The current gasoline price surge is not a simple story of crude oil moving up and down. It is a complex macro cycle in motion, where global crude prices, geopolitical shocks, and regional refining capacity collide to create persistent disparities. The national average has now exceeded $4 per gallon for the first time since 2022, a level driven directly by supply fears. The primary catalyst is the ongoing conflict between the U.S. and Iran, which has led to the effective closure of the Strait of Hormuz-a chokepoint for roughly a fifth of the world's oil. This geopolitical tension has triggered a classic "rockets and feathers" dynamic, where pump prices shoot up quickly in response to crude spikes, creating immediate economic strain.

Yet, the macro picture is more nuanced. The U.S. government's traditional tool for managing such shocks, the Strategic Petroleum Reserve, has shown limited power to counter these forces. Past releases have typically lowered pump prices by only 13 to 31 cents per gallon. This narrow impact highlights that the current pressure is structural and widespread, not easily offset by a one-time injection of supply. The macro dimension of this price spike is significant; gasoline is one of the least discretionary household costs, and its visibility makes it a potent driver of inflation expectations, potentially constraining the Federal Reserve's policy path.

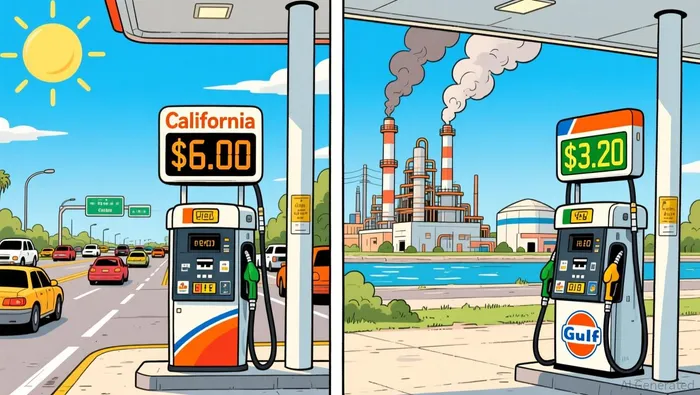

This sets the stage for deep regional divergence. While the national average reflects a broad trend, actual prices vary wildly. States like California, Oregon, and Hawaii are seeing averages above $5 per gallon, with California drivers paying over $6. Meanwhile, the South and Midwest hold the lows. This gap is amplified by refining capacity. The U.S. Energy Information Administration forecasts that decreasing U.S. refinery capacity this year may offset some of the effects of lower crude oil prices, particularly on the West Coast. The region is already facing a forecasted capacity loss that will keep its gasoline margins and prices elevated relative to 2025 levels, even as the national average is projected to fall. The bottom line is that the macro cycle is defined by a high-crude-price environment, but the local price you pay is determined by how much refining capacity you have to convert that crude into fuel.

Regional Anatomy: From West Coast Premium to Gulf Coast Discount

The national average price is a starting point, but the real story unfolds at the regional level. The macro forces of high crude and geopolitical risk translate into a stark geographic map of gasoline costs, where isolation, infrastructure, and policy create persistent premiums and discounts.

The West Coast, or PADD 5, consistently commands the highest prices. In March 2026, its average hit $4.89 per gallon, a figure driven by a perfect storm of constraints. The region's gasoline is produced from a unique, highly regulated blend, and it has relatively few refineries that must run at near full capacity to meet local demand. This makes the supply chain vulnerable; any disruption can quickly spike prices. Furthermore, the region's geographic isolation means that even when supplies are available elsewhere, getting fuel to California or Oregon takes time and adds cost. As a result, the West Coast often pays a significant premium, with prices sometimes exceeding $6 per gallon.

In contrast, the Gulf Coast, or PADD 3, typically offers the lowest prices. Its average in March was $3.27 per gallon. This discount is a direct function of its position as a major refining and export hub. The region is home to a dense concentration of refineries and pipelines, giving it proximity to both crude oil inputs and major distribution networks. This abundance of supply and efficient logistics keeps local prices anchored lower. The Gulf Coast's role as a key export point also means it can be a source of surplus fuel for other regions, reinforcing its position as a price anchor.

Beyond these broad regional trends, a secondary layer of variation is created by state and local taxes, distribution costs, and retail competition. The interactive map from The New York Times vividly illustrates this, showing county-level differences that often defy state borders. A driver in a rural county may pay more than one in a neighboring urban area due to fewer competing stations and higher transportation costs. Similarly, states with high fuel taxes, like California, add another permanent cost layer on top of the regional premium. These factors mean that while the macro cycle sets the broad price trajectory, the final pump price you see is a local equation of geography, regulation, and market structure.

The Forward View: Cyclical Pressure vs. Structural Constraints

The macro cycle for gasoline is now in a defined phase. On one hand, the EIA forecasts a 6% decline in national gasoline prices in 2026, following a trend of falling costs since the 2022 peak. This cyclical pressure is driven by the expectation of lower crude oil prices, with the agency projecting a fall to their lowest annual average since 2020. For investors and policymakers, this suggests a near-term relief valve is in place, with the national average likely to drift back toward the $4 range.

Yet this broad forecast masks a persistent structural reality: regional divergence is expected to persist and even widen. The EIA explicitly notes that decreasing U.S. refinery capacity this year may offset some of the effects of lower crude oil prices on gasoline, especially in the West Coast region. This means the West Coast, already the highest-priced region, will see its prices remain elevated relative to the national trend. The Gulf Coast, with its abundant refining and export capacity, is forecast to maintain its role as the price anchor. The bottom line is that the cyclical decline in crude will provide a floor for national averages, but local supply constraints will continue to define the upper end of the price range.

The most significant risk to this forecast is geopolitical volatility. The ongoing conflict between the U.S. and Iran has already pushed six states into the $5 per gallon range, with California exceeding $6. If tensions escalate further, the potential for a sharp, upside shock to prices remains. The EIA's forecast assumes a baseline of lower crude prices, but a new supply disruption could quickly reset that trajectory. Analysts warn that continued upward pressure could push more regions into the $5 range in the coming weeks, demonstrating how fragile the current equilibrium is.

Zooming out to the long-term macroeconomic landscape, the continued dominance of fossil fuels underscores the inherent sensitivity of energy prices. Even as renewables grow, coal remains the world's largest source of electricity, generating nearly one-third of global power. This entrenched reliance on hydrocarbons means that the global economy will remain vulnerable to the same geopolitical and supply shocks that drive gasoline prices. For investors, this implies that while cyclical dips are predictable, the structural backdrop ensures that energy markets will always be a source of volatility and a key indicator of broader economic health.