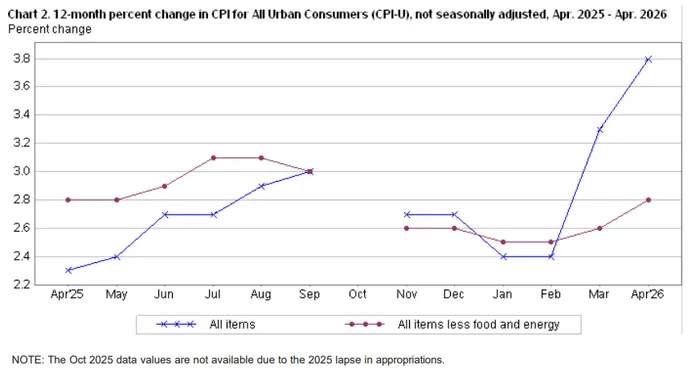

Wall Street received a mixed but increasingly concerning inflation report Tuesday morning as April consumer price data suggested the energy shock tied to the Middle East conflict may finally be spreading more broadly across the U.S. economy. However, the figures were cooler than expected which aided a bounce in the futures. Headline CPI rose 0.7% month-over-month, slightly above economist expectations near 0.6%, while annual CPI accelerated to 3.8% from 3.3% in March. Core CPI, which excludes food and energy, rose 0.4% month-over-month and 2.8% year-over-year, both modestly above expectations. Treasury yields initially moved higher ahead of the release, with the 10-year Treasury yield briefly pushing above the critical 4.40% level before stabilizing following the results. Meanwhile, the Nasdaq futures underperformed broader indices as investors reassessed the implications for Federal Reserve policy and high-multiple AI stocks. The dollar also strengthened modestly while oil prices remained elevated near four-year highs, reinforcing fears that inflation pressures are becoming more entrenched.

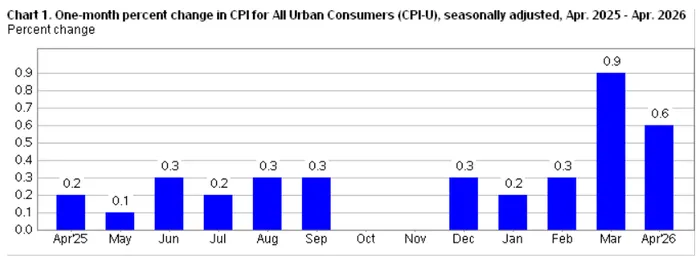

At the headline level, inflation continues to show clear acceleration compared to earlier in the year. February CPI rose just 0.2% month-over-month before surging 0.9% in March and remaining elevated at 0.7% in April. Core inflation has also begun reaccelerating after appearing relatively contained earlier this year, rising from 0.2% in February to 0.2% again in March before jumping to 0.4% in April. The broad takeaway is that inflation is no longer solely an energy story. March largely reflected a direct oil shock tied to higher gasoline prices, but April’s report suggests second-order effects are now emerging across transportation, services, and select goods categories. That distinction matters enormously for markets because energy-driven inflation is something the Federal Reserve can often look through temporarily, while broadening inflation pressures become much more difficult to ignore.

The CPI report showed that energy remained the dominant contributor to headline inflation, though the composition of inflation broadened noticeably in April. Energy prices rose another 4.8% month-over-month after surging 10.9% in March, while gasoline prices climbed an additional 6.1%. However, transportation services accelerated sharply, rising 1.1% month-over-month after a 0.5% increase in March and a 0.4% rise in February. Airfares also reversed higher, climbing 1.4% after falling in March, suggesting higher jet fuel costs are beginning to pass through into travel pricing. Apparel prices rose 0.6% following two consecutive softer months, while household furnishings and durable goods categories also firmed. Food prices remained relatively stable overall, but several packaged goods categories tied to transportation and freight costs showed renewed pricing pressure.

The broader implication is that higher oil prices may now be filtering through supply chains and service categories rather than remaining isolated to gasoline stations. Transportation services, freight-sensitive goods, and travel-related categories all showed renewed strength in April, reinforcing concerns about second-order inflation effects. Markets have spent the past several weeks debating whether the oil shock tied to the Iran conflict would remain transitory or eventually spread across the economy. Tuesday’s report did not fully answer that question, but it clearly suggested inflation breadth is increasing. That is especially important because services inflation tends to be significantly stickier than commodity inflation alone.

Shelter inflation was another major focus within the report, particularly Owners’ Equivalent Rent (OER), which many economists feared could begin reaccelerating. Table 1 showed shelter prices rising 0.5% month-over-month in April after increasing 0.4% in both February and March. OER specifically rose 0.6% in April versus 0.4% in March, while rent of primary residence increased 0.5%. Lodging away from home also jumped sharply, reflecting stronger hotel and travel demand alongside higher operating costs tied to energy and labor. The acceleration in OER is especially important because shelter remains one of the largest components of core CPI and heavily influences Federal Reserve thinking around underlying inflation persistence.

Markets care deeply about OER because it tends to move slowly and remain sticky once it begins accelerating. Unlike gasoline prices, which can reverse quickly if oil declines, shelter inflation typically persists for many quarters. That creates a difficult backdrop for the Fed because it suggests inflation pressures may remain elevated even if energy markets eventually stabilize. Several economists noted that April’s shelter data complicates the “Fed on hold” narrative that had recently supported equities and helped keep Treasury yields relatively contained.

Table 2 also provided evidence that the AI infrastructure boom and semiconductor supply chain pressures may increasingly be influencing goods inflation. Information technology commodities rose modestly in April after remaining largely flat earlier this year, while prices for computer-related equipment and certain electronics categories also firmed. Analysts increasingly believe higher memory pricing, semiconductor supply constraints, and rising data-center buildout costs are beginning to appear in select inflation-sensitive categories. The broader AI investment cycle has fueled enormous demand for advanced chips, networking equipment, power systems, and memory products, all of which could gradually influence broader goods pricing trends if supply constraints persist.

The market implications from the report are significant. The 10-year Treasury yield pushing above 4.40% is particularly important because many technical analysts view that area as a key breakout level that could trigger a broader repricing across risk assets if yields continue rising. While the CPI number is arguably better than feared, there are elements that suggest the Fed is a long way from cutting rates. Technology and AI-related equities remain especially sensitive because their elevated valuations depend heavily on contained discount rates and stable financial conditions.

At the same time, the report was not outright catastrophic for risk assets. Much of the inflation acceleration still remains tied directly or indirectly to energy markets, and some investors continue viewing the current oil shock as temporary rather than structurally inflationary. If tensions in the Middle East ease or shipping flows normalize, some of the transportation and commodity pressures could eventually moderate. Markets now expect very little probability of near-term rate cuts, while several Wall Street economists have already pushed their first-cut expectations well into 2027.

Ultimately, the April CPI report reinforced that inflation risks are becoming broader and more complicated. March largely looked like a pure energy shock, but April showed clearer signs that transportation, travel, shelter, and select goods categories are beginning to absorb those pressures. The Federal Reserve can tolerate temporary commodity volatility, but sticky shelter inflation and broadening services pressure create a much more difficult policy backdrop. Investors will now closely watch upcoming PPI data, retail sales figures, Treasury auctions, and further developments in oil markets and the Iran conflict to determine whether April represented the beginning of a broader inflation reacceleration or merely a temporary energy-driven flare-up.