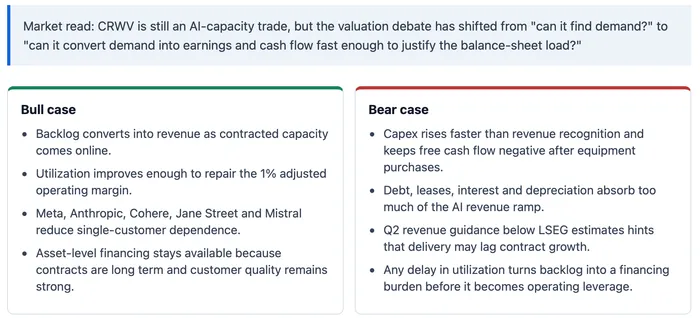

CoreWeave did not report a demand problem. It reported a delivery-cost problem. Shares fell more than 9% in extended trading on May 7 after revenue more than doubled, backlog approached $100 billion and major AI customers kept signing.

Q1 revenue was $2.078 billion, while Reuters said the company lifted the lower end of its 2026 capex guide to $31 billion, with the top end still $35 billion. That full-year capex range is about 15 to 17 times Q1 revenue, or roughly 3.7 to 4.2 times an annualized Q1 revenue run rate. The stock reaction showed investors are no longer valuing CRWV only as a scarce GPU-capacity provider. They are asking how much capital, debt and margin dilution it takes to turn backlog into cash flow.

Demand Still Looks Scarce, but the Stock Is Now Trading on Cost

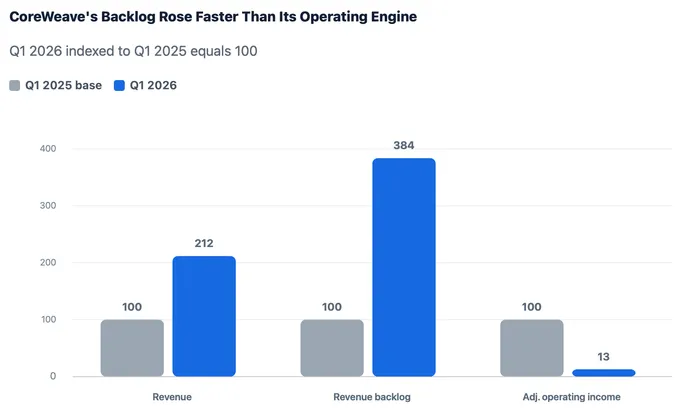

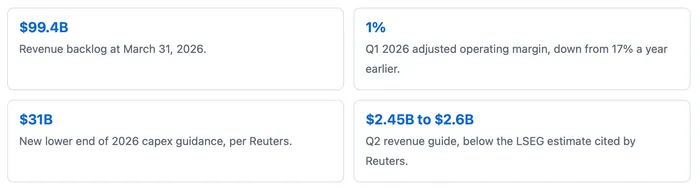

Demand still looks scarce. CoreWeave's Q1 release said revenue rose to $2.078 billion from $982 million a year earlier, and backlog expanded to $99.4 billion. Management also said the company surpassed 1 GW of active power and had more than 3.5 GW of contracted power.

That scale matters because AI labs and large enterprises are still competing for advanced compute. CoreWeave's customer list in the quarter included Meta, Anthropic, Cohere, Jane Street and Mistral, which gives the bull case enough evidence to argue that demand is broadening beyond one customer or one model cycle.

Market pricing, however, has moved past the easy part of the story. A high-growth AI infrastructure name can beat revenue expectations and still sell off if the next dollar of backlog requires too much debt, equipment spending, power commitment or depreciation before it produces durable operating profit or free cash flow.

Backlog Visibility Did Not Translate Into Operating Leverage

A clean growth story would show revenue and backlog rising while operating leverage followed. CoreWeave's quarter did not give investors that simple setup. Adjusted operating income fell to $21 million from $163 million, and adjusted operating margin fell to 1% from 17%.

Those figures do not mean the company lacks strategic value. They mean the market has less room to value CRWV only on contracted demand. As the installed base grows, investors need to see whether capacity goes live at attractive economics or whether higher component costs and infrastructure expenses keep absorbing the revenue ramp.

Source: stitched from CoreWeave Q1 2026 results and CoreWeave Q1 2025 results. Index basis: Q1 2025 equals 100. Revenue uses $2.078 billion versus $981.632 million; backlog uses $99.4 billion versus $25.9 billion; adjusted operating income uses $21 million versus $162.634 million.

Capex Is Several Times the Revenue Run Rate

Cost pressure moved to the center of the debate because CoreWeave raised the lower end of its 2026 capital expenditure forecast to $31 billion from $30 billion, while keeping the upper end at $35 billion, in the Reuters account. The same report said management cited component-price inflation.

The gap between capex and current revenue is the shock point. CoreWeave's full-year capex guide is nearly four times an annualized Q1 revenue run rate, and the Q1 cash-flow statement already shows the strain: $2.984 billion of operating cash flow was more than offset by $7.695 billion of purchases of property and equipment, including capitalized internal-use software. That leaves the buildout dependent on financing even when customers are paying and deferred revenue is rising.

The balance sheet explains why investors reacted to the guide. At March 31, CoreWeave had $7.547 billion of current debt and $17.312 billion of non-current debt, or roughly $24.9 billion combined. Operating lease liabilities added about $10.1 billion, and Q1 net interest expense was $536 million. Depreciation and amortization was $1.147 billion, which is why adjusted EBITDA can look robust while adjusted operating income stays thin.

CoreWeave's own March investor presentation shows the intended structure: asset-level delayed draw term loans fund most capex, secured by take-or-pay customer contracts, associated property and equipment, and data-center leases. Parent-level financing covers the rest through customer prepayments, operating free cash flow from stabilized contracts, ParentCo debt, OEM financings, convertibles or equity. That model can work if deployment is smooth. It becomes fragile if costs are incurred before revenue recognition and margin stabilization.

Q2 revenue guidance of $2.45 billion to $2.6 billion was below the LSEG analyst estimate of $2.69 billion. Even a small guide gap matters when the stock is valued on hypergrowth. It gives bears a way to argue that capacity buildout risk is arriving faster than clean operating leverage.

Customer Wins Keep the Bull Case Alive

Any bearish read has to deal with one strong counterpoint: customers are still signing. CoreWeave said Q1 included multiple agreements with Meta, including a $21 billion commitment, a multi-year deal with Anthropic, and expanded relationships with Cohere, Jane Street and Mistral.

Those contracts are important because they reduce the chance that CoreWeave's growth is just a one-cycle spike in training capacity. They also suggest customers want specialized cloud capacity as AI moves from model training into production inference, where availability, latency and operational tooling can matter as much as raw GPUs.

For investors, that creates a more balanced setup than the after-hours drop alone suggests. Large commitments support the growth floor, but they do not remove execution risk. CoreWeave still has to secure supply, manage power commitments, finance the buildout and bring capacity online at a pace that does not dilute the economics of the contract base.

The bull case therefore needs more than another customer announcement. It needs backlog-to-revenue conversion, higher utilization, adjusted operating margin repair, and evidence that customer diversity is improving faster than balance-sheet intensity. The bear case is equally specific: capex gets revised higher, margins stay compressed, financing costs remain heavy, and capacity delivery runs slower than contract growth.

The Next Test Is Utilization, Not Another AI Headline

Another AI customer win could still move CRWV, but the higher-quality validation point is operational. A better next quarter would show revenue guidance catching up to backlog growth, adjusted operating income recovering from the Q1 trough, and capex translating into visible capacity rather than simply a larger financing requirement.

Sequential backlog also matters. $99.4 billion at March 31 versus $66.8 billion at year-end shows how quickly contracted demand expanded. If that backlog continues rising while margins stay compressed, the market may keep splitting the story into demand strength and delivery cost. If margins improve with utilization, the same backlog can become valuation support again.

For now, CoreWeave has given investors enough evidence to keep believing in AI cloud demand and enough cost pressure to stop treating that demand as a clean equity positive. The stock's next durable move is likely to depend less on whether AI workloads are growing and more on whether CRWV can turn contracted demand into higher-margin capacity before the capex bill gets larger.