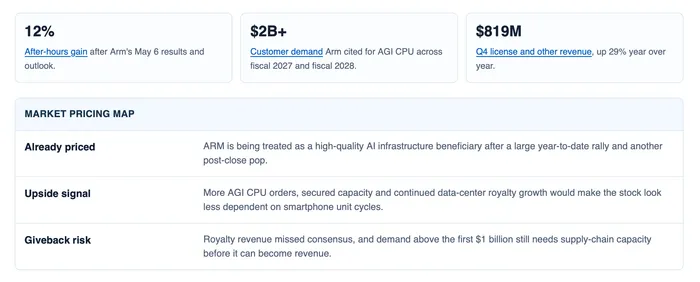

Arm Holdings shares jumped 12% in after-hours trading on May 6 after the company gave a slightly better-than-expected near-term revenue forecast and put a larger number on demand for its first data-center CPU. The move followed a regular-session chip rally, but the important signal was narrower: investors treated Arm as a bigger participant in AI infrastructure economics.

Before the report, ARM already carried a heavy AI premium. The shares had climbed more than 91% this year as of Tuesday's close, leaving little room for an ordinary earnings beat. What changed after the close was the mix: licensing beat expectations, data-center royalties accelerated, and the AGI CPU demand figure became large enough to matter against Arm's current revenue base.

Arm is being valued on a data-center option

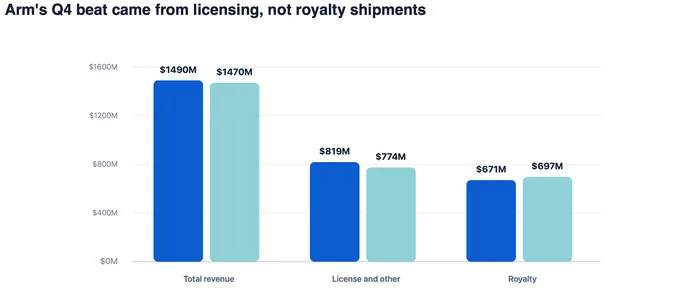

Q4 revenue of $1.49 billion was up 20% year over year, while full-year revenue reached $4.92 billion. Those numbers are strong, but they do not fully explain a double-digit after-hours move in a stock that had already rerated sharply.

Investor attention moved to the new revenue path. Arm said the AGI CPU has more than $2 billion of customer demand across fiscal 2027 and fiscal 2028, more than double the figure discussed at its March Arm Everywhere event. That gives the market a specific way to model Arm's move from architecture licensing into purpose-built silicon for agentic AI workloads.

For the stock, the distinction matters. A pure IP-royalty story depends heavily on customers shipping more chips and paying higher rates. A silicon-linked data-center story can pull forward larger licensing payments, improve visibility into hyperscaler demand, and create a broader read-through to server CPU share. The trade is now testing whether that optionality deserves to sit on top of the existing royalty model.

The revenue mix keeps the rally from being clean

Arm's Q4 beat was not uniform. Revenue beat LSEG estimates, and licensing and other revenue came in above expectations. Royalty revenue, however, landed below the consensus number cited in the same market report.

Source scope: stitched actual and consensus sources. Arm Q4 FYE26 investor presentation provides actual revenue by stream; Reuters via Investing.com provides LSEG estimates. Figures are in millions of dollars, Q4 FYE26, reported May 6, 2026.

That split is why the rally needs discipline. A licensing beat can signal big design commitments and future platform value, but it can also be lumpy. Royalty revenue is the recurring proof that customer chips are shipping at scale. ARM's current valuation is therefore asking investors to accept a near-term royalty miss because the data-center pipeline looks more valuable.

AGI CPU demand changes the competitive read-through

Arm's new CPU matters because it moves the company closer to the spending line item that investors already watch at Nvidia, AMD, Intel and the cloud providers. The AGI CPU was co-developed with Meta, and Arm said systems are available to order from ASRock, Lenovo, Quanta and Supermicro.

That does not make Arm a direct substitute for GPU suppliers. Agentic AI workloads still require accelerators, networking, memory and power infrastructure. The shift is more specific: as inference and autonomous workloads grow, cloud operators need efficient host CPUs and orchestration layers around accelerators. Arm is trying to capture more value from that layer.

For AMD and Intel, the implication is mixed. A larger server CPU market validates their own AI-inference arguments, but Arm's push into production silicon also raises the risk that cloud customers use Arm-based designs to pressure x86 incumbents. For Nvidia, the read-through is less about displacement and more about whether Arm-based CPUs become standard companions in accelerator systems.

Hyperscaler adoption makes smartphone drag less dominant

Arm still has a large smartphone royalty base, and that base is not free from pressure. The same Reuters report noted memory-chip shortages as a strain on consumer electronics demand, a risk for royalty revenue when device units soften.

Data-center adoption gives the stock a counterweight. Arm said data-center royalties more than doubled year over year and said its CPU compute share among top hyperscalers is about 50%. It also pointed to Google Axion, Nvidia Vera, Microsoft Cobalt and AWS Graviton as evidence that Arm-based CPUs are moving deeper into cloud infrastructure.

Market pricing is now asking whether those hyperscaler signals can become a larger recurring royalty stream. If data-center royalties keep compounding, ARM can deserve a different multiple than a handset-cycle IP vendor. If smartphone weakness absorbs the benefit, the stock's AI premium becomes harder to defend.

Guidance helped, but capacity is now part of the thesis

Near-term guidance was supportive rather than spectacular. Arm guided Q1 FYE27 revenue to $1.26 billion, plus or minus $50 million, and non-GAAP diluted EPS to 40 cents, plus or minus 4 cents. Reuters said Wall Street had expected $1.25 billion of revenue and 36 cents of adjusted EPS.

Capacity is the more important detail for the next few quarters. Arm's CEO told Reuters that the company has secured enough capacity to fulfill the first $1 billion of AGI CPU demand discussed at launch, while capacity for the second $1 billion still needs to be secured. That caveat keeps the $2 billion demand figure from becoming fully bankable revenue.

Investors should therefore treat the demand number as a valuation bridge, not a completed sale. The upside case requires Arm to move from customer interest to delivery, then from delivery to durable royalty and silicon economics. Any slippage in supply, timing or customer adoption could expose how much of the post-report move relied on future conversion rather than current shipments.

The next validation point is recurring data-center revenue

ARM can keep its AI premium if three signals hold together: license growth remains strong, data-center royalties keep outgrowing handset royalties, and AGI CPU demand converts into systems that cloud customers deploy at scale. Those signals would support the view that Arm is no longer priced only as a device royalty platform.

A weaker path is equally clear. Royalty misses, supply-chain constraints, slower AGI CPU capacity, or a renewed smartphone unit drag would make the rally look ahead of the financial evidence. With the stock already up sharply this year, the market has less patience for a story that stays mostly in backlog, design wins and future silicon demand.

The practical test after May 6 is not whether AI data-center demand exists. Arm has sourced evidence for that. The test is whether the company can turn that demand into visible recurring revenue quickly enough to justify the premium investors added after the earnings call.