Bank of America (BAC) delivered a strong start to 2026, with first-quarter results coming in ahead of expectations across most key metrics, reinforcing the narrative of a resilient U.S. consumer and a still-healthy financial system. The company reported earnings per share of $1.11, topping consensus estimates of $1.01, while revenue of approximately $30.3 billion also exceeded expectations of roughly $29.9 billion. Net income rose 17% year-over-year to $8.6 billion, marking one of the bank’s strongest quarterly performances in recent years. The upside was driven by broad-based strength across net interest income, trading, investment banking, and asset management, with management highlighting “healthy client activity” and “stable asset quality” as key pillars supporting the results.

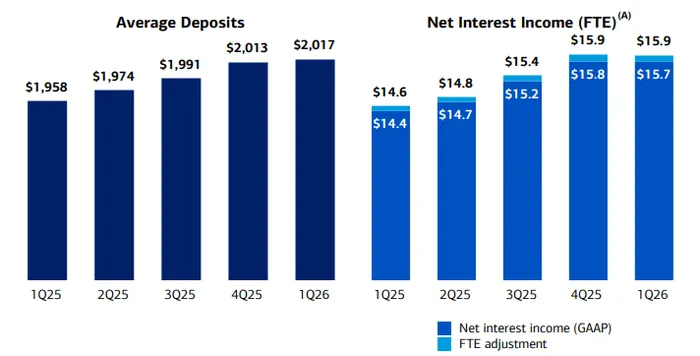

A closer look at the core drivers shows that net interest income (NII) remained a major contributor, rising 9% year-over-year to $15.7 billion and coming in ahead of expectations. This strength was fueled by higher loan and deposit balances, along with the continued benefit of fixed-rate asset repricing and strong activity in global markets. Importantly, this performance came despite some pressure from lower interest rates, suggesting that balance sheet growth and mix are doing more of the heavy lifting. Non-interest income also contributed meaningfully, increasing 5% year-over-year, with particularly strong gains in asset management fees (+15%) and investment banking fees (+21%), underscoring a recovery in capital markets activity.

The Global Markets segment was a standout, with sales and trading revenue rising 13% to $6.4 billion, marking the 16th consecutive quarter of year-over-year growth. Within this, equities trading surged 30% to $2.8 billion, significantly beating expectations and reflecting elevated client activity amid geopolitical volatility. Fixed income, currencies, and commodities (FICC) revenue, however, was more subdued, rising just 2% and missing expectations, highlighting a divergence in trading performance across asset classes. Still, the strength in equities was enough to drive one of the best trading quarters in over a decade, reinforcing Bank of America’s competitive positioning in market-sensitive businesses.

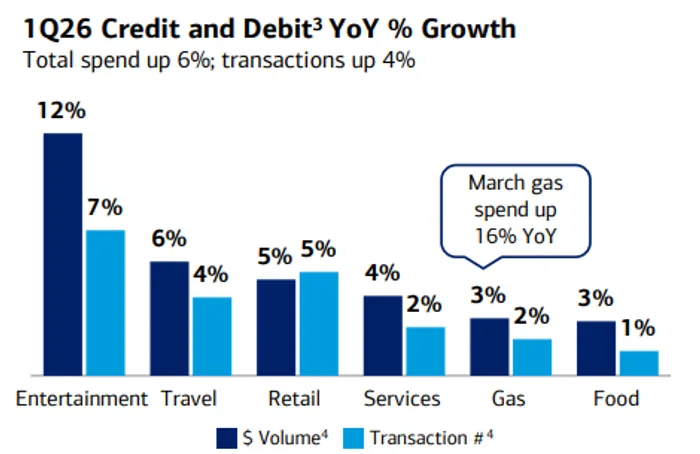

Consumer Banking also delivered solid results, with revenue increasing 5% to $11.0 billion and net income reaching $3.1 billion. The segment continues to benefit from steady consumer engagement, with credit and debit card spending up 7% year-over-year to $245 billion and continued growth in checking accounts. Deposits remained stable at $951 billion, while loans grew modestly. Importantly, credit quality within this segment improved, with provision for credit losses down 12% and net charge-offs declining slightly, reflecting stable borrower behavior. The data suggests that, despite macro uncertainty, the U.S. consumer remains in relatively good shape, supported by employment and wage growth.

Global Wealth and Investment Management was another area of strength, with revenue rising 12% to $6.7 billion and net income of $1.3 billion. The growth was driven primarily by higher asset management fees, supported by stronger market valuations and positive net client flows. Client balances reached $4.6 trillion, up 10% year-over-year, while assets under management climbed 14%. The segment also saw continued growth in high-net-worth relationships, with approximately 4,000 new $500K+ accounts added during the quarter. This performance highlights the operating leverage embedded in wealth management during periods of rising asset prices and reinforces its role as a stable earnings contributor.

Global Banking posted more moderate growth, with revenue increasing 5% to $6.3 billion and net income of $2.1 billion. Investment banking fees were a key bright spot, rising 21% to $1.8 billion and exceeding expectations, reflecting improved deal activity. Loan growth was steady across corporate and commercial segments, while deposits increased 13%, signaling continued client engagement. However, the segment also saw a slight increase in provisions for credit losses and reserve builds, suggesting some caution around corporate credit conditions, even as overall trends remain stable.

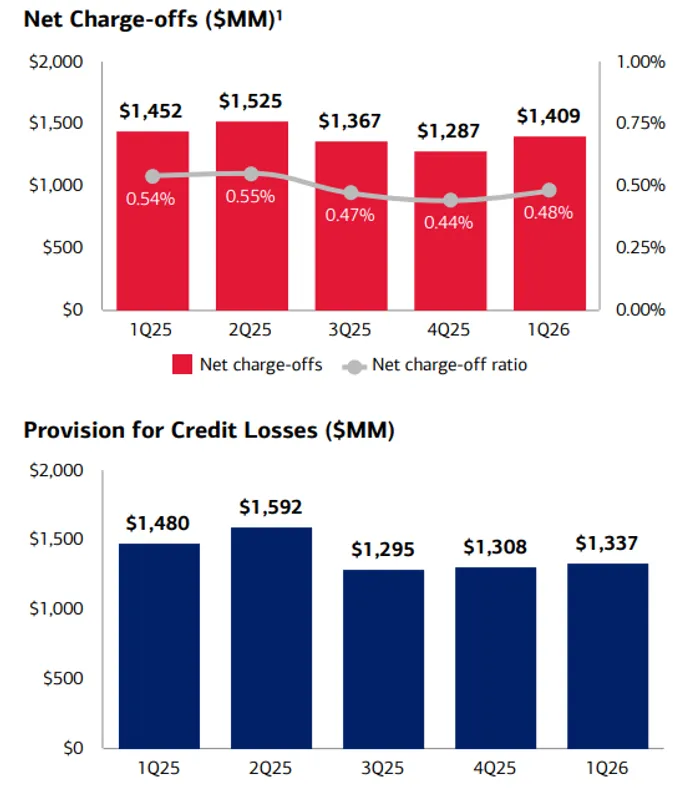

On the credit front, Bank of America’s results were reassuring. The company reported a provision for credit losses of $1.3 billion, down from $1.5 billion a year ago and below expectations. Net charge-offs were $1.4 billion, reflecting typical seasonality in credit cards but remaining well-contained. The net charge-off ratio improved to 0.48%, and management emphasized that asset quality remains stable. Notably, the bank stated it has not experienced any material losses in private credit and highlighted that its loan portfolio is more balanced and carries less inherent risk than in prior cycles. This commentary is particularly important given growing investor concerns about private credit exposure across the financial system.

From a balance sheet perspective, the bank remains well-capitalized and liquid. Average deposits rose 3% to $2.02 trillion, marking the 11th consecutive quarter of sequential growth, while loans and leases increased 9% to $1.19 trillion. The CET1 ratio stood at 11.2%, comfortably above regulatory requirements, even after returning $9.3 billion to shareholders through dividends and buybacks. Profitability metrics also improved, with return on tangible common equity reaching 16%, up more than 200 basis points year-over-year, reflecting strong operating leverage and disciplined cost management.

Looking ahead, Bank of America’s tone was cautiously optimistic. Management reiterated that client activity remains healthy and that the broader economy appears resilient, but also noted that it is “watchful of evolving risks.” While the bank did not provide a detailed near-term outlook in the release, prior guidance calls for net interest income growth in the mid-single-digit range, and the current trajectory suggests that target remains achievable. Investors will be closely watching whether trading and investment banking momentum can continue, as well as any signs of credit deterioration, particularly if geopolitical tensions or higher oil prices begin to weigh on growth.

Overall, the quarter reinforced Bank of America’s position as a well-diversified franchise benefiting from multiple earnings levers. Strong performance in markets and wealth management, combined with stable credit quality and solid consumer trends, helped offset pockets of weakness such as softer FICC trading. The key question going forward is whether this momentum can be sustained as the macro environment becomes more uncertain and the market shifts from a relief rally toward a more earnings-driven phase.