The company now expects server CPU revenue growth to exceed 70% year-over-year during the second quarter, a remarkable acceleration that investors clearly were not fully pricing in ahead of earnings.

AMD’s product roadmap and deployment timelines were another major source of optimism. Investors have been watching closely to see whether AMD could successfully scale production and meet delivery commitments tied to major AI contracts. Management said shipments tied to its Meta and OpenAI agreements remain on track to begin in the second half of the year, helping calm fears that deployment schedules could slip. Lisa Su highlighted strengthening customer engagement surrounding the MI450 GPU architecture and the Helios platform, noting that customer forecasts are now exceeding AMD’s original expectations. She also discussed “multi-gigawatt opportunities” tied to AI infrastructure buildouts, reinforcing the idea that hyperscaler demand remains extremely strong despite already enormous capital expenditure plans from companies like Meta Platforms (META), Alphabet Inc. (GOOGL), Microsoft Corporation (MSFT), and Amazon.com, Inc. (AMZN).

One of the most important takeaways from the call was management’s confidence around supply and capacity expansion. Investors have worried for several quarters that AMD could struggle to scale quickly enough to meet AI demand, particularly given ongoing tightness across advanced packaging and high-bandwidth memory markets. Lisa Su acknowledged that supply chains remain tight and data center buildouts continue facing infrastructure bottlenecks, but she repeatedly stressed that AMD is working closely with manufacturing and supply chain partners to meaningfully increase wafer and back-end capacity. Importantly, management stated that it has secured enough memory supply to meet and exceed current targets, helping alleviate one of the biggest investor concerns heading into the report.

While data center dominated the story, AMD also posted solid results in its other businesses. Client and Gaming revenue rose 23% year-over-year to $3.6 billion, with client revenue climbing 26% thanks to continued strength in PC demand and Radeon GPU sales. Embedded revenue grew 6% to $873 million. Those segments were not the primary reason investors bought the stock aggressively following earnings, but they helped reinforce the idea that AMD’s business strength extends beyond AI accelerators alone. Still, management did strike a somewhat more cautious tone around the second half of the year for consumer-related businesses, noting that gaming revenue could decline more than 20% sequentially due to higher memory and component costs as well as a softer macro backdrop.

The tone on the conference call was overwhelmingly bullish and expansionary. Lisa Su repeatedly used phrases such as “strong and increasing confidence,” “accelerating demand,” and “meaningful acceleration,” which helped reinforce investor confidence that AMD is still in the early innings of its AI growth cycle. Analysts did push management aggressively on areas including OpEx growth, margin trajectory, and AI GPU sequencing, particularly around China-related disruptions and supply constraints. But management largely handled those questions confidently, reiterating that the company has strong visibility into long-term demand and capacity planning. Investors appeared willing to overlook concerns around slightly elevated operating expenses because revenue growth and AI momentum were simply too strong.

The broader takeaway from AMD’s earnings is that the AI infrastructure spending boom remains very real and may actually be accelerating. Investors were worried that expectations for the semiconductor sector had become impossibly high after a massive rally across AI names. Instead, AMD delivered a report that not only justified the stock’s prior gains but may have fundamentally expanded perceptions around the company’s long-term earnings power. The combination of stronger-than-expected data center growth, accelerating server CPU demand, bullish AI guidance, increasing customer commitments, and improving capacity visibility created exactly the type of “beat-and-raise” quarter growth investors were looking for. The only real question now is valuation, as the stock’s enormous rally means expectations heading into the next several quarters will become even more demanding.