The biogas market is entering a sustained growth phase, but its investment case hinges on the durability of policy support and energy security incentives, which are themselves cyclical and regionally uneven. This isn't a simple linear climb; it's a commodity cycle where the long-term trajectory is being reshaped by geopolitical shocks and the global push for energy independence.

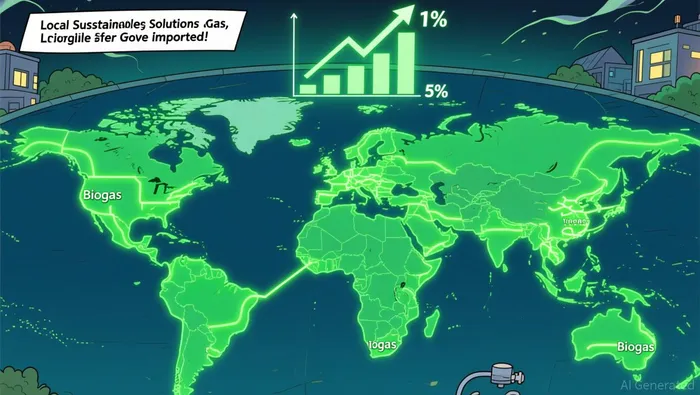

The numbers point to a powerful underlying trend. The global market is projected to grow at an 8.1% CAGR from its current size, reaching a value of $93.7 billion by 2034. This expansion is not just about incremental gains. It's about biogas's projected rise from a niche player to a significant fuel source. In the International Energy Agency's Stated Policies Scenario, its share of total gaseous fuel demand is expected to climb from 1% in 2023 to around 5% by 2050. That trajectory frames the opportunity: biogas is being positioned as a critical low-emissions fuel for sectors that cannot easily be electrified.

The catalyst for this accelerated cycle was a geopolitical shock. The Russian invasion of Ukraine in 2022 triggered a fundamental re-evaluation of energy security across Europe and beyond. This crisis directly boosted interest in developing biomethane as a substitute for imported natural gas. The result was a strengthening of policy incentives, notably in Europe and China, which are now key drivers of the market's growth. In other words, the war acted as a powerful policy accelerator, turning a long-term climate goal into an urgent energy imperative.

This creates a macro cycle where growth is driven by a feedback loop: geopolitical instability increases demand for alternatives, which spurs policy support, which in turn attracts investment and scales the industry. Yet the cycle's durability is not guaranteed. The projected investment needs are substantial, with the IEA noting that annual spending on biogases must rise from an average of $3 billion per year over the past decade to $15 billion per year by 2050 under current policies. This hinges on overcoming barriers like long payback periods. The path to scale is therefore not just about technology or feedstock-it's about the persistence of the energy security and climate policy framework that makes the investment math work.

Regional Leadership and Their Policy Cycles

The global biogas cycle is not uniform; it is a mosaic of regional growth engines, each powered by a distinct blend of natural resources and policy frameworks. Understanding which drivers are likely to be sustained versus temporary is key to navigating the investment landscape.

Brazil exemplifies a market where natural endowment and policy support are aligning for a steady climb. The market is projected to grow at a 4.32% CAGR to reach $1.7 billion by 2034. This expansion is underpinned by a massive technical potential, with the country's feedstocks capable of generating enough biomethane to supply 31.8% of national electricity demand. The growth is driven by a large agricultural base and supportive environmental policies, creating a durable cycle where waste-to-energy technology adoption strengthens alongside sustainability goals. The feedstock dominance of livestock manure and sugarcane residues ensures a consistent, low-cost input stream, providing a structural advantage that policy alone cannot easily replicate.

Germany's trajectory is more directly tied to its ambitious climate targets and a well-established regulatory framework. The market is forecast to grow at 4.9% annually through 2033, supported by government incentives and a focus on agricultural and municipal waste. This growth is a direct response to the national goal of climate neutrality by 2045, embedding biogas into the energy transition. The driver here is policy-driven demand, which provides long-term revenue certainty for developers. While the feedstock base is diverse and reliable, the sustainability of the growth rate depends on the continuity and strength of these incentives, making it more sensitive to shifts in the political and economic cycle than Brazil's resource-led model.

India's momentum, meanwhile, is being propelled by a dual catalyst: supportive policy frameworks and corporate decarbonization targets. While specific market size projections for India are not in the evidence, the global industry's 4.59% CAGR in capacity reflects strong emerging market growth, with India as a key contributor. The driver is less about a single national policy and more about a convergence of national renewable energy goals and corporate ESG commitments. This creates a powerful, multi-faceted demand pull that can sustain growth even if individual policy initiatives face delays. The focus on agricultural and food-waste feedstocks also aligns with waste management challenges, adding a layer of social and environmental justification.

The bottom line is that Brazil's cycle appears most anchored to its fundamental resource base, offering a longer-term, less policy-volatile path. Germany's growth is a direct function of its climate policy cycle, which is robust but requires sustained political will. India's momentum is a product of a broader decarbonization trend, making it a high-potential, though perhaps more volatile, segment of the global cycle. For investors, the regional mix offers a way to diversify exposure across different types of growth drivers.

Investment Landscape and Execution Risks

The macro drivers are clear, but translating them into investment returns requires navigating a complex landscape of execution risks and structural challenges. The confidence of major players is a positive signal, yet the path to scale is fraught with logistical and policy uncertainties.

On the bullish side, the expansion plans of established firms like Veolia and EnviTec Biogas in Germany, and the broader industry momentum noted by Mordor Intelligence, indicate a sector gaining credibility. This is supported by a fundamental shift in the value chain: a growing focus on upgrading biogas to renewable natural gas (RNG) and the rising corporate decarbonization targets that are creating a new, stable demand pull. This move from simple electricity generation to high-value RNG for transport and grid injection enhances project economics and opens a more durable revenue stream.

Yet the sector faces significant operational hurdles. Scaling requires solving the "last mile" problems of feedstock logistics and grid integration. The evidence highlights the need for enhanced technological integration and collaborative partnerships to manage diverse inputs like livestock manure and municipal waste efficiently. Without solving these supply chain and infrastructure bottlenecks, the projected capacity growth of 4.59% annually could face delays and cost overruns.

The most persistent risk, however, is the cyclical nature of policy support. The market's accelerated growth is a direct response to the geopolitical shock of 2022, which triggered strengthened policy incentives, notably in Europe and China. This creates a dependency on continued political will and economic stability. The long-term trajectory, which depends on incentives becoming permanent, is vulnerable to shifts in government priorities or fiscal constraints. The investment case, therefore, is a bet on the durability of a policy cycle that was itself born from a crisis.

The bottom line is a market of high potential but high friction. The corporate expansions and value chain upgrades point to a maturing industry, but the execution risks-logistics, integration, and policy volatility-will determine whether the projected growth is smooth or bumpy. For investors, the opportunity lies in backing players with the technical and financial capacity to navigate these constraints, while remaining acutely aware that the sector's fortunes remain tied to the stability of its policy lifeline.

Catalysts and Watchpoints for the Cycle

The investment thesis for biogas hinges on a few critical forward-looking events. These are the metrics and milestones that will confirm whether the sector's growth is becoming self-sustaining or remains hostage to policy whims and infrastructure delays.

First, monitor the implementation of the EU's RED IV consultation and similar policy frameworks in key markets. This is the single most important catalyst for defining the long-term regulatory environment. The consultation, which seeks to develop a pathway for renewable energy post-2030, will signal whether the bloc's ambitious 90% GHG reduction target by 2040 translates into concrete, binding mandates for biomethane blending or renewable gas quotas. The outcome will set the standard for other regions, directly influencing investment certainty and project economics across Europe and beyond. A positive, prescriptive framework would validate the sector's structural growth case; a vague or delayed rollout would introduce significant uncertainty.

Second, track the pace of biogas-to-biomethane upgrading capacity and pipeline injection infrastructure. The industry's value chain is maturing, with a clear shift toward upgrading biogas into renewable gas for transport and grid injection. Yet, this upgrade is only valuable if there is a market and a way to deliver it. The recent deal to purchase 50GWh of French-origin biomethane annually highlights the demand pull, but scaling requires a parallel build-out of the physical backbone. Delays in pipeline access or insufficient RNG blending mandates would cap the value of projects, keeping them mired in lower-margin electricity generation. This is the "last mile" constraint that must be solved for the cycle to reach its full potential.

Finally, watch for shifts in natural gas prices and energy security concerns. These act as powerful, cyclical catalysts that can dramatically accelerate adoption. The sector's recent growth was a direct response to the Russian invasion of Ukraine in 2022, which triggered interest in biomethane as a substitute. If geopolitical tensions resurface or gas prices spike, the economic case for biogas becomes compelling again, potentially triggering a new wave of investment. Conversely, prolonged periods of cheap, abundant gas could dampen the urgency for alternatives, testing the durability of policy-driven demand. This volatility is a core feature of the commodity cycle, and investors must be prepared for these swings.

The bottom line is that the cycle's trajectory will be confirmed or challenged by these three watchpoints. Policy frameworks set the long-term rules of the game, infrastructure unlocks the value, and energy market volatility provides the catalysts for acceleration. Monitoring them is essential for navigating the path from projected growth to realized returns.