CRWV has quickly become one of the most important companies in the artificial intelligence infrastructure buildout, serving as a specialized cloud provider built specifically for AI workloads. The company rents out massive clusters of high-performance GPUs — primarily from NVIDIA — to AI labs, hyperscalers, and enterprises that are training and running large language models. CoreWeave sits directly in the middle of the AI compute arms race, providing the infrastructure layer powering many of the industry’s largest AI projects. That positioning has made the company one of Wall Street’s hottest AI infrastructure plays, with shares soaring nearly 80% this year entering earnings. However, the latest report highlighted a growing debate around whether explosive demand can offset mounting losses, rising infrastructure costs, and increasingly aggressive spending requirements. Shares are down roughly 10% following the report as investors digest weaker-than-expected guidance and another sharp increase in projected expenses.

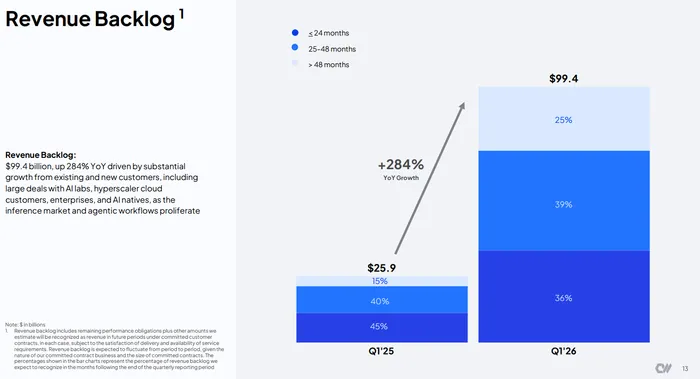

CoreWeave delivered a mixed first-quarter report that featured another massive revenue beat but also widening losses and disappointing near-term guidance. Revenue surged 112% year-over-year to $2.08 billion, ahead of analyst expectations near $1.97 billion. Adjusted EBITDA came in at $1.16 billion, roughly in line with expectations, while adjusted EBITDA margins landed at 56%. The company’s backlog also exploded higher, reaching $99.4 billion as of March 31, up from approximately $66.8 billion last quarter. Management noted that this was the strongest bookings quarter in company history, with more than $40 billion of new commitments signed during the period.

Despite the impressive top-line growth, profitability metrics were much weaker than investors hoped. Adjusted net loss widened to $589 million compared to expectations closer to $446 million, while GAAP net loss reached $740 million. Operating expenses surged to $2.22 billion from just over $1 billion a year ago as the company aggressively expanded infrastructure capacity and invested heavily in new deployments. Technology and infrastructure expenses rose even faster than revenue growth, reflecting the enormous cost associated with building out AI data centers packed with increasingly expensive GPUs and networking equipment.

Margins were another key concern. Adjusted EBITDA margin fell to 56% from 62% a year ago, while adjusted operating margin collapsed to just 1% from 17% last year. Gross margin pressure has become one of the biggest investor concerns surrounding the company. Management attempted to reassure analysts on the conference call by arguing that the margin compression is primarily timing-related rather than structural. CoreWeave explained that when it receives new powered data center shells, it immediately begins incurring lease, power, and depreciation expenses before revenue generation begins. According to management, these new deployments initially operate at negative contribution margins before normalizing several months later as customer workloads ramp. The company repeatedly stressed that Q1 represented the “trough” for margins and that profitability should sequentially improve throughout the remainder of the year.

Still, the market’s biggest disappointment centered around guidance. CoreWeave projected second-quarter revenue between $2.45 billion and $2.6 billion, below Wall Street expectations near $2.7 billion. While the company reaffirmed full-year revenue guidance of $12 billion to $13 billion, the midpoint still slightly trails analyst expectations. Investors also focused heavily on the company’s sharply rising capital expenditure forecast. CoreWeave raised its 2026 CapEx outlook to $31 billion to $35 billion, citing rising component pricing pressures throughout the AI infrastructure supply chain. Management acknowledged that shortages in critical components have intensified over the past six to nine months, though executives argued the company is largely insulated because it builds those costs directly into customer contracts.

Free cash flow and debt levels remain among the most controversial aspects of the CoreWeave story. The company continues to burn enormous amounts of cash as it races to expand infrastructure capacity. CoreWeave generated approximately $2.9 billion in operating cash flow during the quarter, but that was overwhelmed by roughly $7.7 billion in property and equipment spending. CapEx totaled $6.8 billion in Q1 alone as the company accelerated deployment schedules. To finance that expansion, CoreWeave has aggressively tapped debt markets, raising approximately $8.5 billion in new debt during the quarter while bringing total indebtedness to nearly $25 billion. Management highlighted that the company has now secured more than $20 billion in debt and equity financing year-to-date through heavily oversubscribed offerings.

Much of the conference call focused on supply chain constraints, pricing dynamics, and whether CoreWeave can sustain margins while scaling so aggressively. Analysts repeatedly questioned management about rising component prices and whether those costs could eventually squeeze profitability. CEO Michael Intrator argued that CoreWeave’s contracts are structured to pass through rising infrastructure costs while still targeting mid-20% contract-level margins. Analysts also pressed management on the massive second-half earnings ramp implied by the company’s guidance, particularly given relatively weak first-half operating income expectations. Management maintained that revenue and margin expansion should inflect sharply beginning in the third quarter as more deployments transition from buildout phase into active revenue generation.

Another major topic on the call was AI inference demand. Intrator revealed that more than 50% of CoreWeave’s compute capacity is now likely being used for inference workloads rather than training. That is significant because inference workloads represent the monetization phase of AI adoption, where customers are actively generating revenue from deployed AI models. Management also emphasized that demand remains extraordinarily strong across older NVIDIA Hopper and Ampere architectures in addition to newer Blackwell systems. CoreWeave stated that its H100 and A100 GPU fleets remain essentially sold out while pricing continues to rise quarter-over-quarter.

Wall Street analysts largely remained positive on the long-term story despite the stock reaction. Wells Fargo reiterated its Overweight rating and raised its price target to $155, while Jefferies maintained a Buy rating with a $160 target. Bulls continue pointing to the company’s nearly $100 billion backlog, multi-year contract visibility, and central role in the AI infrastructure buildout. However, skeptics argue the company’s valuation increasingly depends on flawless execution, sustained AI spending growth, and continued access to massive amounts of capital at favorable rates.

Technically, the stock now finds itself in an important position following the post-earnings selloff. Shares had staged a massive rally ahead of the report, meaning expectations entering earnings were already extremely elevated. The April 28 low near $110 is now becoming a critical support level traders are watching closely. A successful hold of that area could potentially set up a reflexive bounce given the stock’s strong AI momentum and aggressive institutional interest. However, a decisive break below that level would likely intensify concerns that investors are beginning to lose patience with the company’s accelerating spending, widening losses, and increasingly back-end-loaded profitability story.