Dell shares rose around 39% in extended trading on Thursday, May 28, after fiscal first-quarter results made the AI server boom visible in reported revenue, not only in backlog language. The company said record revenue reached $43.8 billion, up 88% year over year, while AI orders totaled $24.4 billion and AI server revenue reached $16.1 billion.

Before the release, the market already had a friendly tape, with the S&P 500 and Nasdaq closing at records on May 28. Dell's result added a more specific message for the AI hardware chain. Revenue recognition, annual guidance and segment profit now matter more than broad enthusiasm for data-center spending.

AI server demand reached the income statement

Reported demand was concentrated in Infrastructure Solutions Group, where Dell said revenue rose 181% to $29.0 billion and operating income rose 206% to $3.1 billion. Within that segment, AI-optimized server revenue was $16.1 billion, up 757% year over year, alongside $8.5 billion from traditional servers and networking and $4.3 billion from storage.

Those figures change the way the Dell move should be read. A backlog story asks whether orders eventually convert. A quarter with $16.1 billion of AI server revenue and faster ISG operating-income growth gives the stock reaction an operating anchor, even if full-year delivery timing remains unsettled.

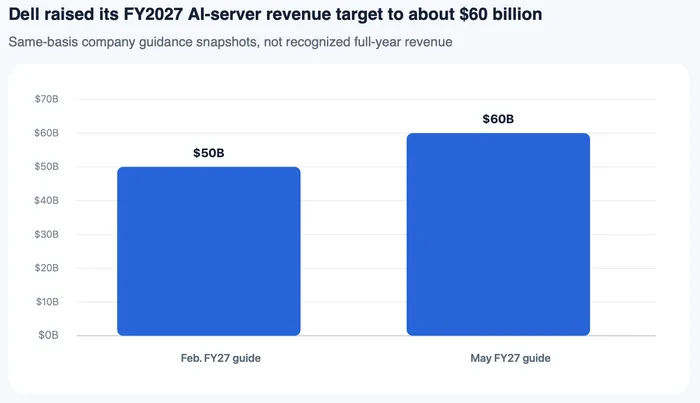

The $60 billion target lifts the operating bar

February's full-year setup was already aggressive. Dell's prior fiscal 2027 guide called for roughly $50 billion of AI-optimized server revenue. By May 28, the company had lifted that target to roughly $60 billion, after a first quarter that already delivered roughly 27% of the new annual figure.

Source note Dell Technologies ticker DELL; source scope is stitched from the fiscal 2026 fourth-quarter release and fiscal 2027 first-quarter release; date range February 26, 2026 to May 28, 2026; interval company guidance snapshots; basis FY2027 AI-optimized server revenue outlook. Visible values compare February guidance with May guidance.

At that scale, the debate shifts from whether demand exists to whether Dell can keep enough supply moving through the year. A $60 billion annual AI server target requires more than one strong quarter. It requires component availability, customer scheduling and pricing discipline to hold together through the second half.

Memory pricing keeps the margin question open

Strong revenue does not automatically settle the economics. Reuters reported that Dell was managing memory-chip pressure through price increases and supply-chain adjustments, and the same report cited management's comments about frequent repricing in an inflationary environment.

Dell's Q1 segment profit gives the constructive side of the debate more evidence. ISG operating income rose faster than ISG revenue, and the company guided fiscal second-quarter revenue to $44.0 billion to $45.0 billion. The unresolved issue is how much of the AI server mix can keep flowing into operating income if memory availability, customer urgency or component costs change.

Hardware peers carry different parts of the AI chain

Peer signals should stay role-specific. Reuters said U.S. tech giants including Alphabet and Amazon plan to spend over $700 billion on AI infrastructure this year, supporting demand for server and data-center equipment from suppliers such as Dell and Super Micro Computer. That does not make Dell, Super Micro and Nvidia the same exposure.

Nvidia remains the accelerator and data-center platform center, with record Data Center revenue of $75.2 billion in its latest quarter. Dell's angle is different. The company packages GPUs, networking, storage and services into systems that customers can deploy. Super Micro is a server peer and demand proxy, but without Dell's Q1 release in hand, it should not be treated as carrying the same margin profile.

Next numbers need to show supply catching demand

Validation now sits in a short list of company disclosures. Dell's $44.0 billion to $45.0 billion second-quarter revenue guide is the nearest revenue checkpoint, while the $60 billion AI server target makes order cadence, backlog language, ISG operating margin and memory supply commentary more important than another broad AI demand statement.

More AI server revenue can keep the stock linked to the data-center buildout. A weaker margin path, slower order intake or signs that the after-hours jump pulled too much future revenue into one session would make the repricing harder to sustain. For now, Dell has given the market a concrete operating number to argue about.