Dell Technologies delivered what may ultimately be remembered as the most impressive earnings report of the season, blowing past Wall Street expectations by an extraordinary margin and forcing analysts to dramatically raise their forecasts. The stock had already been one of the best performers in the market heading into the release, rallying sharply over the previous several sessions on optimism surrounding AI infrastructure demand, the company's recent Pentagon contract win, and positive read-throughs from Lenovo's earnings. Yet even after a massive run that left shares more than 150% higher in 2026 and trading roughly three standard deviations above their 200-day moving average, Dell still managed to surprise investors.

The magnitude of the earnings beat was staggering . Dell reported first-quarter revenue of $43.84 billion, crushing consensus estimates of approximately $35.4 billion. Adjusted earnings per share came in at $4.86 versus expectations of just $2.94. Revenue surged 88% year-over-year, marking the fastest growth period since Dell returned to the public markets, while adjusted EPS increased 214% from the prior year. Just as importantly, management significantly raised both near-term and full-year guidance, signaling that this was not simply a one-quarter anomaly.

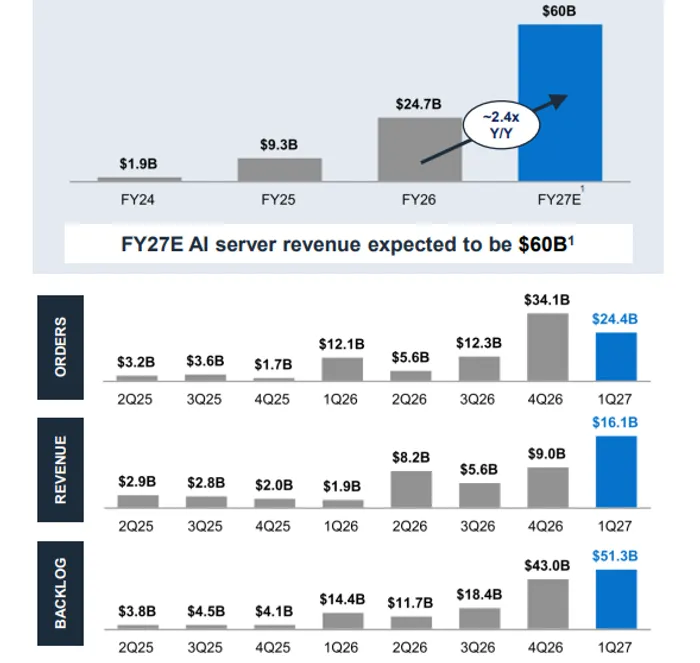

The primary driver behind the blowout performance remains artificial intelligence infrastructure. Dell reported AI-optimized server revenue of $16.1 billion during the quarter, representing growth of 757% from a year ago. AI orders booked during the quarter totaled an incredible $24.4 billion, while backlog expanded to a record $51.3 billion. Management noted that demand continues to exceed supply and repeatedly emphasized that the company is constrained by component availability rather than customer demand.

Chief Operating Officer Jeff Clarke described demand as stronger than anticipated across all geographies and business lines. Management highlighted increasing adoption from hyperscalers, sovereign customers, enterprises, neo-cloud providers, and AI startups. Dell also expanded its ecosystem relationships with partners including Nvidia, Google Cloud, OpenAI, Palantir, ServiceNow, CrowdStrike, Mistral, and xAI. The company continues positioning its Dell AI Factory as one of the primary enterprise deployment platforms for large-scale AI workloads.

The Infrastructure Solutions Group was the clear star of the quarter. Revenue within the segment surged 181% year-over-year to a record $29.0 billion, far exceeding analyst expectations. AI servers generated $16.1 billion of revenue, but investors should not overlook the strength elsewhere in the business. Traditional Servers and Networking revenue increased 92% to $8.5 billion, while Storage revenue rose 8% to $4.3 billion. Management repeatedly highlighted that agentic AI and inference workloads are increasing demand not only for GPUs but also for traditional compute, networking, and storage infrastructure.

This broad-based strength may be one of the most important takeaways from the quarter. Several analysts noted that investors had expected AI demand to be strong, but the true surprise came from traditional server demand. Dell reported that many enterprise customers remain on 14th-generation server platforms and are beginning large-scale refresh cycles that bypass intermediate generations entirely. This dynamic is creating a powerful upgrade cycle alongside the AI buildout.

Dell's Client Solutions Group also delivered a much stronger-than-expected performance. Revenue increased 17% to $14.6 billion, ahead of consensus expectations. Commercial client revenue rose 18% to $13.0 billion while consumer revenue increased 9% to $1.6 billion. Operating income within the segment jumped 79% year-over-year. Some analysts questioned whether these margins are sustainable, but management attributed the strength to disciplined pricing, favorable mix, operating leverage, and improved execution.

Margins remain a closely watched topic because AI servers typically carry lower gross margins than traditional enterprise infrastructure. Dell reported a gross margin rate of 18.1%, with management noting that the AI mix created pressure. However, excluding AI server mix effects, gross margins actually improved. Operating leverage helped offset this pressure, with operating income increasing 154% and operating margin expanding to 9.7%.

Free cash flow was another standout. Dell generated a record $4.1 billion in operating cash flow during the quarter and produced approximately $3.2 billion in adjusted free cash flow. The company returned $2.1 billion to shareholders through dividends and buybacks. Analysts increasingly view Dell as an AI infrastructure company capable of generating substantial cash rather than merely a low-margin hardware vendor.

Guidance was arguably just as impressive as the quarterly results. Dell expects second-quarter revenue between $44 billion and $45 billion, dramatically ahead of analyst expectations near $35 billion. Adjusted EPS guidance of approximately $4.80 also comfortably exceeded consensus estimates.

For fiscal 2027, Dell now expects revenue between $165 billion and $169 billion, compared with its prior forecast of $138 billion to $142 billion. Adjusted EPS guidance increased to roughly $17.90 from previous expectations near $12.90. The company also raised its AI server revenue outlook to approximately $60 billion, up from the prior target of $50 billion.

The primary concern investors continue to monitor is supply. Management repeatedly cited memory as the largest constraint, followed by NAND, microprocessors, and hard drives. Clarke emphasized that Dell does not have a capacity problem and does not have a demand problem. The challenge remains obtaining enough components to satisfy customer orders. While this creates some risk around quarterly timing, it also suggests that demand remains exceptionally robust.

From a technical perspective, Dell's stock has entered rare territory. The shares had already been climbing aggressively ahead of earnings before exploding higher following the report. Trading roughly three standard deviations above the 200-day moving average highlights just how extended the stock has become. While such conditions often lead to consolidation periods, analysts across Wall Street appear increasingly convinced that Dell is one of the clearest beneficiaries of the AI infrastructure supercycle.

The debate heading forward may no longer center on whether Dell can reach management's fiscal 2027 targets. Instead, investors are beginning to ask whether those numbers are still too conservative. If AI demand remains supply constrained rather than demand constrained, Dell's current guidance may prove to be another waypoint rather than a final destination.