Apollo Global Management and Blackstone are working to bring in additional investors for about $36 billion of debt financing tied to Anthropic's AI infrastructure.The reported package puts the Claude maker's compute demand into a credit-market structure just as Anthropic is raising equity and signing larger cloud-capacity commitments.

A plain equity story would be simpler. This one is more revealing because the money would buy Google custom chips that Anthropic leases, while Broadcom is reported to provide payment support on the largest portions of the transaction. The financing read therefore turns on ownership, lease cash flows and residual-value protection rather than only on whether Anthropic can get more TPUs.

Debt mechanics matter more than the chip headline

The reported debt would buy Google tensor processing units that Anthropic would then lease. Apollo and Blackstone plan to sell down part of the debt while retaining significant portions, and the report said orders were being sought this week with a possible close next week. Those details keep the story conditional because discussions are ongoing and terms can still change.

A separate Investing.com summary citing Bloomberg News described a special-purpose vehicle, gradual drawdowns as chips become available, and roughly $31 billion of senior debt tranches with Broadcom residual-value support. That is the core market distinction. Anthropic would use the compute, Google supplies the TPU ecosystem, Broadcom helps make the chips and supports the senior debt, and private-credit buyers fund the asset before the end customer turns compute into cash flow.

Anthropic's new equity puts fixed payments beside a richer valuation

Anthropic said on May 28 that it raised $65 billion in Series H funding at a $965 billion post-money valuation, and the company said run-rate revenue had crossed $47 billion earlier in the month. That equity round is a vote on Claude demand, but the reported debt package adds a different burden because leases and debt service have to be matched by durable usage.

The company's compute commitments show why the credit channel is becoming relevant. Anthropic said the Series H would help expand compute, and it listed agreements with Amazon for up to five gigawatts of new capacity, with Google and Broadcom for multiple gigawatts of next-generation TPU capacity starting in 2027, and with SpaceX for GPU capacity. The valuation is richer, but capacity access is also turning into a larger fixed-cost problem.

Private credit gets the clearest public-market read

For public equities, the reported transaction is not automatically an Alphabet or Broadcom earnings number. Alphabet's role is TPU and cloud capacity, while Anthropic's earlier Google Cloud expansion targeted up to one million TPUs and well over one gigawatt of capacity in 2026. Broadcom's role is more direct to the Google TPU supply chain, yet the report's payment-support detail means credit exposure and chip economics are intertwined.

Apollo and Blackstone get the more immediate credit-market signal because a successful sale of the debt would show institutional demand for AI compute collateral. Alphabet and Broadcom still need evidence on chip delivery timing, margins, cloud consumption and the terms of any support agreement before the debt report can be translated into revenue or profit with confidence.

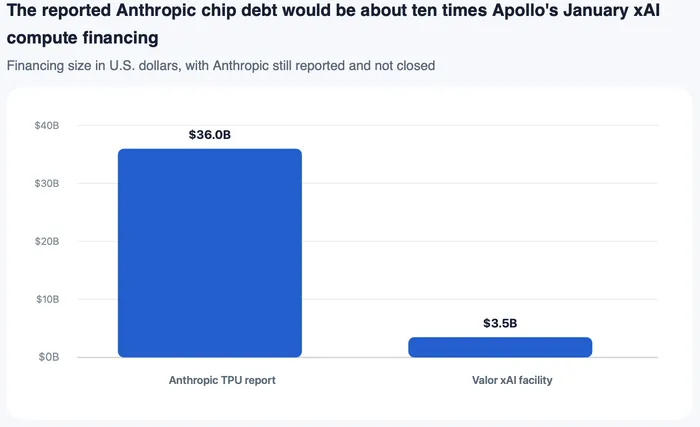

Apollo's January xAI deal gives the yardstick

Apollo already has a smaller public precedent in AI compute finance. In January, Apollo announced a $3.5 billion capital solution for Valor's $5.4 billion acquisition and lease of compute infrastructure, including Nvidia GB200 GPUs, to an xAI subsidiary. That transaction used a triple-net lease structure and gave Apollo a template for asset-based AI infrastructure credit.

Sources are the Reuters debt report and Apollo's official release.

A $3.5 billion capital solution could be treated as a specialized private-credit transaction; a roughly $36 billion package would move chip financing closer to a repeatable funding channel for AI labs, provided debt buyers accept the lease payment stream, hardware depreciation risk and backstop terms.

Orders, pricing and backstop terms decide the financing read

Near-term confirmation is concrete. The next disclosures or reports that matter are order-book demand, final pricing, how much Apollo and Blackstone retain, whether Broadcom's support covers the senior pieces as reported, and whether lease start dates line up with chip availability. Without those terms, the deal remains a high-profile financing attempt rather than a closed template for AI infrastructure debt.

Failure would not require a collapse in Anthropic demand. Soft syndication, wider debt spreads, weaker residual-value language or delayed TPU delivery would be enough to keep the read-through narrow. A close near reported terms would send a different message, showing that frontier AI compute can be financed through asset-backed private credit even when equity valuations are already near the trillion-dollar mark.