Goldman Sachs (GS) kicked off earnings season in unusual fashion as the first major money center bank to report, delivering a solid top- and bottom-line beat that, on the surface, should have been enough to support shares. Instead, the stock is trading lower by roughly 2% following the release, a move that appears less about disappointment and more about positioning after a remarkable run. Shares of Goldman Sachs (GS) have surged approximately 83% over the past 12 months, leaving expectations elevated and little room for anything short of a clear upside surprise across all segments. In that context, this quarter looks more like a “good but not great” print, with pockets of strength offset by a few notable misses and a broadly in-line outlook.

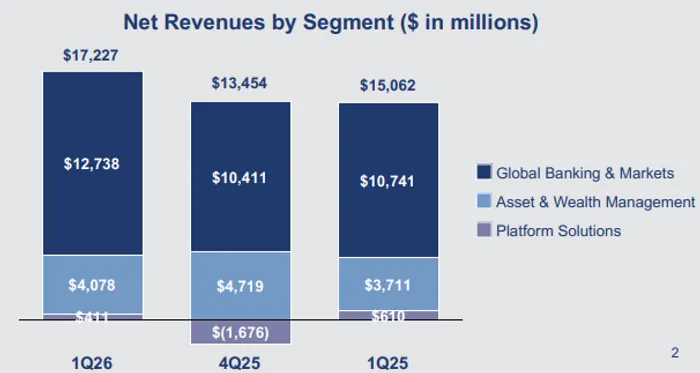

From a headline perspective, Goldman Sachs (GS) delivered first-quarter revenue of $17.23 billion, ahead of expectations of $16.97 billion, while earnings per share came in at $17.55 versus the $16.49 consensus estimate. Net income totaled $5.63 billion, translating to a robust return on equity of 19.8%, a level that underscores the firm’s ability to generate strong profitability even in a more volatile macro environment. The firm also reported investment banking fees of $2.84 billion and net interest income of $3.56 billion, both broadly supportive of the overall beat. Importantly, this marked one of the strongest quarters in recent periods, with management highlighting that it was among the second-highest levels of revenue and earnings in the firm’s history.

Diving into the segment-level performance, the standout was clearly equities trading, where Goldman Sachs (GS) generated $5.33 billion in revenue, well ahead of the $4.9 billion estimate. This strength was driven by record equities financing and strong intermediation activity, particularly in cash products, reflecting heightened client engagement amid elevated market volatility. This aligns with broader industry trends, where equity desks have benefited from increased trading volumes and hedge fund activity. In contrast, fixed income, currencies, and commodities (FICC) came in meaningfully below expectations, generating $4.01 billion in revenue versus the $4.87 billion estimate—a roughly $1 billion shortfall that stands out as the key blemish in the report. Weakness in rates, mortgages, and credit products drove the miss, partially offset by strength in commodities and currencies, which benefited from the recent surge in energy prices.

Investment banking delivered a strong year-over-year rebound, with fees rising 48% to $2.84 billion, supported by a significant increase in advisory activity and equity underwriting, particularly in convertible offerings. This is an encouraging sign for the broader dealmaking environment, suggesting that M&A pipelines are reopening after a subdued period. However, the firm did note that its investment banking backlog declined slightly on a sequential basis, hinting that while activity has improved, visibility remains somewhat uncertain. That nuance likely contributed to the muted stock reaction, as investors are looking for a more sustained recovery rather than a one-quarter rebound.

One of the more important—and underappreciated—lines in the release relates to debt underwriting, where Goldman Sachs (GS) reported higher revenues driven by investment-grade and asset-backed issuance, but “significantly lower” revenues from leveraged finance. This shift is notable because it reflects a broader change in credit market dynamics. Simply put, capital is flowing more readily to higher-quality borrowers, while demand for riskier, highly levered deals remains constrained. This is not just a Goldman-specific issue; it is a signal that credit markets are becoming more selective, with tighter conditions for lower-rated borrowers. For private equity, which relies heavily on leveraged financing for buyouts and recapitalizations, this environment presents a clear headwind. Fewer deals are getting done, and those that do are likely coming with higher costs and more restrictive terms.

At the same time, this shift toward investment-grade issuance is not entirely negative. It provides a more stable, albeit lower-margin, revenue stream for Goldman Sachs (GS), helping to smooth earnings in a more uncertain macro backdrop. However, it does cap upside potential, as leveraged finance tends to be more lucrative during periods of strong risk appetite. In that sense, the mix shift can be viewed as a defensive positioning within the firm’s capital markets business, reflecting both client behavior and broader market conditions.

Another area to watch is credit quality, with provisions for credit losses rising to $315 million, driven primarily by growth and impairments in wholesale loans. While not alarming, this does suggest some early signs of stress in certain parts of the loan book, particularly in a higher-rate environment. Operating expenses also increased 14% year-over-year to $10.43 billion, largely due to higher compensation and transaction-related costs, which is consistent with stronger business activity but also worth monitoring from a margin perspective.

Looking ahead, the conference call at 9:30 a.m. ET will be critical in shaping investor sentiment. Markets will be focused on management’s commentary around the investment banking pipeline, particularly whether the recent uptick in advisory and underwriting activity is sustainable. Given the current backdrop of heightened volatility—driven in part by geopolitical developments and rising energy prices—clients may remain cautious, which could impact deal flow in the near term. Additionally, any discussion around private credit will be closely scrutinized, as investors try to gauge how much activity is migrating away from traditional bank-led underwriting into alternative financing channels.

From a technical standpoint, Goldman Sachs (GS) is trading around $875, sitting directly on its 50-day moving average, a level that is likely to serve as a key near-term support zone. After such a significant run over the past year, this area becomes an important test of whether the stock can consolidate gains or is due for a deeper pullback. A sustained break below this level could invite further selling pressure, while a hold could reinforce the broader uptrend.

In sum, this was a strong quarter for Goldman Sachs (GS), but not one that fundamentally changes the narrative. The firm continues to execute well across its core businesses, particularly in equities and investment banking, but the miss in FICC and the softness in leveraged finance highlight areas of caution. The stock’s reaction appears more tied to positioning and expectations than to any material deterioration in fundamentals. As always, the real story will emerge not just from the numbers, but from the tone and guidance provided on the conference call, especially as investors look for clarity in an increasingly complex macro environment.