Fortinet moved to the top of the after-hours board on May 6 after a beat-and-raise quarter challenged the market's worry that artificial intelligence would erode established cybersecurity franchises. FTNT traded roughly 15% to 18% higher in extended trading, with Investing reporting a 17.8% jump after the release and its after-hours board later showing FTNT up 14.81% at $103.27.

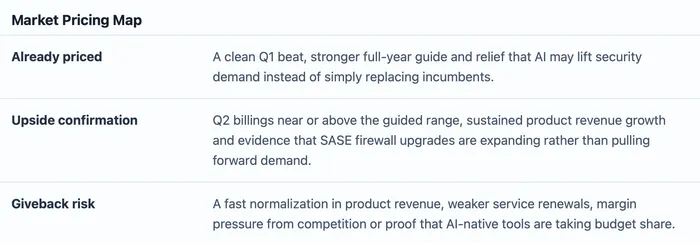

Investors are repricing Fortinet as an AI-era security demand beneficiary because billings, product revenue and guidance all beat expectations while management said the threat environment is being intensified by AI. The trade is still conditional: a cybersecurity stock can hold a higher multiple only if the next billings and renewal data show that the demand surge is durable rather than a one-quarter hardware catch-up.

A beat-and-raise quarter changed the question

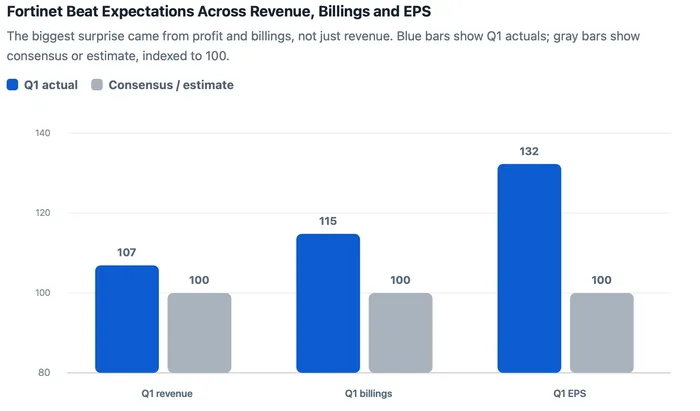

Fortinet's official release showed Q1 revenue rising 20% year over year to $1.85 billion, product revenue rising 41% to $645 million and billings rising 31% to $2.09 billion. Non-GAAP EPS grew 41% to $0.82, while operating cash flow and free cash flow reached record levels of $1.08 billion and $1.01 billion.

Consensus was set lower. The same earnings reaction report put Wall Street's Q1 EPS estimate at $0.62 and revenue estimate at $1.73 billion, while Investor's Business Daily said billings were expected at $1.821 billion. That gap matters because billings and product revenue are closer to the demand question than GAAP earnings alone.

A narrow cost-driven beat would have left the old debate intact. Broad strength across billings, product revenue, EPS and cash generation gives the market a cleaner reason to revalue Fortinet as a platform that can capture more enterprise security spending as networks become more complex.

The chart shows where expectations were too low

Fortinet beat expectations in several places, but the cleanest comparison is Q1 actuals against Q1 expectations. Revenue exceeded the estimate by roughly 7%, billings cleared the expected level by about 15%, and non-GAAP EPS was more than 30% above consensus. Q2 and full-year guidance still matter, but they belong in the execution discussion rather than the same chart.

Sources: Fortinet Q1 2026 release, Investing.com consensus comparison, and Investor's Business Daily billings estimate. This stitched comparison indexes each Q1 consensus or estimate value to 100 so revenue, billings and non-GAAP EPS can be compared without mixing dollar units on one axis.

AI is moving from disruption risk to threat demand

Cybersecurity has been one of the more complicated AI trades. AI-native products can pressure older software categories, yet generative AI also raises the complexity of phishing, malware, data leakage and automated attacks. Fortinet's management framed Q1 billings growth around that second channel, saying the threat environment is being intensified by AI.

Product details reinforced the market read. Fortinet highlighted FortiOS 8.0, new FortiGate G Series products and collaboration with AI companies including Anthropic and OpenAI. Those disclosures do not prove Fortinet owns the AI-security opportunity, but they move the near-term debate away from simple disruption risk and toward whether its integrated platform can win larger enterprise budgets.

Guidance keeps the rally tied to execution

Management guided Q2 revenue to $1.83 billion to $1.93 billion, billings to $2.09 billion to $2.19 billion and non-GAAP EPS to $0.72 to $0.76. The revenue midpoint was above the $1.82 billion consensus cited in the earnings reaction report, and the EPS range also sat above the $0.70 estimate.

Full-year guidance carries the same message. Fortinet now expects $7.71 billion to $7.87 billion of 2026 revenue, $8.8 billion to $9.1 billion of billings and non-GAAP EPS of $3.10 to $3.16. Investing.com put the new revenue midpoint above a prior $7.6 billion consensus and the EPS midpoint above a $2.98 estimate.

That guidance is strong enough to explain the stock reaction, but it also raises the hurdle. A bigger revenue base, high margins and a sharp stock move leave less room for a merely in-line quarter. Investors will likely focus less on whether AI is a theme and more on whether Q2 billings prove that buyers are expanding deployment.

What can keep or break the repricing

Fortinet has already earned credit for Q1 execution. Fresh upside now depends on a narrower set of validation points: billings inside or above the Q2 range, continued product strength without excessive discounting, service revenue that supports recurring demand and margin guidance that does not show competitive pressure from cloud-native or AI-native rivals.

Fortinet's own risk language still names technological changes, including advances in artificial intelligence, as a factor that could make products less competitive. For now, the quarter gives bulls better evidence than a simple cybersecurity relief rally. The next test is whether AI-driven threat demand keeps converting into billings quickly enough to justify the new price.