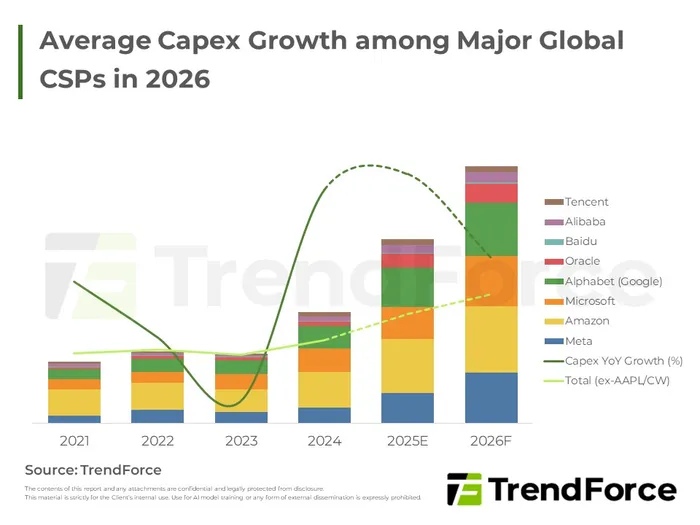

$800 billion in, 0.1 point out—the capex boom is real, but the macro payoff is a rounding error

Watch the trajectory of a single forecast and you learn more than any single data point can tell you. In January, Goldman Sachs projected that the hyperscalers would spend north of $527 billion on AI in 2026. By late May, the bank had lifted its U.S. business investment forecast to 7.8% from 6.5%, with AI outlays running at an annualized $650 billion in the first quarter and tracking toward more than $800 billion by year-end. In roughly four months, the headline number jumped by more than $270 billion. That is not a forecast being fine-tuned; it is a forecast chasing a moving target.

The instinct is to read each upgrade as confirmation: spending is even bigger than we thought, so the trade is even better than we thought. I'd argue the more useful signal is the chase itself. When the best-resourced research desk on the Street has to keep marking its own number higher every quarter, it tells you the institution is reacting to momentum, not anticipating it—and momentum is exactly the thing that reverses without warning.

But the line that should stop investors cold is buried in the same note. For all those hundreds of billions, Goldman estimates AI-related spending will add just 0.3 percentage points to "true" GDP growth in 2026—and only 0.1 point to measured GDP. The gap exists because a large share of the equipment is imported, and semiconductor investment is still partially undercounted in official statistics. Sit with that for a second: an $800 billion capital cycle, arguably the defining economic story of the decade, lands on the actual economy as a rounding error.

That disconnect is the whole point. The capex is real—it flows into servers, memory, power infrastructure, data centers, and R&D, and Goldman reckons it adds about 3.3 points to true capex growth. The spending is genuinely reshaping the investment cycle. What it is not doing, at least not yet, is showing up where it ultimately has to: in broad economic output, and by extension in the productivity gains that are supposed to justify the bill. Money going in is not the same as value coming out, and right now the market is pricing the first as if it were proof of the second.

The Boom Has Fuel—But That Was Never the Question

There are real tailwinds keeping the cycle alive, to be fair. New expensing provisions in the One Big Beautiful Bill Act are adding roughly three points to capex growth, and two drags from 2025—fading CHIPS-era construction and tariff uncertainty—are easing. Goldman doesn't even think higher oil prices will derail it. The boom has fuel. The bulls aren't wrong that the spending is happening.

The question is what the spending earns. Not every analyst frames it as a risk—22V Research, for instance, calls the buildout a physical-world bottleneck rather than a bubble, more 1970s capex regime than 1999 mania. That may prove right. But "bottleneck" and "boom" both describe the input side. Neither answers the output question, and the output question is the one that gets repriced fastest when sentiment turns.

So here's the takeaway I'd hold onto. Don't treat each upward revision to the AI spending number as bullish news in itself—a forecast racing to keep pace with reality is a sign of how fast the narrative is moving, not how sound it is. Watch the conversion instead: the moment when capex starts translating into measured output and durable margins, or the moment it conspicuously fails to. Until that line moves, the most honest description of the AI buildout is that we are spending like the future is certain while the economy registers almost nothing. The bill is enormous and concrete. The payoff is still, for now, a forecast.