US consumer inflation accelerated sharply in May as the Middle East energy shock pushed gasoline prices higher, but a softer-than-expected core reading offered some reassurance that price pressures have not yet spread broadly across the economy.

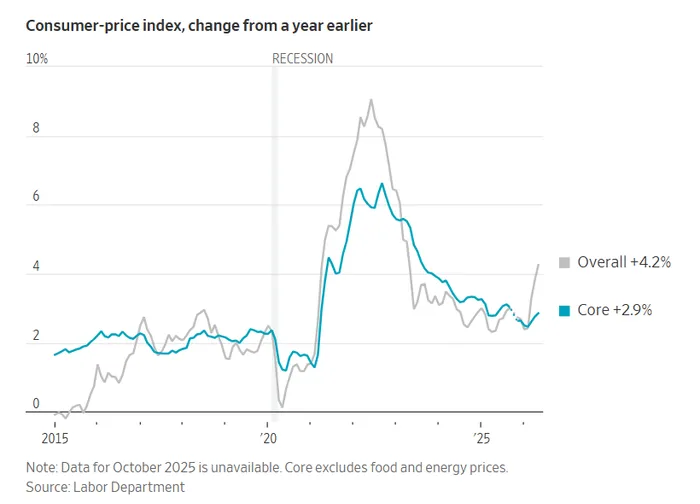

Headline CPI rose 4.2% year-over-year, matching the consensus forecast and climbing from 3.8% in April. This was the highest annual inflation rate since April 2023. On a monthly basis, headline CPI increased 0.5%, also in line with expectations and slightly below April's 0.6% gain.

Core CPI, which excludes food and energy, rose 2.9% year-over-year, matching expectations and edging up from 2.8% in April. More importantly, monthly core inflation increased just 0.2%, below the 0.3% consensus estimate.

The report therefore delivered two different messages. Consumers are facing the fastest overall inflation in more than three years, but the underlying data still look more like an energy and transportation shock than a broad inflation spiral.

Markets Take the Report in Stride

The market reaction was relatively muted because the headline figures matched forecasts and core monthly inflation came in softer than expected.

The 10-year US Treasury yield was around 4.528% shortly after the release, almost unchanged from 4.530% immediately before the data. US stock futures initially slipped but recovered part of their losses after investors concluded that the report contained no major upside surprise.

That calm reaction is significant. Markets had been highly sensitive to hawkish risks after a stronger-than-expected May jobs report raised concerns that the Federal Reserve might eventually need to resume rate increases. May's CPI report did not remove that risk, but it also did not intensify it.

Wages Fall Further Behind Inflation

Average hourly earnings increased 3.4% year-over-year in May, well below the 4.2% rise in consumer prices.

As a result, real earnings fell 0.7% from a year earlier and declined 0.1% during the month. Inflation has now outpaced wage growth for a second consecutive month, reducing the purchasing power of American workers.

The squeeze is especially difficult for middle-income households, which are more exposed to essential expenses such as fuel, food, and rent. Higher-income consumers are generally better positioned to absorb the increase, reinforcing the increasingly divided pattern of US consumer spending.

Energy Accounts for Most of the Inflation Surge

Energy was by far the largest inflation driver in May. The energy index increased 3.9% month-over-month and 23.5% from a year earlier, its biggest annual rise since August 2022. Energy accounted for more than 60% of the monthly increase in headline CPI.

Gasoline prices jumped 7.0% during the month and 40.5% year-over-year as the conflict in the Middle East disrupted supply chains and kept oil markets under pressure. Electricity prices rose 0.6%, while natural gas prices declined 0.5%.

The impact of higher fuel costs was also visible beyond the energy category. Airline fares increased 2.7% in May, showing how the oil shock is already feeding into travel-related inflation.

Food Inflation Cools, While Rent Remains a Pressure Point

Food prices rose 0.2% month-over-month, slowing from April's 0.5% increase. On an annual basis, food inflation stood at 3.1%.

The moderation provides some relief, but the outlook remains uncertain. Persistently high energy and transportation costs can eventually raise the cost of producing and distributing food, while supply disruptions could create additional pressure in coming months.

Housing costs also remain important. Bloomberg's live coverage highlighted that home rental prices continued to climb, suggesting shelter inflation is still limiting the improvement in core inflation even as several goods categories remain soft.

Goods Data Suggest Limited Second-Round Effects

The details outside energy were less alarming than the headline number. Motor vehicle insurance, household furnishings, and new vehicle prices were among the softer categories.

This matters because it suggests that the energy shock has not yet produced widespread second-round inflation. For now, higher prices are concentrated mainly in energy, transportation, and travel rather than spreading rapidly through the broader consumer basket.

The risk is that a prolonged oil shock changes that picture. Companies facing persistently higher fuel, shipping, and input costs may eventually pass more of those expenses on to customers.

Analysts: Softer Core CPI Offers Reassurance, but Cuts Remain Unlikely

Arielle Ingrassia of Evelyn Partners said the softer core reading offered some reassurance that inflation expectations had not become unanchored. That interpretation is consistent with the muted Treasury-market response.

Mark Hamrick of Bankrate warned that inflation could remain elevated in the near term because Middle East supply-chain disruptions are likely to keep pressure on prices. If energy costs remain high, wage growth may continue to lag inflation and household purchasing power could weaken further.

The report is unlikely to change the Federal Reserve's immediate policy stance. Before the release, futures markets assigned a 98% probability that rates would remain unchanged at the June 17 meeting. Headline inflation at 4.2% gives the Fed little reason to consider rate cuts, while the softer core figure and limited evidence of broader pass-through reduce the urgency for an immediate hike.

The most likely outcome is an extended pause. The Fed can tolerate a temporary energy-driven rise in inflation, but only if core inflation remains contained and inflation expectations stay anchored. A prolonged oil shock or broader price pass-through would make that position increasingly difficult to defend.