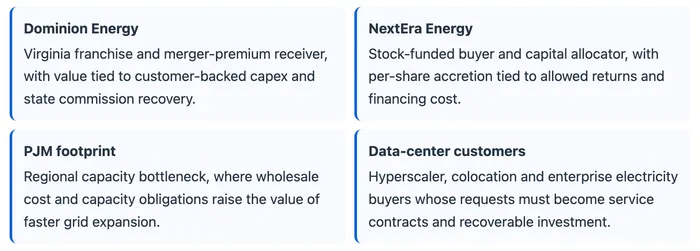

NextEra Energy agreed to buy Dominion Energy in a $66.8 billion stock-for-stock transaction on May 18, turning Northern Virginia electricity scarcity into a utility-finance problem. The tape split quickly, with Reuters reporting that Dominion rose about 10% while NextEra fell about 5%.

AI data-center demand does not lift utility earnings by itself. Dominion's rise reflects the merger premium and Virginia franchise scarcity, while NextEra's drop reflects dilution, regulatory concessions and execution burden. The next share-price inputs are the deal spread, rating-agency reaction, commission conditions and whether data-center demand lands in recoverable capex.

Share Issuance Comes Before Accretion

Under the exchange ratio, Dominion holders receive 0.8138 NextEra shares for each Dominion share, with existing NextEra owners expected to hold about 74.5% of the combined company and Dominion holders about 25.5%, according to the company announcement. Existing NextEra holders keep control, but they give Dominion holders a quarter of the future company before the acquired franchise adds any regulated recovery under NextEra ownership.

NextEra and Dominion say the all-stock transaction should be immediately accretive to adjusted EPS at closing and support 9% plus adjusted EPS growth through 2032. The bridge from issuance to accretion runs through the $138 billion combined rate base, expected 11% annual growth in regulatory capital employed, financing costs, commission conditions and the buyer's ability to fold Dominion projects into its construction and funding platform.

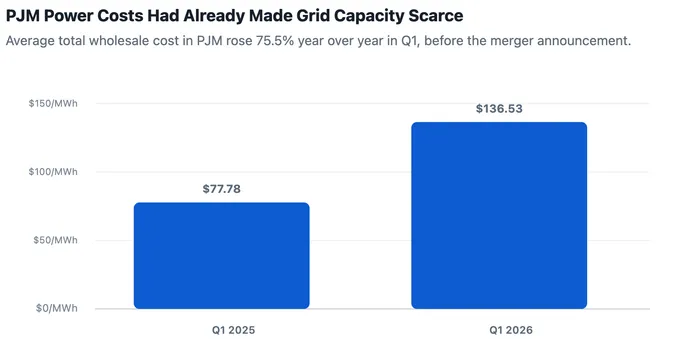

The chart uses Monitoring Analytics Q1 2026 PJM State of the Market data (source) and the Monitoring Analytics market-monitor release (source).

PJM Bottlenecks Raise Virginia Franchise Value

Dominion's geography matters because Northern Virginia is one of the most important data-center clusters in the U.S. power market. AP reported that Dominion provides regulated electric service in Virginia, North Carolina and South Carolina, plus regulated natural gas service in South Carolina. The acquisition gives NextEra broader exposure to PJM through Dominion's Virginia footprint, where new data-center demand is stressing capacity planning.

PJM's market backdrop gives that geography a price signal. Monitoring Analytics reported average total wholesale power cost at $136.53 per MWh in Q1 2026, up from $77.78 per MWh a year earlier, while its market-monitor release tied new data-center demand to substantial capacity obligations. Higher regional power costs do not make every megawatt a profit stream, but they make a constrained utility franchise more valuable to a buyer that can finance generation, transmission and grid upgrades.

Large-Load Numbers Split Into Different Stages

The large-load numbers describe different stages, not one revenue bucket. Reuters cited more than 130 GW of large-load opportunities across the combined footprint and nearly 51 GW of contracted data-center capacity at Dominion. Dominion's own large-load report separately says it proceeds project by project, based on confirmed and contracted demand forecasts, and had assigned energization dates to 25 GW of new data centers through 2031 while another 45 GW did not yet have future connection dates.

The same report describes a contracting ladder that matters for shareholder return. A Construction Letter of Agreement authorizes construction, triggers cash deposits and requires customer reimbursement if a project is canceled before energization. An Electric Service Agreement then sets how the customer takes service and how costs are recovered, including revenue requirements even if the customer does not take service.

That staging matters because contracted capacity, queue position and energization dates do different financial work. A signed service arrangement can support cost recovery; an undated request still depends on interconnection work, generation or transmission approval and large-load tariff treatment.

Bill Credits And Debt Shape The Return Burden

The $2.25 billion of customer bill credits lowers political friction, but it is also value that must be absorbed by the combined company over two years after close. The companies frame those credits beside operating, procurement, construction and financing efficiencies, so the accretion path depends on whether those efficiencies arrive fast enough to offset customer credits, integration cost and a larger capital program.

Dominion also brings a balance sheet that already carries utility-finance pressure. Its first-quarter 10-Q showed balance-sheet total long-term debt of $45.110 billion, including securitization bonds, junior subordinated notes and other long-term debt items, plus short-term debt of $3.098 billion and accrued capital expenditures of $1.107 billion at March 31, 2026. The filing says short-term debt funds working capital and bridges long-term debt financings, and interest-rate exposure is tied to outstanding and future debt.

NextEra says the combination should improve its credit rating thresholds and help Dominion and Dominion Energy Virginia with financing costs. The financing benefit is therefore not cosmetic. If ratings agencies, state commissions or customer-credit commitments narrow it, the stock-funded acquisition becomes harder to turn into per-share earnings.

Allowed ROE And Alternative Power Routes Set The Payoff

Shareholder return depends less on physical megawatts than on the regulatory compact around them. Dominion's 10-Q describes Virginia biennial reviews of earned returns on base-rate generation and distribution services, plus prospective rate-base setting for future periods. Closing will also require Dominion and NextEra shareholder votes, FERC approval, NRC approval and state commission review, with the companies targeting a 12 to 18 month timetable.

Virginia is not the only route for AI compute growth. Hyperscalers and colocation operators can phase campuses across other grid regions, sign with independent power producers, add behind-the-meter generation, or support nuclear, gas, renewables and transmission projects outside Dominion's franchise. PJM bottlenecks raise the value of a constrained node, but they also give new campuses a reason to compare faster interconnection, available generation and friendlier state calendars elsewhere.

The watch points are narrower than the AI-power headline. Deal spread, rating-agency reaction, Virginia SCC conditions, bill-credit treatment, large-load tariff approvals and PJM capacity or connection-queue changes will matter more than another broad data-center demand update.