Arm Holdings plc shares are setting up for a pivotal session after the company delivered another strong quarter but exposed a new risk that investors are increasingly beginning to focus on across the semiconductor space: supply chain execution. The stock initially surged roughly 10% in after-hours trading following the report as investors cheered better-than-expected earnings, strong licensing growth, and bullish commentary surrounding demand for the company’s new Arm AGI CPU platform. However, the rally quickly reversed after management acknowledged that the company currently lacks sufficient supply capacity to meet surging customer demand. Shares have since slipped back toward the $220 area in premarket trading, which traders are closely watching as a key gamma flip zone that could determine whether momentum buyers step back in or whether the stock enters a more meaningful consolidation phase after its enormous run higher.

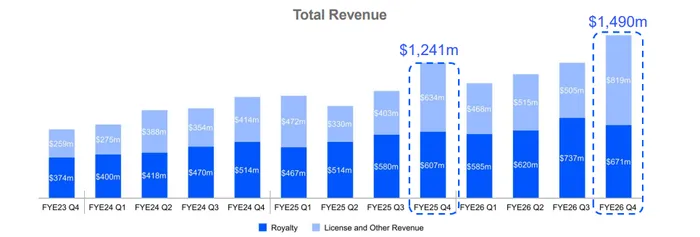

On the surface , the quarter itself was solid. Arm reported adjusted earnings per share of 60 cents, ahead of consensus expectations for 58 cents, while revenue climbed 20% year-over-year to a record $1.49 billion, slightly above analyst estimates of $1.47 billion. The company also guided fiscal first-quarter revenue to approximately $1.26 billion at the midpoint, modestly ahead of expectations, while projected earnings per share of roughly 40 cents also came in above Wall Street forecasts. For a stock that had already rallied aggressively into the print following strong semiconductor earnings from names like Advanced Micro Devices (AMD), the results were good enough to initially fuel another breakout higher.

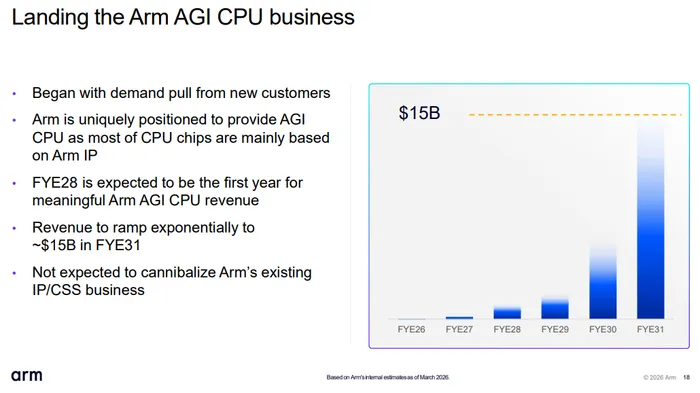

The real excitement centered around Arm’s growing push into AI infrastructure and data center CPUs. Management said customer demand for the company’s Arm AGI CPU platform has now surpassed $2 billion across fiscal 2027 and fiscal 2028, more than double what the company projected just six weeks ago during its Arm Everywhere event. CEO Rene Haas described an environment where customers are increasingly asking how quickly Arm can deploy units, with hyperscalers, AI infrastructure providers, and enterprise customers rapidly adopting Arm-based compute platforms as AI workloads scale globally.

That demand story is critical because Arm is no longer simply licensing chip architectures and collecting royalties. The company is now aggressively expanding into designing and selling its own silicon solutions, marking a major strategic shift for the business. Arm’s AGI CPU is designed specifically for massive AI data center workloads, where efficiency, power consumption, and scalability are becoming increasingly important as companies deploy large-scale agentic AI systems. Management believes AI data centers could require more than four times today’s CPU capacity by the end of the decade, creating what it estimates could become a $100 billion-plus market opportunity.

Importantly, Arm’s data center momentum appears very real. Management highlighted that data center royalty revenue more than doubled year-over-year during the quarter, driven by accelerating deployment of Arm-based server chips from major hyperscalers including Amazon Web Services, Google, and Microsoft. Arm-based CPUs are increasingly being paired alongside AI accelerators from companies like NVIDIA Corporation (NVDA), while custom silicon initiatives such as Google Axion, AWS Graviton, and Microsoft Cobalt continue gaining traction. Arm management went as far as saying they believe Arm architectures could eventually become the dominant CPU platform in data centers by the end of the decade.

The company’s licensing segment was particularly strong during the quarter. Licensing and other revenue rose 29% year-over-year to $819 million, easily topping analyst estimates near $774 million. Management attributed the upside to strong demand for next-generation compute architectures, cloud AI infrastructure, and deeper strategic partnerships with customers. Arm also signed new next-generation compute subsystem agreements tied to smartphones and data center networking chips, while annualized contract value growth remained strong at 22%.

However, royalty revenue was a relative soft spot and likely one reason investors became cautious following the call. Royalty revenue increased 11% year-over-year to $671 million, but still missed analyst expectations near $697 million. Management acknowledged weakness in the smartphone market, particularly in lower-end devices, while memory shortages and pricing pressures also impacted shipments. Investors were particularly focused on the idea that even though demand for AI infrastructure remains extremely strong, Arm still remains exposed to broader consumer electronics cycles through its royalty business.

Margins also came under some pressure as the company ramps investment spending tied to its silicon ambitions. Adjusted operating margins declined from 53% last year to roughly 49% this quarter, while operating expenses rose 30% year-over-year due to aggressive research and development investment. Management made clear that operating expense growth will continue rising sequentially throughout the year as the company builds out supply chain infrastructure and engineering capacity around the AGI CPU initiative.

That brings investors to what is now the central debate around the stock: execution risk. The semiconductor industry has increasingly become a story of who can actually secure enough packaging, wafers, memory, testing capacity, and advanced manufacturing supply to capitalize on AI demand. Arm essentially admitted during the conference call that supply constraints are currently preventing the company from fully monetizing demand. Haas stated the company is “working around the clock” to secure sufficient wafers, packaging, memory, and test equipment capacity to support future growth.

For investors, that creates both enormous opportunity and substantial risk. Demand appears far stronger than originally expected, reinforcing the idea that Arm is rapidly becoming one of the most important CPU platforms in AI infrastructure. However, the company is entering a far more operationally complex business by selling complete silicon solutions rather than simply licensing IP. That means investors will increasingly scrutinize execution, manufacturing relationships, supply procurement, margin structure, and delivery timelines — areas that historically were not major concerns for Arm’s business model.

Moving forward, investors will likely focus on several key areas. First, can Arm actually secure enough supply chain capacity to support the rapidly growing AGI CPU demand pipeline? Second, can royalty revenue growth reaccelerate despite ongoing smartphone weakness? Third, will data center revenue continue offsetting softness in traditional mobile markets? And finally, can margins stabilize as the company scales its silicon ambitions?

For now, the AI demand story remains firmly intact. But after an enormous rally and a valuation approaching 95 times forward earnings, the market is signaling that simply having demand is no longer enough. Investors now want proof that Arm can execute operationally in one of the most competitive and supply-constrained environments the semiconductor industry has seen in years.