CME Group and Silicon Data said on May 12 that they plan to launch compute futures later this year, pending regulatory review, based on daily GPU rental-rate indices. For CME, Nvidia, CoreWeave and the cloud-capex trade, the market signal is not just a new product. It is a sign that AI compute is becoming a priced financial risk.

Investors have already rewarded the AI infrastructure chain for scarcity. Nvidia carries the hardware scarcity premium, CoreWeave represents the leveraged AI cloud model, and Microsoft, Amazon, Alphabet and Meta keep turning AI capacity into a capital-spending question. CME's plan challenges a narrower assumption: that GPU access stays a private procurement problem rather than becoming a benchmarked input cost that can be hedged, arbitraged and traded.

That shift matters because a futures market would not make AI compute cheaper by itself. It would make the price of compute more observable, which can pressure cloud margins, sharpen contract negotiations and give investors another way to test whether AI infrastructure economics are improving or merely becoming more financialized.

Compute is moving from capacity story to price-risk story

CME described the target market as a multi-trillion-dollar compute market with fragmented pricing across providers, regions and contract structures. That wording is important. It frames compute less like a software feature and more like power, freight, interest rates or energy: a cost line large enough to need a clearing price.

Silicon Data's role is the other half of the setup. Its indices track on-demand GPU rental rates, giving the contracts a benchmark rather than leaving the market dependent on anecdotal quotes. A benchmark does not guarantee liquidity, but it gives hedgers and speculators a common settlement language.

In market terms, the announcement turns one AI question into two. Demand still matters, but price discovery starts to matter as well. If compute rental rates fall, AI application builders may gain operating leverage while cloud suppliers face pricing pressure. If rates rise, the winners may be owners of scarce accelerated capacity, but the cost burden moves back to software and model companies.

GPU price dispersion is the evidence behind the contract

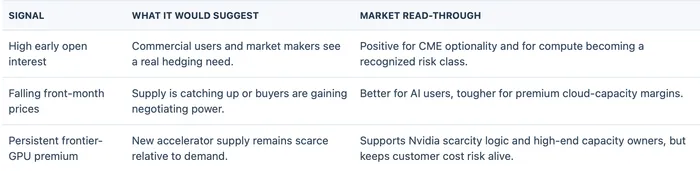

Silicon Data's April work shows why a benchmark can be useful. Its H100 Hyperscaler On-Demand Index moved in a narrow $7.40 to $7.52 band between March 1 and April 20, with a 0.47% coefficient of variation and a small net change over the period.

Newer-generation compute looked different. The same Silicon Data note said B200 rental pricing surged 24%, briefly moved above $6 an hour in late March and showed far more volatility. That is the market gap CME is trying to package: mature GPU capacity can trade like a stable benchmark, while frontier capacity can behave like a volatile scarcity premium.

For public equities, that split is a cleaner read-through than a simple bullish AI headline. Nvidia benefits if frontier scarcity persists, but cloud buyers and AI application companies benefit when benchmarked compute costs become more predictable. A futures curve could make those cross-currents visible before they show up in reported margins.

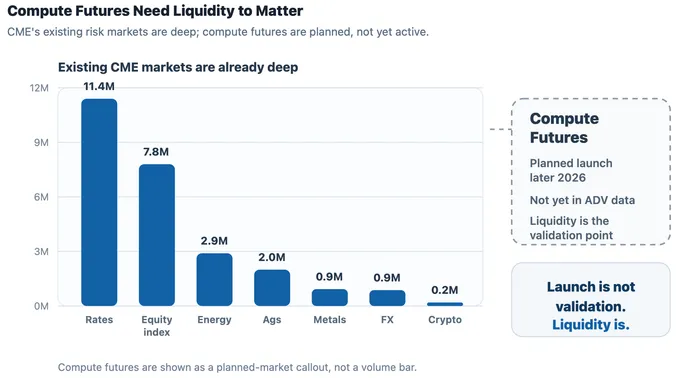

Source: CME Group April 2026 monthly volume release. Bars show April 2026 ADV by asset class, in millions of contracts. Compute futures are planned products and are not included in ADV data.

CME has the venue, but compute still needs a hedger base

CME's April data shows the scale that new risk markets must grow into. The exchange reported 25.9 million contracts of average daily volume, led by 11.4 million interest-rate contracts and 7.8 million equity-index contracts.

That liquidity stack is why the announcement matters for CME stock, even before any compute volume exists. A successful compute market could add a new data and transaction-fee category tied to one of the fastest-growing corporate cost pools. A failed launch would say something else: AI compute may be large, but not yet standardized enough for the listed-futures model.

Investors should treat regulatory approval as only the first gate. Useful futures markets need natural hedgers, speculators, market makers and trust in the settlement benchmark. Cloud providers, AI labs, banks, trading firms and large enterprise buyers all have reasons to care about compute prices. Whether they want to trade listed contracts is the open question.

CoreWeave shows why hedging does not solve the whole trade

CoreWeave is the cleanest public example of why compute costs and financing costs now sit at the center of AI infrastructure valuation. The company reported first-quarter 2026 revenue of $2,078 million, up from $982 million a year earlier, and said revenue backlog was nearly $100 billion.

Growth did not remove the margin question. CoreWeave also reported net interest expense of $536 million, a $740 million net loss and adjusted operating income margin of 1%, down from 17% a year earlier. That is the kind of model where compute-price visibility can help, but cannot erase debt service, depreciation or utilization risk.

A compute futures curve could eventually help investors separate volume demand from price pressure. If CoreWeave or peers show backlog growth while benchmark compute prices fall, revenue quality becomes harder to underwrite. If benchmark rates stay firm while utilization improves, the AI cloud trade gets a more durable economics signal.

Asset read-through is broader than CME

CME gets the most direct exchange-business optionality. Nvidia and accelerator suppliers get a new market-based signal for scarcity and pricing power. CoreWeave and other AI cloud capacity owners get a possible hedge, but also a public yardstick that can expose pricing pressure faster.

Hyperscalers sit on both sides of the ledger. Microsoft, Amazon, Alphabet and Meta are large buyers of compute, but they also sell cloud capacity and negotiate long-term infrastructure contracts. More transparent compute prices can help them manage cost risk, yet it may also make customers more aware of where cloud margins are coming from.

Software and AI application companies would probably prefer a liquid curve that lowers uncertainty around inference and training cost. The risk is that a futures market attracts financial flows before commercial hedging demand is deep enough, creating another volatile signal investors may overread.

Liquidity, not launch language, is the validation point

The planned contract has a clear market story, but it is not a finished repricing event. The validation path is practical: regulatory review, contract specifications, index governance, initial market-maker support, real commercial hedging and enough open interest to make the curve useful.

A clean launch would make AI compute easier to compare across providers and chip generations. It would also give investors a new dashboard for the AI margin debate: spot rental rates, futures spreads, cloud utilization, backlog conversion and capex intensity.

For now, the market should not treat CME's compute futures as proof that AI economics are solved. The better interpretation is more disciplined: AI infrastructure is becoming large enough, costly enough and volatile enough that Wall Street wants a contract for it. That makes compute pricing a new checkpoint for the AI trade, not a free pass for every stock attached to the theme.