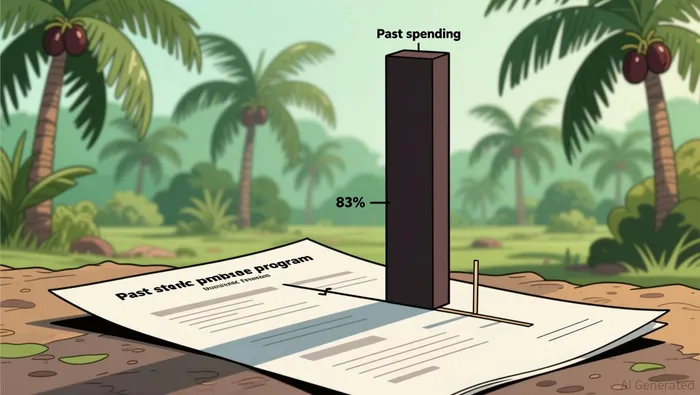

The programme shrank 83%. No one has noticed.

M.P. Evans Group, the AIM-listed Indonesian palm oil producer, is announcing another round of share cancellations. On June 8, the company confirmed it had repurchased and cancelled 15,605 shares at an average of 1,480 pence each. The ticker has been busy: 12,626 shares on May 31, 12,547 on June 1, 2,501 on June 3. The press releases stack up. The message is supposed to be capital discipline.

Look at the programme budgets and the message inverts.

In June 2025, M.P. Evans announced a share buyback programme of up to £12 million. This year, on May 26, the new programme is £2 million. That is an 83% reduction. The company does not get a headline for trimming its own capital return while it sits on record profits, a debt-free balance sheet, and commodity prices near cyclical peaks.

Why the budget collapsed is the real story

For a commodity producer, buyback size is a proxy for management's conviction about where prices are heading. You buy back aggressively when you think the market is undervaluing your future cash flows. You pull back when you see the other side coming.

M.P. Evans delivered a record year in 2025. Revenue hit $371 million. Gross profit rose 22% to $142.2 million. Operating cash flow was $161.5 million. The company repaid $32.5 million of debt and paid $38.7 million in dividends. It is now debt-free.

Against that backdrop, a £2 million buyback on a £772 million market cap represents 0.26% of market value. Last year's £12 million programme was 1.5%. Either way, these are cosmetic. But the direction of travel - from £12M to £2M - is the data point that matters.

Management's explanation, in their own words, is that the board considers shares "undervalued." They then allocated a budget that will take months to spend at the current pace. At roughly £190,000 per weekly transaction batch, the £2 million will last 10+ weeks. That is not how you act when you believe your stock is a screaming buy.

The commodity cycle does not care about your buyback programme

Here is what M.P. Evans cannot engineer away: it is a crude palm oil producer. Its revenue is a function of two variables - volume and price - and it controls neither in any meaningful sense.

CPO prices are near record levels. As of early June 2026, palm oil traded at 4,575 ringgit per tonne, up 16.6% year-over-year. M.P. Evans confirmed crop volumes are up 10% in early 2026 and selling prices are close to last year's record levels. That is why profits are record.

But S&P Global flagged in January that palm oil prices are expected to weaken in 2026. Indonesia is set for a production recovery, with CPO output projected to increase by 1.5–2.0 million tonnes from 2024 levels. More supply enters the market while biofuel policy support remains uncertain. The analyst consensus CPO price range for 2026 is $800–950 per tonne, below 2025's elevated realized prices.

M.P. Evans' revenue model is sensitive to this range. A move from $1,100/tonne to $850/tonne is not a "minor adjustment" - it is a step change that erases the margin expansion that made 2025 a record year.

The per-share mathematics

The company's total share count sits at approximately 52.19 million shares. The cancelled shares in this programme total around 43,000 so far - 0.08% of the float. The buyback is a rounding error.

What is not a rounding error is the share price trajectory. M.P. Evans shares hit a 52-week high of 1,918 pence and are now trading near 1,474 pence. The buybacks have been executed between 1,480p and 1,539p - in the lower part of the recent range. Management is not overpaying. But they are also not buying enough to make the programme a statement.

The annual dividend of £0.60 per share yields roughly 3.4%. Over the past five years (FY2020–2024), the dividend grew at a 21.6% compound annual rate. The dividend has been the real vehicle for capital return, not the buyback. As CPO prices normalize, that dividend sustainability becomes the question.

The cross-currents

The case for the stock is not that the buyback is impressive. It is that M.P. Evans is debt-free, operating at scale across 66,100 hectares of plantation land, and expanding. If CPO prices hold in the $900–1,000 range, earnings remain robust and the low P/E of 9.4 looks cheap. The company has demonstrated real operating leverage.

The case against it is simpler: the company cut its own stated conviction by 83% in one year. Management sees the commodity cycle turning and is hedging by returning less capital to shareholders. The buyback programme is too small to move the share count and too small to signal confidence. What it signals is caution.

The cross-currents are: palm oil prices at cyclical highs but forecast to weaken, a debt-free balance sheet that provides a margin of safety, and a buyback programme that tells you management is no longer convinced the stock is cheap.

Directionally, the buyback shrinkage is the leading indicator. Commodity traders price the CPO curve six months out. Management priced the earnings impact twelve months ago when they set the 2025 programme at £12 million, and they repriced it again when they cut this one to £2 million.

If the board believed the stock was undervalued, it would not have reduced its bid by five-sixths.

The stock at 9.4 times trailing earnings looks attractive only if earnings power is stable or growing. For a commodity producer, that requires stable or rising commodity prices. The market is telling you it doesn't. Neither is management.

The implication is straightforward: treat the share cancellation announcements as window dressing. The real capital allocation signal is in the programme budgets. The budget told you everything. Most investors skimmed the press release and missed it entirely.