Next week's Federal Reserve meeting may not produce an interest rate change, but it could still rank among the most important policy meetings in years.

The June 16-17 Federal Open Market Committee meeting marks the first chaired by Kevin Warsh, ushering in what many investors expect to be a significant shift in how the central bank communicates, operates, and potentially conducts monetary policy. While markets overwhelmingly expect the Fed to leave its benchmark interest rate unchanged at 3.50%-3.75%, the focus will be squarely on Warsh's first press conference, the updated Summary of Economic Projections (SEP), and any clues regarding his promised "regime change" at the institution.

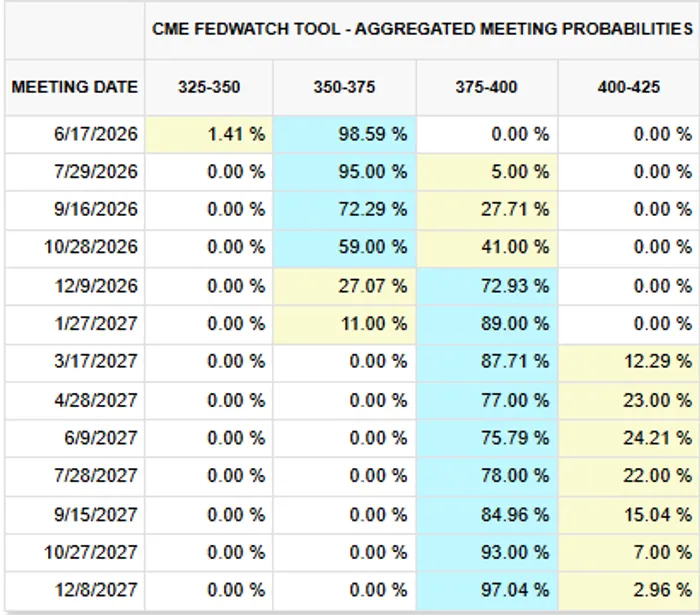

The market has already made its decision on rates.

Fed funds futures imply almost no chance of action next week, and investors have steadily pushed expectations for the next move further into the future following this week's inflation reports. The first hike is now largely expected around the December meeting, while expectations for a second increase are no longer on the table.

That represents a shift from only a few weeks ago when investors feared a much more aggressive tightening cycle.

The decline is notable given the combination of stronger-than-expected labor market data and rising inflation readings. Headline CPI accelerated to 4.2% year-over-year in May while core inflation rose 2.9%. Producer prices also remained elevated, reinforcing fears that inflation was becoming more entrenched.

However, a deeper look at the data suggests much of the pressure remains concentrated in energy-related categories.

The monthly pace of both headline and core inflation actually moderated versus April, and oil prices have since collapsed sharply as traders increasingly price in the possibility of a diplomatic breakthrough between the United States and Iran. WTI crude has fallen to its lowest level in roughly two months, raising the possibility that May's inflation report ultimately marks the peak of this latest inflation scare.

That distinction is important.

The Fed's concern is not simply whether inflation is elevated today, but whether it becomes embedded across the broader economy. Thus far, much of the acceleration remains linked to fuel, transportation, and supply-chain-sensitive categories rather than a broad-based wage-price spiral.

That gives Warsh some breathing room.

While inflation remains above target, the latest CPI and PPI reports likely reduce the urgency for any immediate policy response. The result is a Fed that can afford to wait, observe incoming data, and begin shaping its longer-term strategy.

That strategy may look very different from the Powell era.

Perhaps the most closely watched element of next week's meeting will be whether the Fed even continues to provide the same level of forward guidance that investors have grown accustomed to over the past decade.

Warsh has repeatedly criticized the central bank's communication framework, arguing that excessive forward guidance reduces policy flexibility and encourages markets to become overly dependent on Fed forecasts. He has questioned the usefulness of the quarterly Summary of Economic Projections and the famous "dot plot," which shows where individual policymakers expect rates to move in coming years.

As a result, next week's release could potentially become one of the final versions of the SEP in its current format.

Few expect Warsh to eliminate the dot plot immediately. Such a move would likely require broader committee support, and many policymakers value the ability to communicate their individual views. However, investors should pay close attention to any changes in language, presentation, or emphasis.

Even modest adjustments could signal a broader shift toward less transparency and greater policy discretion.

Many economists believe one of Warsh's first moves will be to reduce the amount of forward guidance embedded in the Fed's official statement. Several committee members have already expressed discomfort with language suggesting the next move would likely be a rate cut. Following stronger inflation data and resilient labor markets, that guidance increasingly appears outdated.

In fact, many analysts expect the Fed to either remove the easing bias entirely or adopt a more neutral stance.

The message would be simple: future policy decisions will depend on incoming data rather than predetermined forecasts.

That approach would represent a major departure from the Powell era, where the Fed frequently signaled policy intentions months in advance.

Investors will also be watching for any discussion surrounding the Fed's balance sheet.

Warsh has been a vocal advocate of a smaller balance sheet and has argued that the central bank's massive ownership of Treasury securities distorts capital allocation and financial markets. While meaningful balance sheet reductions are unlikely in the near term, next week's meeting could offer the first clues regarding how aggressively Warsh intends to pursue that objective.

Most economists believe any major changes remain several years away.

The Fed's balance sheet is already constrained by the banking system's demand for reserves, and significant reductions would likely require extensive study, regulatory changes, and committee consensus. Nevertheless, investors should listen carefully for any comments that indicate balance sheet normalization is becoming a higher priority.

Beyond the policy specifics, the press conference itself may be the most important event of the week.

Markets know the Fed is not hiking rates next week.

Markets know the Fed is unlikely to cut rates anytime soon.

What they do not know is who Kevin Warsh will be as Fed Chair.

Will he emerge as the dovish figure many expected during his nomination process? Or will he embrace the more hawkish posture currently favored by much of the committee?

The answer may determine how investors interpret monetary policy for the next several years.

There is also a certain nuance in the language a Fed Chair uses that the market becomes accustomed to. When there is a change in the Chair there tends to be a learning curve in which the new Chair makes a statement that appears reasonable to them and the committee, but that the market views differently and thus, reacts more aggressively than originally expected. This raises the potential for increased volatility around the event.

For now, the backdrop remains relatively supportive. Oil prices are falling, inflation may be peaking, and financial markets have already significantly repriced rate expectations. Those factors reduce the pressure on the Fed to take immediate action.

Instead, next week's meeting is likely to be remembered less for what the Fed does and more for what Warsh says.

A new chairman, a new communication strategy, and potentially a new policy framework are all on the table.

The rate decision itself may be the least important part of the meeting.

The real story will be the first glimpse into how Kevin Warsh intends to reshape the Federal Reserve and whether that transformation ultimately makes monetary policy more flexible—or simply more uncertain—for investors.