Deere & Company (DE) delivered another earnings beat Thursday morning, but investors clearly decided that was not enough to offset mounting concerns surrounding the global agricultural cycle, rising input costs, and a stock that had already been deteriorating technically ahead of the report. Shares of Deere were down roughly 4% in early trading despite topping Wall Street expectations on both earnings and revenue while maintaining its full-year guidance. The reaction highlights the increasingly difficult backdrop facing agricultural equipment manufacturers as farmers contend with higher fertilizer, fuel, and financing costs at a time when crop profitability remains pressured. It also reinforces that investors were looking for something more than simply “better-than-feared” results after Deere stock had already fallen sharply from roughly $674 to near $560 in the weeks leading into earnings.

From a headline perspective, the quarter itself looked quite strong.

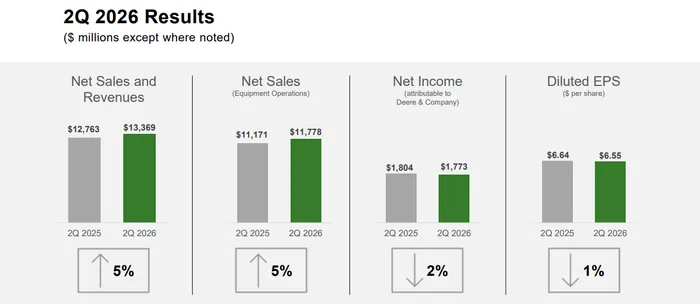

Deere reported fiscal second-quarter adjusted EPS of $6.55, comfortably above analyst expectations near $5.70-$5.81. Equipment sales reached $11.78 billion, well ahead of consensus estimates around $10.3-$11.5 billion and up from $11.17 billion a year ago. Worldwide net sales and revenue rose 5% year-over-year to $13.37 billion.

Net income came in at $1.77 billion, or $6.55 per share, compared with $1.80 billion, or $6.64 per share, in the prior-year quarter. While profits declined slightly year-over-year, the result still represented a major operational outperformance relative to investor expectations.

So why is the stock trading lower?

The answer largely comes down to the broader agricultural backdrop and concerns that Deere’s earnings power may have already peaked for this cycle.

The biggest headwind remains farmer profitability.

Although corn prices have stabilized somewhat around $4.70 per bushel versus roughly $4.40 at the end of 2025, fertilizer prices and fuel costs have surged following the war with Iran and the sharp rise in energy prices. Fertilizer production remains heavily dependent on oil and natural gas, meaning higher crude prices directly pressure farm economics.

At the same time, the USDA now expects U.S. farm income to remain roughly flat in 2026 near $153 billion, well below the record $182 billion reached in 2022. That matters enormously because Deere’s large agricultural equipment business is highly dependent on strong farm profitability and confidence. Flat farm income may be manageable, but it does not create the kind of aggressive replacement cycle that investors typically want to see for large-ticket farm machinery purchases.

Investors also appear increasingly concerned that the agricultural downcycle may persist longer than expected.

That concern was visible directly inside Deere’s largest business segment.

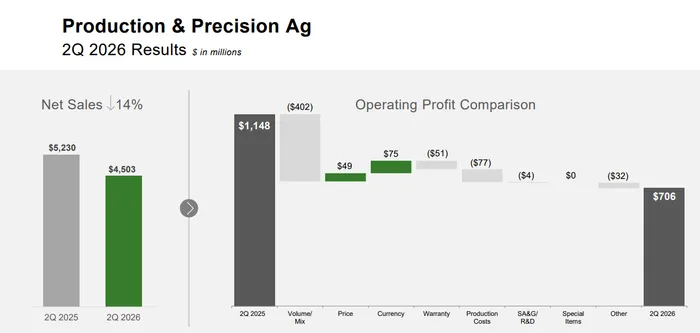

Production & Precision Agriculture revenue fell 14% year-over-year to $4.50 billion, while operating profit plunged 39% to $706 million. Operating margin compressed sharply to 15.7% from 22.0% a year ago.

Management said the decline was primarily driven by lower shipment volumes and higher production costs, partially offset by favorable currency effects. In other words, Deere is still facing meaningful weakness in demand for large agricultural equipment — arguably the single most important part of the company’s long-term earnings profile.

This is likely the core reason the stock is struggling despite the headline beat.

The market appears less focused on the quarter itself and more focused on what the deterioration inside large agriculture implies about the next 12-18 months.

However, there were several major bright spots inside the report.

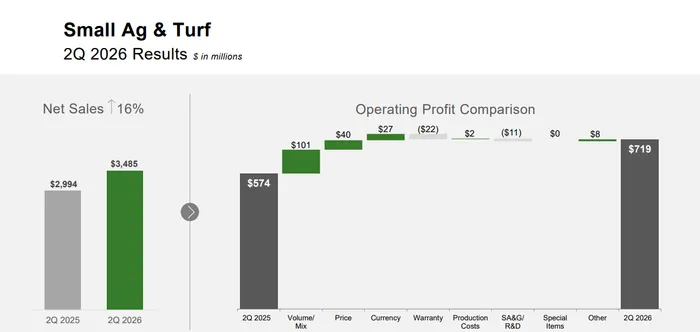

Small Agriculture & Turf delivered very strong results, with revenue rising 16% year-over-year to $3.49 billion while operating profit jumped 25% to $719 million. Operating margin improved to 20.6% from 19.2% last year. Deere attributed the strength to higher shipment volumes and favorable pricing realization.

That segment has increasingly become an important stabilizer for Deere because it is less dependent on large commercial farming activity and more tied to smaller farms, landscaping, residential, and turf-related demand.

Construction & Forestry was arguably the strongest segment in the entire report.

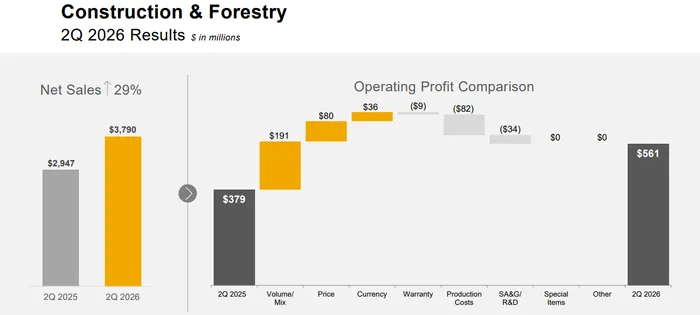

Revenue surged 29% year-over-year to $3.79 billion while operating profit jumped 48% to $561 million. Operating margin expanded to 14.8% from 12.9% a year ago.

Management said growth was driven by higher shipment volumes, pricing realization, and stronger overall demand trends. Construction equipment markets in North America remain relatively healthy, particularly in infrastructure-related categories and compact equipment. That strength helped partially offset weakness within large agriculture.

Importantly, Deere also maintained its full-year guidance despite ongoing macro uncertainty.

The company reiterated fiscal 2026 net income guidance of $4.5 billion to $5.0 billion, signaling management still believes the business can navigate current agricultural weakness without a major deterioration in profitability.

CEO John May attempted to strike a balanced tone on the call.

He acknowledged that customers continue facing significant challenges within global agricultural markets but emphasized that Deere’s diversified portfolio, dealer network, and ongoing investments in technology continue supporting long-term market share gains and operational resilience.

The industry outlook itself, however, still reflects meaningful caution.

For fiscal 2026, Deere expects:

U.S. and Canada Large Ag markets down 15%-20%

South American tractor and combine markets down roughly 15%

Global forestry markets down roughly 5%

Those forecasts reinforce the idea that agricultural equipment demand remains in a cyclical slowdown phase despite some stabilization in crop prices.

There was also an interesting one-time item buried inside the report tied to tariffs.

Following a Supreme Court decision invalidating certain IEEPA tariffs, Deere recorded a $272 million recovery tied to previously filed refund claims accepted by U.S. Customs and Border Protection.

From a valuation perspective, Deere still trades at a premium relative to peers despite the recent correction.

The stock currently trades near roughly 27x forward earnings compared to approximately 20x for CNH Industrial (CNH) and roughly 17x for AGCO Corporation (AGCO). That premium likely reflects Deere’s superior technology positioning, precision agriculture investments, and stronger long-term margins. However, it also leaves the stock vulnerable during periods of cyclical uncertainty.

Ultimately, the market reaction appears less about the quality of the quarter and more about lingering uncertainty surrounding the agricultural cycle itself. Deere still executed well operationally, Construction & Forestry remained extremely strong, and management maintained guidance. But until investors gain confidence that farm profitability and large agricultural demand are stabilizing, Deere stock may continue struggling to regain momentum despite continued earnings beats.