U.S. producer prices jumped 1.4% in April, the largest monthly increase since March 2022, and rose 6.0% from a year earlier. In a normal rate-sensitive tape, that would be a direct hit to long-duration growth stocks.

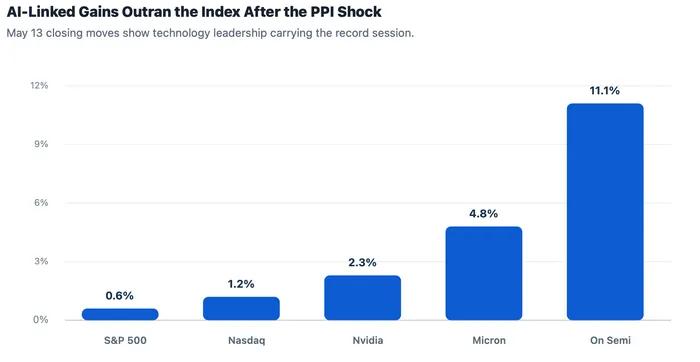

May 13 produced the opposite headline. The S&P 500 rose 0.6% to 7,444.25 and the Nasdaq Composite gained 1.2% to 26,402.34, both record closes, while the Dow slipped 0.1%. Investors were not ignoring inflation. They were paying more for the part of the market where AI-linked earnings and policy optionality still looked strong enough to absorb it.

Stocks are not fearless about inflation. For now, Wall Street is betting AI earnings can pay the inflation bill. Macro risk is being repriced into breadth, rates and margin tests, while AI leadership is still being rewarded at the index level.

A Hot PPI Print Became a Narrow Rally

April's inflation mix was not benign. The BLS report showed final-demand services up 1.2% and final-demand goods up 2.0%, with energy prices rising 7.8% and gasoline up 15.6% from March. Core producer prices excluding food, energy and trade services rose 0.6% on the month and 4.4% from a year earlier.

Those numbers challenge the earlier market assumption that inflation pressure was becoming manageable enough for easier policy to return. Energy, transportation and services inflation raise the risk that corporate cost pressure will show up later in margins, consumer prices or both.

Stock action still split sharply. AP described a record-setting session led by technology, even as the majority of U.S. stocks fell. That distinction matters more than the record itself. A broad inflation-friendly rally would say investors had dismissed the macro shock. A narrow tech-led rally says the market has chosen a smaller group of companies as its shock absorber.

Rate Cuts Were Not What Stocks Rewarded

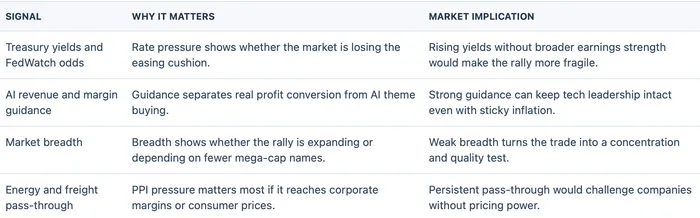

Bond pricing did react. Traders expected the Fed to stay on hold through the year, with a 34.3% chance of a rate hike by December, up from about 15% a week earlier, according to CME FedWatch data cited by Reuters in its May 13 report.

Timing matters here. The PPI figures are April data released by BLS on May 13; the FedWatch number is a live market-pricing snapshot as cited in the same day's Reuters market report, not a fixed probability. Treating both as timestamped evidence keeps the article from turning a volatile futures-implied reading into a settled Fed forecast.

Equity resilience matters for this reason. If the S&P 500 and Nasdaq were still trading mainly on imminent rate cuts, a PPI shock of this size should have been harder to shrug off. Instead, the tape behaved as if easier policy is no longer the only route to equity upside.

Higher rates still matter. They lift the discount rate on future earnings and pressure companies that depend on cheap funding. The shift is more specific: investors appear willing to pay for technology earnings visibility and AI revenue momentum even as the bond market removes some of the easing cushion.

AI Buying Was Selective Across the Supply Chain

Technology leadership had fresh support beyond a generic AI narrative. In the same market wrap, Micron Technology rose 4.8%, On Semiconductor gained 11.1% and Nvidia advanced 2.3%, with Nvidia the strongest positive force on the S&P 500 because of its market weight.

Investors were not buying every technology stock equally. Nvidia carried the compute-core logic: if AI training and inference demand stays strong, the largest accelerator supplier remains the most direct index-level expression. Micron gave investors the memory leg, where AI memory and storage products are tied to data-center buildouts. On Semiconductor gave the trade a power and edge-chip angle, with AI data-center power solutions closer to the infrastructure layer.

Cloud and capital-allocation evidence filled out the rest of the chain. SoftBank's profit for the 12 months through March rose nearly five-fold as AI investments paid off, while Alibaba said AI and cloud growth accelerated in the latest quarter and its U.S.-listed shares rose even though broader results missed expectations. Alibaba's Cloud Intelligence Group revenue rose 38% in the January-March quarter, giving investors a cleaner revenue example than a pure narrative bid.

Those examples do not prove every AI stock deserves a higher multiple. They explain why the market was willing to treat the inflation shock as a relative-value event instead of a full risk-off event. Investors rewarded the parts of the AI chain most able to point to revenue, scarcity or profit conversion, while weaker parts of the tape absorbed more of the macro damage.

Source: AP market wrap for May 13, 2026. PPI context from the BLS April 2026 Producer Price Index release. Values are daily closing stock and index moves, not monthly inflation rates.

Weak Breadth Turned the Rally Into a Quality Test

Record closes can hide a lot of stress. Declining issues outnumbered advancers by 2.39-to-1 on the NYSE and by 1.89-to-1 on the Nasdaq, according to Reuters. That is not the footprint of a market that has forgotten inflation risk.

Narrow breadth changes the trade from simple momentum to a quality screen. Companies with visible AI revenue, pricing power, balance-sheet flexibility or margin leverage can keep attracting capital. Companies with weak cost pass-through or stretched funding needs become more exposed as producer inflation pushes through the system.

This is why the regime label matters. "Bad macro, strong tech" is not the same as "bad macro does not matter." It means macro damage is being distributed unevenly, with the largest and most AI-exposed companies masking stress elsewhere in the index.

China Optionality Was Still Only an Option

Nvidia also had a policy catalyst. Jensen Huang joined President Donald Trump's trip to China, where discussions could include shipments of Nvidia AI chips to the world's second-largest economy. A China opening would not erase U.S. inflation pressure, but it gives investors a company-specific upside channel that is separate from Fed policy.

For macro pricing, a stock tied to AI demand, China access and dominant index weight can behave differently from a smaller cyclical company facing higher input costs. The same PPI print can pressure one balance sheet and raise the relative appeal of another.

Policy optionality should still be treated as conditional. Export rules, licensing terms and geopolitical risk can change quickly. Possible China access is option value, not booked revenue. The market signal is not that China risk has disappeared; it is that investors are willing to price a possible offset while earnings momentum remains visible.

Margin Pass-Through Is the Next Test

Producer inflation usually becomes more important when it moves from data release to income statement. If energy, freight and services costs keep rising, investors will need to watch whether companies can pass those costs through without damaging demand.

AI leaders have a cleaner story only if revenue growth keeps absorbing that pressure. Memory suppliers need pricing strength, chipmakers need order visibility, hyperscalers need cloud and AI workloads to justify capex, and software firms need proof that AI demand is becoming paid usage rather than just higher infrastructure bills.

A staged path is more useful than a single bullish or bearish label. Near term, AI and chip earnings decide whether the major indexes can keep absorbing higher-rate pressure. Over the medium term, if PPI keeps feeding into CPI and corporate costs, the market will shift from buying AI growth broadly to screening for pricing power and margin durability. Later, if AI earnings stop beating expectations while Treasury yields stay elevated, the larger risk may not be an immediate market-wide break, but sharper dispersion inside high-valuation technology.

May 13's record does not say inflation is harmless. It says the market has found a powerful counterweight in AI-linked earnings, semiconductors and mega-cap technology. That counterweight can keep working, but only while the proof keeps arriving. If inflation raises yields faster than AI lifts earnings expectations, the same narrow leadership that made new highs possible can turn into the market's main vulnerability.