On May 5, 2026, AMD's blockbuster Q1 earnings and upgraded guidance crushed estimates, igniting a spectacular 16.54% after-hours stock surge. The defining takeaway extends beyond the financial beat: the AI hardware narrative is fundamentally shifting. Driven by agentic AI and inferencing workloads, the CPU's critical role is rapidly ascending, triggering a structural re-rating of AMD's core value.

Beyond the Beat: Data Center Assumes the Growth Engine Mantle

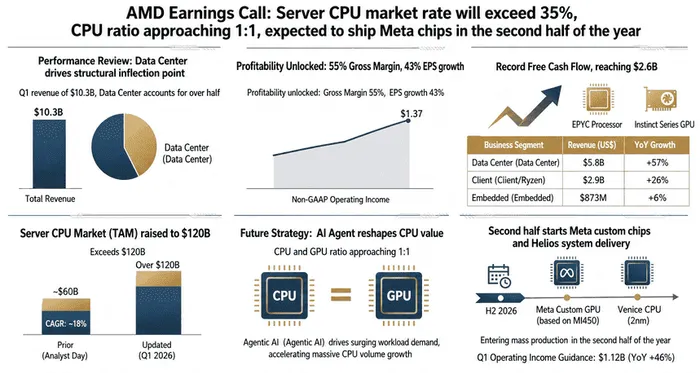

AMD's stellar Q1 performance was defined by both scale expansion and profitability improvements. The company generated $10.25 billion in total sales, representing a 38% year-over-year increase, while non-GAAP gross margins expanded to 55%. Furthermore, non-GAAP operating income reached $2.54 billion, demonstrating that the revenue growth is yielding tangible margin leverage rather than relying on price-cutting strategies.

The structural transformation of AMD's business model is now complete, with the Data Center segment emerging as the indisputable primary engine. Data center revenues climbed 57% year-over-year to $5.77 billion, accounting for more than half of the total top line. More importantly, this division generated $1.59 billion in operating profit, serving as the most lucrative profit pool for the enterprise. The quality of these earnings is validated by a record free cash flow generation of $2.56 billion. This robust cash conversion metric signals to the market that the aggressive capital expenditures required for AI development are not eroding the company's fundamental cash-generation capabilities. While the client business also saw a solid 26% growth to $2.88 billion driven by Ryzen processor demand, the gaming segment faced headwinds, with revenue dropping to $720 million, hampered by lower semi-custom sales. Consequently, the core growth narrative has officially pivoted away from the cyclical recovery of the personal computer market and anchored itself firmly in data center AI infrastructure.

The Anatomy of a 16.54% Rally: Short-Term Catalysts Meet Medium-Term Re-rating

The massive after-hours equity rally was fueled by a confluence of immediate financial catalysts and a broader strategic re-rating. On the short-term front, the Q2 revenue guidance provided the necessary fuel for multiple expansion. By projecting second-quarter sales of $11.2 billion, AMD implies a 46% year-over-year and 9% sequential growth rate. This robust outlook comfortably exceeded the $10.5 billion consensus estimate compiled by Bloomberg, providing institutional investors with the strong order visibility required to justify bidding up the stock.

From a medium-term perspective, a profound valuation re-rating is underway as management elevates the CPU narrative to a higher structural plateau. CEO Lisa Su clearly articulated that the proliferation of inferencing and agentic AI is creating unprecedented demand for high-performance CPUs alongside traditional accelerators. Previously, market participants harbored concerns that AI GPU demand might represent a transient cyclical peak. However, AMD showcased expanding customer visibility and deepening partnerships with hyperscalers, including Meta, Amazon Web Services (AWS), Google Cloud, and Microsoft Azure. Notably, Meta plans to deploy up to 6 gigawatts of AMD Instinct GPUs, including custom silicon based on the upcoming MI450 architecture scheduled for volume production in the second half of 2026. This multi-cloud, multi-region adoption curve convinces the market that AMD is entering a protracted, durable AI deployment cycle rather than experiencing a one-off revenue spike.

The Architecture Shift: Can the CPU AI Narrative Sustain Its Momentum?

The sustainability of AMD's current market momentum relies heavily on the evolving architectural demands of next-generation AI workloads. During the earnings call, management aggressively revised its total addressable market (TAM) projections. According to Ainvest analysis, AMD now expects the data center CPU market to grow at an annual rate exceeding 35%, reaching over $120 billion by 2030. This represents a dramatic doubling of the 18% compound annual growth rate forecast provided just months prior at the November analyst day.

This upward revision is driven by concrete technological necessities. While GPUs dominate the initial training phases of large language models, the subsequent deployment of inferencing and complex agentic AI workflows requires massive CPU compute for task orchestration, data movement, and parallel execution. Consequently, the hardware topology within modern data centers is shifting. The historical CPU-to-GPU deployment ratio, once resting at 1:8 or 1:4, is rapidly compressing toward a 1:1 parity in high-density AI environments. This structural evolution is already materializing in order books, with AMD anticipating its server CPU revenue to grow more than 70% year-over-year in the current quarter, a trajectory expected to persist into 2027. Concurrently, the company is actively collaborating with supply chain partners to meaningfully increase wafer and back-end capacity, confirming that these demand signals have transitioned from theoretical models to actual manufacturing orders. To maintain its competitive edge against ARM-based alternatives, AMD is also advancing its product matrix, heavily promoting its upcoming 6th Gen EPYC "Venice" CPUs built on a 2-nanometer process.

Conclusion

In summary, AMD's blockbuster Q1 report validates a critical paradigm shift: the CPU is reclaiming its indispensable status within the AI data center architecture. While the long-term infrastructure investment logic appears incredibly robust, investors must remain vigilant regarding executional and macroeconomic risks. Sustaining this premium valuation requires flawless commercialization of the MI450 and Helios systems later this year. Furthermore, management cautioned that memory shortages and component cost inflation will likely pressure PC shipment volumes in the second half of the year, potentially creating a margin headwind in the client segment despite the prevailing data center strength.