The Federal Reserve is not expected to change interest rates this week, but that doesn't mean the meeting lacks importance. In fact, Wednesday's Federal Open Market Committee decision may be one of the most closely watched Fed events of the year as investors get their first real look at Kevin Warsh's leadership style and his vision for the future of the central bank.

Markets overwhelmingly expect policymakers to leave the federal funds target range unchanged at 3.50%-3.75%. The focus instead will fall on the updated Summary of Economic Projections (SEP), the revised dot plot, and perhaps most importantly, Warsh's first press conference as Fed Chair.

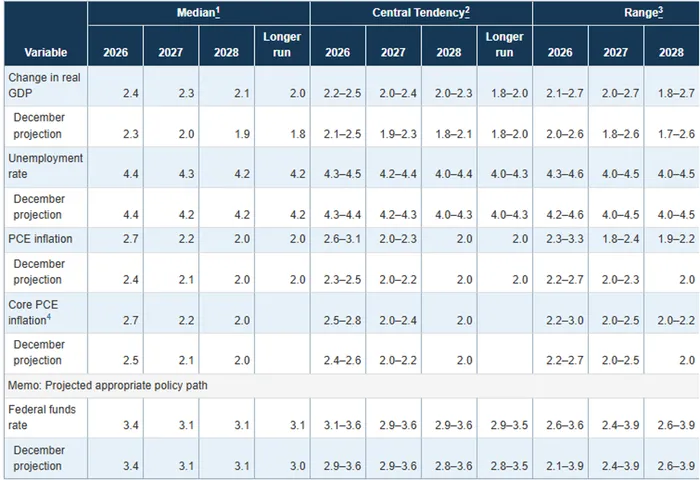

March SEP:

While there has been considerable discussion about inflation reaccelerating over the past several months, the backdrop has changed meaningfully heading into the meeting. The most notable shift has been the collapse in energy prices following the memorandum of understanding announced between the United States and Iran over the weekend. WTI crude has fallen to roughly $80 per barrel while Brent crude has slipped below $83, both marking their lowest levels since early March.

That decline creates an interesting challenge for policymakers.

The May CPI and PPI reports were generally viewed as hot. Headline CPI accelerated to 4.2% year-over-year while producer prices also surprised to the upside. However, much of the pressure came from energy-related categories, transportation costs, and supply-chain-sensitive areas. If oil prices remain near current levels, some of those inflation pressures could begin easing over the coming months.

As a result, the Fed finds itself in an unusual position.

Inflation remains elevated and above target, but one of its largest recent drivers is now moving sharply in the opposite direction.

That dynamic may help explain why markets still expect the Fed to remain on hold this week despite recent inflation surprises.

Current futures pricing suggests the first rate hike remains most likely in December, with investors only expecting one additional increase over the next year. That outlook could change quickly, however, depending on the message delivered Wednesday.

One of the biggest questions facing investors is whether Warsh begins implementing some of the communication changes he discussed before becoming chair.

Warsh has frequently criticized the Fed's reliance on forward guidance and has questioned whether the central bank should be providing detailed forecasts years into the future. That has fueled speculation that the SEP and dot plot may eventually be scaled back or even eliminated under his leadership.

While few expect that to happen immediately, this meeting could provide clues about the future direction of Fed communications.

Ironically, that possibility makes this week's dot plot even more important.

Some analysts believe this could be one of the final opportunities to see policymakers publicly express their individual rate expectations in the current format.

The latest projections suggest a committee that remains divided.

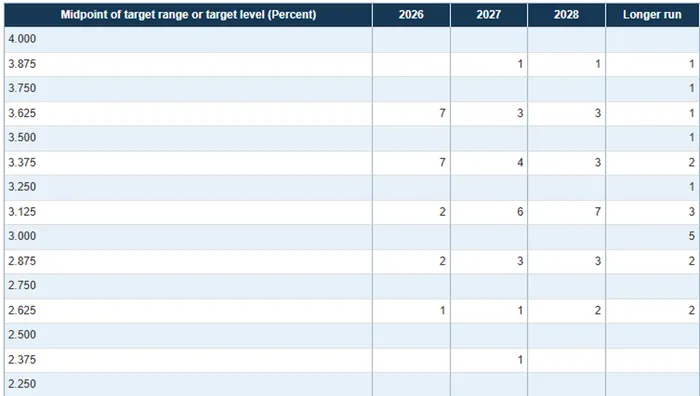

The current dot plot indicates most policymakers expect rates to remain between 3.125% and 3.625% through 2027, with the longer-run estimate centered near 3.0%. However, investors will be watching closely to see whether more officials shift toward higher rate projections following the recent inflation data.

March Dot Plot:

A hawkish shift does not necessarily require an outright rate hike forecast.

Even modest adjustments could carry significant implications for markets.

If several policymakers move their 2026 and 2027 projections higher, it would suggest growing concern that inflation is proving more persistent than expected. Likewise, if the median projection begins drifting upward, investors may interpret that as a signal that the Fed is becoming less comfortable with current inflation trends.

The policy statement itself may also provide important clues.

One area to watch closely is the Fed's characterization of inflation.

If policymakers continue describing inflation as "elevated" but note recent declines in energy prices and improving inflation expectations, markets may view that as a relatively balanced outcome. However, if the statement emphasizes that inflation remains "unacceptably high," "persistent," or that progress toward price stability has stalled, investors would likely interpret the language as more hawkish.

Another important section involves risk assessment.

During the Powell era, the Fed often attempted to balance concerns about inflation and economic growth. Investors should watch whether the committee begins placing greater emphasis on inflation risks relative to growth risks. Any suggestion that inflation has become the dominant concern would represent a meaningful shift in tone.

Balance sheet policy could be another source of headlines.

Warsh has long argued that the Federal Reserve's balance sheet became too large following years of quantitative easing. While major changes are not expected this week, investors will be listening carefully for any comments regarding future balance sheet reduction plans.

The press conference may ultimately prove more important than the statement itself.

Markets already know the Fed is unlikely to move rates Wednesday.

What remains uncertain is how Warsh intends to lead the institution.

Will he embrace a more rules-based framework? Will he reduce reliance on forecasts? Will he prioritize inflation control over labor market concerns? Investors are unlikely to receive definitive answers, but Wednesday may provide the first meaningful clues.

For traders, several developments would qualify as notably hawkish.

A higher median dot plot, upward revisions to inflation forecasts, language emphasizing inflation risks over growth risks, discussion of additional tightening if necessary, or commentary suggesting rates may need to remain restrictive for longer would all likely push yields higher and pressure risk assets.

Conversely, acknowledgment of falling energy prices, balanced risk language, stable long-term projections, and discussion of uncertainty surrounding inflation trends would likely be viewed as more neutral.

Ultimately, this meeting is less about what the Fed does and more about how the Fed communicates.

The era of Jerome Powell is over.

This week investors begin learning what the era of Kevin Warsh might look like.