ASML Holding (ASML) delivered a closely watched first-quarter report that reinforced its central role in the artificial intelligence buildout, though a softer near-term outlook has pressured shares and shifted investor focus to management’s upcoming conference call (9am ET). As the sole supplier of extreme ultraviolet (EUV) lithography machines, ASML sits at the very foundation of advanced semiconductor manufacturing, making it one of the most important “picks and shovels” providers in the AI ecosystem. Its tools are essential for producing cutting-edge chips at 3nm and below, meaning demand for its systems serves as a direct read-through on AI infrastructure spending from companies like Taiwan Semiconductor Manufacturing (TSMC), Samsung, and Nvidia’s broader supply chain.

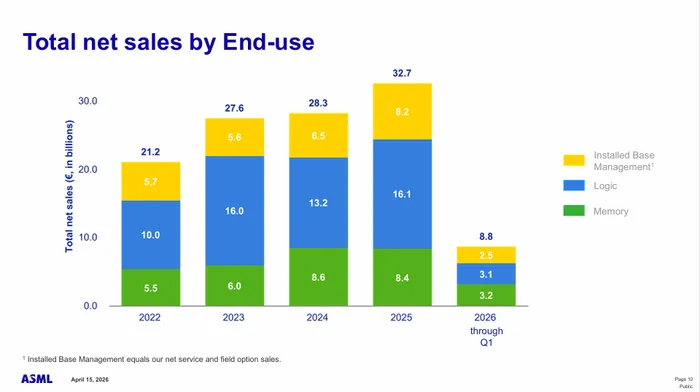

From a headline perspective, the quarter came in ahead of expectations . ASML reported Q1 revenue of €8.77 billion, above consensus estimates of approximately €8.63 billion, while net income of €2.76 billion also topped expectations of around €2.55 billion. Earnings per share of €7.15 beat by €0.55 versus consensus, reflecting solid execution and continued demand strength across its customer base. Revenue grew 13% year-over-year, driven by strong sales of advanced lithography systems and continued momentum in installed base management services. These results confirm that AI-driven demand is not just intact but accelerating, particularly as chipmakers race to expand capacity.

Gross margins were another key highlight, coming in at 53.0%, which was at the high end of the company’s guidance range and slightly above expectations. This level of profitability underscores ASML’s unique pricing power, driven by its near-monopoly position in EUV technology and the critical nature of its machines in semiconductor production. The company reiterated its full-year gross margin outlook of 51% to 53%, suggesting continued stability despite potential geopolitical and supply chain uncertainties. For investors, this margin profile remains a critical component of the long-term investment thesis, as it reflects both strong demand and disciplined cost management.

However, the market reaction has been more muted, with shares trading lower following the release, and the primary culprit is the company’s second-quarter guidance. ASML expects Q2 revenue in the range of €8.4 billion to €9.0 billion, which falls below consensus estimates of approximately €9.07 billion. While not a dramatic miss, the guidance introduces uncertainty at a time when expectations for AI-driven growth are already elevated. In contrast, the company raised its full-year 2026 revenue outlook to €36 billion to €40 billion, up from a prior range of €34 billion to €39 billion and broadly in line with expectations. This creates a tension in the narrative: strong long-term demand but potential near-term lumpiness in deliveries.

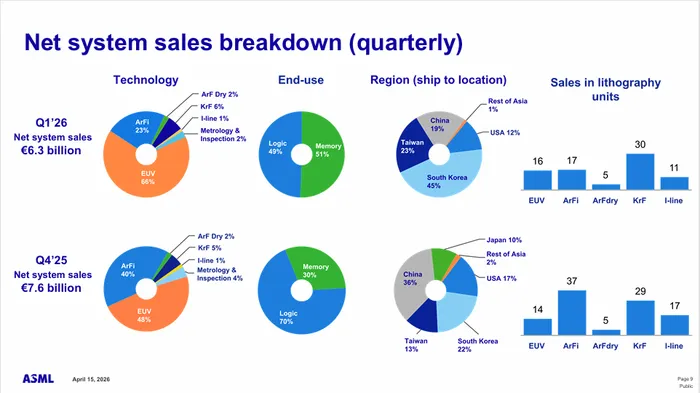

Management commentary suggests that demand remains robust, with CEO Christophe Fouquet stating that “demand for chips is outpacing supply” and that customers are accelerating capacity expansion plans into 2026 and beyond. This is consistent with broader industry signals, including aggressive capital expenditure plans from TSMC and continued investment from memory manufacturers like Samsung and SK Hynix. Notably, ASML indicated that 51% of its system sales in the quarter were tied to memory customers, a sharp increase from 30% in the prior quarter, highlighting the growing importance of memory in AI workloads.

Production and delivery dynamics remain a key area of focus. ASML sold 67 new lithography systems in the quarter, down from 94 in the prior quarter, reflecting the inherent lumpiness of its business given the high cost and complexity of its machines. The company also reiterated that it is closely aligned with customers to support demand through both new system deliveries and upgrades to its installed base. Looking further out, management suggested it could deliver up to 80 low numerical aperture EUV machines in 2027, though this fell short of some investor expectations closer to 90 units. This has raised questions about the pace of production scaling and whether supply constraints could limit upside in the medium term.

Another point of contention is ASML’s previous decision to stop disclosing quarterly order intake, historically a key metric for investors. While management emphasized that order activity remains “very strong,” the lack of transparency has introduced an additional layer of uncertainty, particularly in a market that is already highly sensitive to forward demand signals. At the same time, geopolitical risks remain in focus, especially around China, where export restrictions continue to limit the company’s ability to ship its most advanced systems. China accounted for 19% of sales in the quarter, down from 36% previously, and further restrictions could weigh on future growth.

The upcoming conference call at 9 a.m. will be critical for shaping the market’s interpretation of the quarter. Investors will be listening closely for management to address the softer Q2 guidance and to clarify whether it reflects conservatism or genuine near-term demand variability. A strong defense of the long-term outlook, particularly around AI-driven demand and capacity expansion, could help stabilize sentiment. Conversely, any indication that demand is normalizing or that production constraints are more binding than expected could pressure the stock further.

Technically, the setup is becoming more fragile. Shares are already under pressure following the results, and if management fails to convincingly frame the Q2 guidance as conservative, the stock could see further downside toward its 50-day moving average near $1,395. Given the stock’s strong run over the past year and elevated expectations around AI, the bar for reassurance is high.

In sum, ASML delivered a strong quarter that reinforced its structural importance to the AI ecosystem, with beats across revenue, earnings, and margins. However, the softer Q2 outlook and questions around production scaling and order visibility have introduced near-term uncertainty. The long-term story remains intact, but the next leg of the stock will likely depend on management’s ability to convincingly articulate that this is a timing issue rather than a demand problem.