Cisco's biggest market message was not simply that it beat another quarterly estimate. Reuters reported that Cisco shares surged 17% to a record high on May 14 after the company lifted its AI order outlook and announced a restructuring aimed at technology investment. AP later reported the stock finished up 13.4%, its best day in nearly 15 years.

Cisco's rally shows Wall Street is no longer just buying the chip inside the AI server. It is buying the network that makes the server useful. The AI trade is moving from who sells the GPU to who removes the bottlenecks around the GPU.

Investors are repricing the AI trade from a narrow accelerator story into a broader infrastructure chain. Nvidia still owns the center of the compute trade, but Cisco's quarter showed that cloud AI spending is also landing in the equipment that connects accelerators, moves data across clusters, protects traffic and links data centers together.

The Rally Was an AI Order Reset

Cisco reported Q3 FY2026 revenue of $15.8 billion, up 12% from a year earlier, and non-GAAP EPS of $1.06. Guidance also moved higher, with Cisco calling for Q4 FY2026 revenue of $16.7 billion to $16.9 billion and full-year revenue of $62.8 billion to $63.0 billion.

Those numbers mattered, but the stock reaction was tied to the AI order reset. Cisco said it had taken $5.3 billion of AI infrastructure orders from hyperscalers year to date and raised expected FY2026 orders to $9 billion from $5 billion. With one quarter still left in the fiscal year, the old target had already been exceeded.

For a company often valued around enterprise refresh cycles, that changes the stock debate. A normal earnings beat asks whether demand can hold for a few more quarters. Cisco's AI order guide asks whether networking gear is becoming a structural line item in the same AI capex budgets that drove GPU, HBM, server and power-equipment demand.

Source scope: stitched from Cisco Q2 FY2026 and Cisco Q3 FY2026 releases. Basis: hyperscaler AI infrastructure orders for FY2026 through Q3 and company targets, not recognized revenue or profit.

Networking Is Becoming Part of the Compute Trade

AI clusters do not scale on accelerators alone. As GPU clusters grow, latency, bandwidth, power efficiency, optical interconnect and security management become harder constraints. Training and inference workloads require switching, routing, optics, telemetry, security and software control so GPUs can stay fed with data instead of waiting on congestion, packet loss or interconnect bottlenecks.

Cisco's product disclosures support that shift. In Q3, Networking revenue rose 25%, campus networking orders grew more than 25%, and data-center switching orders grew more than 40%. Those metrics are not pure AI revenue, but they show that the AI trade is touching the larger networking refresh cycle.

A February product release made the same point at the architecture level. Cisco described Silicon One G300 as 102.4 Tbps switch silicon for AI clusters, with new N9000 and 8000 systems, optics and management tools aimed at hyperscalers, neoclouds, sovereign clouds, service providers and enterprises.

That matters for Nvidia-linked investors because better networking can raise effective GPU utilization. It also matters for Cisco because the buyer is no longer just an enterprise CIO replacing aging campus gear. The buyer increasingly includes AI infrastructure teams trying to make expensive compute clusters run more efficiently.

Scale changes the purchasing frame. Bigger training and inference footprints can turn a traditional server buy into a system-level infrastructure buy, where compute, networking, optical links, security policy, observability and energy efficiency are judged together. That is the point Cisco's rally forces the market to revisit.

The $9 Billion Number Reframes Cisco's Growth Story

Before the latest quarter, the cleanest Cisco bull case was a mix of product-order recovery, campus refresh and Splunk-driven observability. AI was visible, but still easy to treat as a useful add-on rather than the main rerating variable.

The new $9 billion order target is large enough to challenge that view. Reuters noted that Cisco had already taken $5.3 billion of AI infrastructure orders and raised the full-year expectation from $5 billion. In market terms, the stock is now being asked to carry a higher AI multiple before those orders have flowed through the income statement.

Orders are an earlier signal than revenue, not a substitute for it. That makes the rerating meaningful but still fragile. Strong orders show that hyperscalers are buying network capacity, but investors still need evidence that orders become revenue, revenue becomes profit and profit arrives without a material deterioration in margin quality.

Portfolio Focus Becomes Part of the Valuation Test

Cisco announced the rally alongside a cost action. In a May 13 employee note, the company said it would reduce its workforce in Q4 by fewer than 4,000 jobs, less than 5% of its total employee base, while investing in silicon, optics, security and employees' use of AI.

The market rewarded the message because it framed layoffs as capital reallocation rather than simple expense defense. That does not make the cuts a clean positive. If Cisco is reducing roles while emphasizing AI investment, investors may reward near-term efficiency but demand stronger product iteration, faster delivery and tighter execution in the areas management says matter most.

Margin is the other constraint. Cisco's Q3 non-GAAP gross margin was 66.0%, down from 68.6% a year earlier, even as revenue and orders improved. AI networking demand can lift growth, but a hardware-heavy mix, component costs and competitive pricing can still limit operating leverage.

The Read-Through Spreads Beyond Cisco

AP's market wrap captured the broader setup: U.S. equities hit more records as Cisco joined companies reporting stronger-than-expected profits, and BlackRock's Gargi Pal Chaudhuri said earnings have shown an AI-led market where the impact is broadening quickly.

For the AI supply chain, Cisco's quarter points to a second layer of beneficiaries and tests. Switch makers, optical-component suppliers, Ethernet silicon vendors, security platforms, observability vendors and data-center interconnect providers all sit closer to the bottlenecks that appear after the GPU has been purchased.

Cisco's rally is not an isolated stock event if AI capex keeps expanding. It signals that investors are searching for the next constraint in the stack: bandwidth inside the cluster, power and cooling around the rack, optical links between systems, security around AI traffic and software that tells operators where performance is breaking.

That does not mean every networking or optics stock deserves a Cisco-style rerating. The stronger conclusion is narrower: the market is now willing to pay for proof that AI capex is creating non-GPU revenue pools. Companies that can show orders, backlog, revenue conversion and stable margins will have an easier case than companies selling only exposure language.

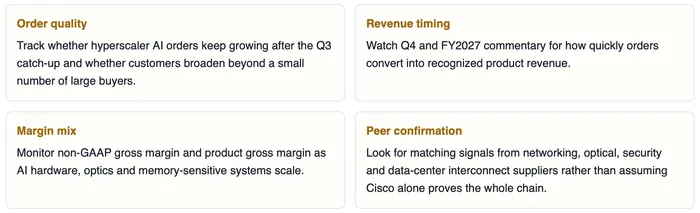

The Next Tests Are Revenue Conversion and Margin Quality

Cisco's rally has already priced in a more ambitious AI infrastructure story. Near term, the move is likely to push investors toward other non-GPU AI beneficiaries in networking, optical communications, power, cooling, security and data-center infrastructure. The stronger the headline chase becomes, the more important it will be to separate confirmed orders from broad exposure language.

Medium term, the AI infrastructure trade should move from buying the story to testing conversion. Further upside needs the $9 billion target to look conservative, not merely newly disclosed. A giveback risk would rise if orders slow, if hyperscaler deployments stretch out, if cloud customers trim AI capex, or if hardware mix pressure weighs on gross margin.

Longer term, network gear could move from a supporting cost to a performance bottleneck if GPU capex keeps expanding. That is the upside case for Cisco's rerating. The downside case is just as direct: second-layer AI beneficiaries can fall quickly if orders take longer to recognize, if margins weaken, or if peer results fail to confirm the broader infrastructure spillover.

Cisco has given investors a new place to look in the AI trade. The stock move says Wall Street is no longer paying only for the accelerator at the center of the cluster. The next phase will be judged by revenue conversion, margin quality and peer confirmation, not by order headlines alone.