Citigroup (C) delivered a strong first-quarter print that stood out relative to peers, with shares moving higher in early trading as investors rewarded a combination of solid execution, reaffirmed guidance, and an ongoing turnaround story under CEO Jane Fraser. While JPMorgan Chase (JPM) and Wells Fargo (WFC) both posted generally solid results but saw their stocks slip, Citi’s lower valuation and improving operating trajectory appear to be driving a more favorable reaction. The quarter reinforced the narrative that Citi is gaining momentum as it moves deeper into the final phase of its multi-year transformation.

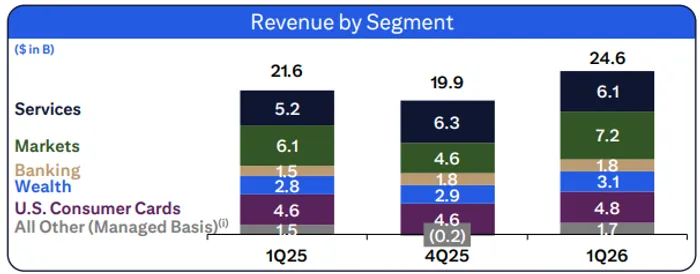

At the headline level , Citigroup reported earnings per share of $3.06, well above consensus expectations of $2.65, while revenue came in at $24.6 billion, topping estimates of $23.5 billion. Net income rose to $5.8 billion, up significantly from $4.1 billion a year ago, representing 42% year-over-year growth. The revenue beat was driven by broad-based strength across all five of Citi’s core businesses, with total revenue increasing 14% year-over-year.

Net interest income was a key contributor, rising 12% year-over-year to $15.7 billion, supported by growth across all operating segments. Noninterest revenue increased 17%, reflecting strong fee generation in areas like investment banking, wealth, and services. Importantly, Citi demonstrated positive operating leverage, with revenue growth outpacing expense growth, a key milestone for a bank that has been under pressure to improve efficiency.

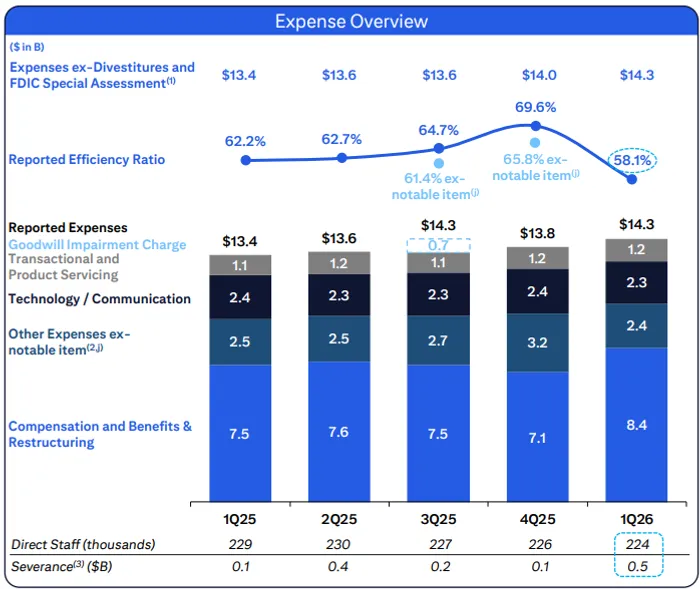

Expenses rose 7% to $14.3 billion, driven by higher compensation, severance costs tied to restructuring, and increased volume-related expenses. However, these increases were partially offset by productivity savings, lower legal costs, and declining transformation expenses, signaling that Citi’s restructuring efforts are beginning to yield tangible benefits. The efficiency ratio improved meaningfully to around 58%, highlighting better cost discipline and improved profitability.

Breaking down the segments, the Services business was a standout performer. Revenue increased 17% to $6.1 billion, driven by strong growth in Treasury and Trade Solutions and Securities Services. Net interest income rose 18%, supported by higher deposit balances and improved spreads, while fee income also expanded, reflecting increased cross-border transaction activity and higher custody assets. This segment continues to serve as a stable, high-return engine for Citi, with RoTCE of approximately 27%.

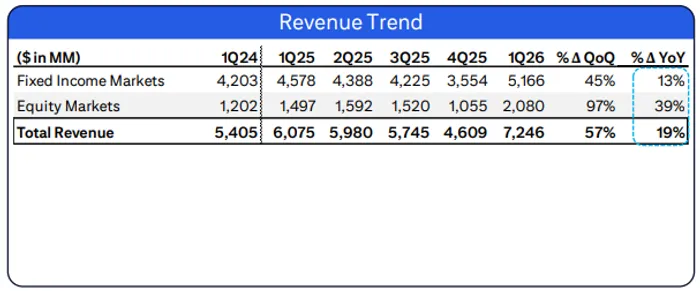

Markets also delivered a strong quarter, with revenue rising 19% to $7.2 billion. Fixed income trading increased 13%, driven by strength in commodities, currencies, and spread products, while equities surged 39%, supported by growth in derivatives, prime services, and cash equities. The segment benefited from elevated volatility and strong client engagement, similar to trends seen at peers, but Citi’s performance stood out due to its breadth across asset classes. Net income in Markets rose 40%, aided by both revenue growth and a favorable credit environment.

The Banking segment showed improving momentum, with revenue up 15% to $1.8 billion. Investment banking fees rose 12%, driven by strong advisory and equity capital markets activity, though partially offset by softer debt underwriting. Advisory fees increased 19%, while equity capital markets revenue jumped 64%, highlighting strength in equity issuance. Corporate lending was more mixed, with revenue down slightly due to mark-to-market impacts, though underlying loan spreads remained supportive.

U.S. Consumer Cards, a key area of focus for investors, delivered moderate growth. Revenue increased 4% to $4.8 billion, supported by higher loan balances and improved fee income. Net interest income rose 3%, while noninterest revenue climbed 14%, driven by higher interchange fees and card-related income. However, profitability was pressured by higher credit costs, with net income declining 13% as the bank built reserves and absorbed higher losses tied to seasonal trends and portfolio mix changes.

On credit, Citi reported a provision for credit losses of $2.8 billion, including $2.2 billion of net credit losses and a $597 million reserve build. While the provision increased modestly, net credit losses were actually down 10% year-over-year, suggesting underlying credit quality remains stable. The reserve build reflects a more cautious stance given macro uncertainty and portfolio growth rather than a deterioration in credit conditions.

Nonaccrual loans increased to $3.4 billion, up 25% year-over-year, driven primarily by corporate exposures, though the absolute level remains manageable. Citi ended the quarter with approximately $22 billion in total reserves, with a reserve-to-loans ratio of 2.6%, indicating a solid buffer against potential losses. Overall, credit trends appear stable, though investors will continue to monitor areas like consumer cards and corporate exposures for signs of stress.

The balance sheet remained strong, with loans increasing 8% year-over-year to $762 billion and deposits rising 10% to approximately $1.4 trillion. Capital levels are also robust, with a CET1 ratio of 12.7%, providing ample flexibility for continued capital return. Citi returned $7.4 billion to shareholders during the quarter, including $6.3 billion in share repurchases, underscoring management’s confidence in the firm’s capital position and earnings outlook.

Importantly, Citi reaffirmed its full-year 2026 outlook, maintaining its target for return on tangible common equity in the 10–11% range. The bank also reiterated expectations for mid-single-digit growth in net interest income excluding Markets and continued fee-driven growth across its businesses. This reaffirmation is a key differentiator relative to peers, as it provides investors with greater confidence in the trajectory of earnings and returns.

CEO Jane Fraser highlighted that the firm is now in the final phase of its transformation, with approximately 90% of its initiatives at or near completion. The restructuring has focused on simplifying the organization, exiting non-core businesses, and improving efficiency, all of which are now beginning to show up in the financials. The combination of revenue growth, improving margins, and disciplined capital return is reinforcing the turnaround narrative.

From a market perspective, Citi’s relative outperformance reflects both its results and its valuation. While not dramatically cheaper than some regional peers, the stock still trades at a discount to larger money-center banks, leaving more room for upside as execution improves. In contrast, JPMorgan’s premium valuation and Wells Fargo’s slower growth profile leave less margin for error, contributing to their weaker stock reactions.

Ultimately, Citi’s first-quarter results reinforce the view that the bank is steadily closing the gap with its peers. The combination of broad-based revenue growth, improving efficiency, stable credit, and reaffirmed guidance provides a compelling case for continued multiple expansion. While risks remain, particularly in the macro environment and credit cycle, Citi appears to be gaining traction at a time when investors are increasingly looking for both value and execution.