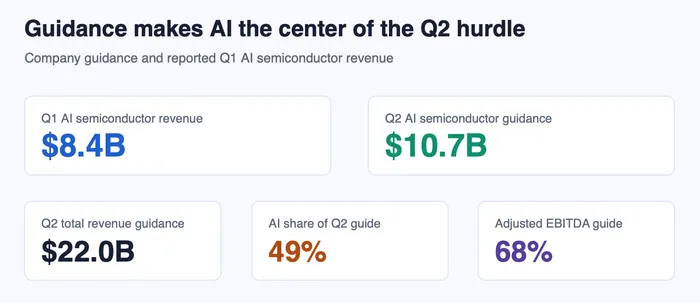

Broadcom reports fiscal second-quarter results after the U.S. close on Wednesday, June 3, and the bar is already set by its own March guide. The company said Q2 revenue should reach about $22.0 billion, adjusted EBITDA should run near 68% of revenue and AI semiconductor revenue should reach $10.7 billion, up about 140% from a year earlier. A result that confirms that run rate would give the chip rally a second anchor outside Nvidia GPUs. A guide that lacks margin or customer-timing detail would leave custom silicon growth large but harder to extend across the sector.

AVGO matters beyond one ticker because Broadcom sits between Nvidia's accelerator platform and the hyperscaler push to design more of the compute stack themselves. The June update needs to show whether custom accelerators, Ethernet networking and VMware cash flow can carry the next phase without asking the market to ignore customer concentration, TSMC dependence or mix-related profitability drag.

Sources Broadcom Q1 FY2026 release and company guidance. AI share is calculated from the $10.7 billion AI semiconductor guide and the $22.0 billion total revenue guide.

The bar is already near half of guided sales

March guidance made the second quarter a high-threshold report before a single result appears. Broadcom's $10.7 billion AI semiconductor target would be about 49% of the company's $22.0 billion total revenue guide, based on the two official guidance figures. Reuters reported that AVGO shares rose nearly 5% after that guide and that management had line of sight to more than $100 billion of AI revenue by fiscal 2027. That prior reaction makes the June report less about announcing demand and more about confirming whether the revenue path is still accelerating.

AI semiconductors are no longer an optional side story inside Broadcom's model. They are close to half of the guided Q2 revenue base, so a modest top-line beat can still disappoint if Q3 AI guidance, backlog visibility or adjusted EBITDA quality fails to rise with it. The harder question is whether the company can add scale without making the market pay less for each dollar of chip revenue.

Customer timing now matters as much as the number

Broadcom's April filing disclosed a Google custom TPU and networking supply agreement running to 2031 and a Google Anthropic agreement for up to 3.5 gigawatts of TPU access beginning in 2027, subject to commercial success conditions. Those details move the story away from broad AI enthusiasm and toward a more measurable question. When do the largest customers convert committed AI infrastructure plans into chip shipments, networking content and cash collections for Broadcom.

Reuters reported that Broadcom shares rose about 3% in extended trading after the Google and Anthropic announcement, which shows that the market gave value to customer visibility before the June report. The counterweight is concentration. A few hyperscalers can create a long revenue runway, but they can also compress timing into a small set of product cycles and negotiation windows.

Networking is the swing factor inside the AI mix

Custom accelerators get the headline, but networking decides whether Broadcom's AI revenue is a broader platform or a narrow accelerator ramp. CRN reported that AI networking was about one third of Broadcom's Q1 AI revenue and was expected to approach 40% in Q2. That mix matters because Ethernet switching, routing and connectivity attach Broadcom to the data-center buildout even when the market debate starts with GPUs.

AVGO is the custom-accelerator and networking name, Nvidia remains the GPU platform benchmark, Marvell is the custom and optical peer pressure point, and SMH or SOX shows whether the sector accepts a broader AI semiconductor bid. CRN also reported that Broadcom had secured supply-chain capacity for customer demand from 2026 through 2028, so June commentary on capacity, lead times and second-source risk will carry as much information as the headline AI revenue figure.

Margins decide whether revenue quality keeps up

Revenue acceleration alone is not enough because the Q2 guide already bakes in high profitability. Broadcom guided adjusted EBITDA to about 68% of projected Q2 revenue and reported Q1 infrastructure software revenue of $6.796 billion. The software base gives the model a cash-flow cushion, but the market still needs to see whether the semiconductor mix can expand without turning the margin story into a tax on growth.

The Morningstar report supplied for this preview lists Broadcom with a $500 fair value estimate, a 0.89 price to fair value ratio, a wide moat rating and high uncertainty. That combination is useful for framing, not for replacing company facts. It says the valuation debate is already generous to durable AI and software economics, while uncertainty remains high enough that one weak guide can matter.

Morningstar also frames custom AI chips as potentially gross-margin dilutive but operating-margin accretive as volume rises. The June report therefore needs a quality bridge. Higher AI chip dollars are constructive only if adjusted EBITDA, supply costs and software cash flow show that scale is producing operating leverage instead of only larger revenue.

Three cases decide the post-call read

Morningstar identifies customer concentration, TSMC reliance, supply constraints and key-person risk as major uncertainties. Those are not reasons to dismiss the AI ramp, but they keep the earnings setup narrow. A stronger June report should separate confirmed shipments from customer reservations, near-term supply from long-term capacity, and AI networking from custom accelerator timing.

- Bullish read. Q2 AI revenue clears the $10.7 billion guide and adjusted EBITDA stays close to the 68% guide, while networking mix keeps moving toward the Q2 path CRN reported and management ties Q3 demand to named customer ramps. That would make AVGO a stronger sector-breadth signal, not only a company-specific beat.

- Neutral read. Q2 AI revenue lands near the guide and EBITDA holds, but Q3 AI guidance and customer timing stay broad. That would keep Broadcom's AI story credible while limiting the read for NVDA, MRVL, SMH and SOX.

- Bearish read. Q3 AI guidance fades, networking detail is thin, or profitability comments show custom silicon absorbing more supply cost than expected. That would move the debate back to the customer concentration, TSMC reliance and margin-dilution risks flagged in the research context.

The market conclusion is therefore conditional. Treat the print as a positive AI-breadth confirmation only if the bullish read arrives in the same report. A merely solid Q2 number with missing Q3 or networking detail is neutral. A guide that loses customer or EBITDA support shifts the read back to AVGO-specific execution risk.