KEY TAKEAWAYS

- Demand is real, but quality matters: HPE reported more than $6.3 billion of AI backlog, with 61% coming from government and large business customers, according to Reuters.

- Margin is the first test: Cloud and AI operating margin reached 12.4%, up from 6.6% a year earlier, while Server revenue inside the segment rose 32.7%.

- Networking is the second profit channel: Networking revenue rose 148.2% to $2.7 billion with a 21.6% operating profit margin, helped by the Juniper portfolio.

- Cash is the final test: HPE raised fiscal 2026 free-cash-flow guidance to at least $3.5 billion and introduced a fiscal 2027 framework calling for at least $4.5 billion.

- The risk is not weak AI interest: the risk is strong AI demand arriving with lower mix quality, pricing lag, inventory build or slower Juniper synergy capture.

HPE's 36% extended-trading surge after Monday's results was not just a relief rally around AI server demand. It was a rerating around whether HPE can make that demand show up in enterprise infrastructure economics. The company reported $10.7 billion of fiscal second-quarter revenue, up 40%, non-GAAP diluted EPS of $0.79, $1.4 billion of operating cash flow and $0.9 billion of free cash flow. That combination moved the debate from "can HPE sell AI servers?" to "can HPE turn AI servers into repeatable profit and cash?"

The distinction matters because an AI server dollar is not a software dollar. It often begins with expensive components, custom configurations, delivery timing and support commitments before it becomes margin or cash. HPE's quarter looked stronger because demand, segment margin, networking profit and cash generation all improved at the same time. The next few quarters have to prove that those links hold when more backlog converts into revenue.

Why The Stock Moved: Demand Was Finally Matched By Economics

AI server rallies can be fragile because revenue growth alone does not prove value creation. Servers carry component costs, supply-chain risk and customer-specific deployment work. In HPE's case, the quarter had a broader earnings bridge. The company reported record revenue, gross margin and non-GAAP diluted EPS, and its GAAP gross margin rose to 36.5%, up 810 basis points from the prior-year period, while non-GAAP gross margin rose to 36.9%, up 750 basis points. That is why the market reaction was larger than a simple revenue beat.

Reuters framed the demand backdrop clearly: HPE is benefiting as customers buy servers and networking products to power AI applications, while CFO Marie Myers said the company was managing a dynamic pricing environment with tools including long-term agreements that extend into 2027 and price adjustments that began late last year. That pricing point is central. If component costs move faster than HPE can price through, AI revenue can expand while profit quality deteriorates.

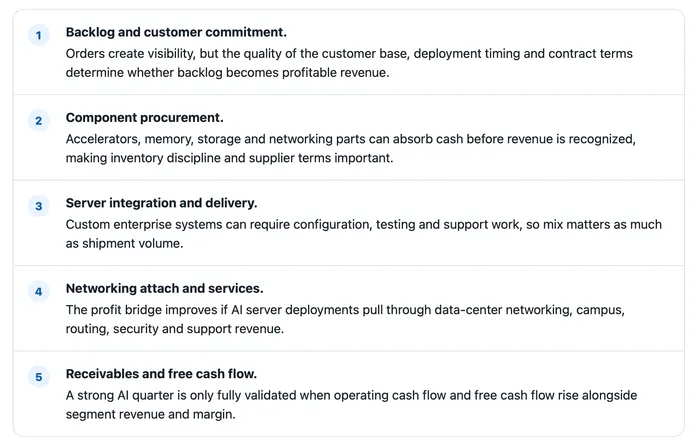

Where The AI Server Dollar Actually Flows

The central question for investors is not whether AI infrastructure spending exists. It is how much of that spending HPE can keep after component procurement, configuration, deployment, support and working-capital timing. The economic path looks more like a chain than a single sale:

The company's AI story is not just "more servers." It is a test of whether servers can pull through a higher-value enterprise stack.

Cloud And AI Margin Is The First Stress Test

HPE's most important evidence came from Cloud and AI, the segment that now absorbs Server, Storage and Financial Services. Cloud and AI revenue was $7.7 billion, up 22.9%, with a 12.4% operating profit margin. Server revenue inside that segment was $5.5 billion, up 32.7%.

The 12.4% margin is the new bar. A one-quarter improvement can come from better mix, utilization, price realization, cost discipline or timing. A durable thesis requires that margin to remain resilient as backlog converts. If future AI orders come with heavier customization, lower-priced hardware, memory-cost pressure or larger service obligations, HPE could still report strong Server revenue while the operating-margin story weakens.

- The core margin question: Was the Cloud and AI improvement mainly operating leverage, repeatable enterprise mix and pricing discipline, or was it partly a favorable quarter-specific mix effect?

- The evidence to watch: Cloud and AI margin staying near the new level while Server revenue grows would support a rerating. Server revenue growing while Cloud and AI margin rolls over would turn the story back into a lower-quality hardware cycle.

Pricing Power Is Now Part Of The AI Thesis

Reuters reported that HPE was navigating higher memory chip prices and that the company had been agile in passing cost increases to customers. That detail is more important than it looks. AI infrastructure is capital-intensive, and the gross margin of a server supplier can be squeezed if component inflation arrives before customer pricing resets.

HPE's answer is a combination of long-term agreements, pricing adjustments and customer mix. The government and large-enterprise backlog matters because these buyers may offer better visibility than more speculative demand, but they can also bring procurement complexity and timing risk. The best outcome is not simply more orders. It is orders with price protection, repeatable configurations and attached networking or service revenue.

Juniper Turns AI Demand Into A Networking Story

Networking made the quarter much more than a server headline. HPE reported $2.7 billion of Networking revenue, up 148.2%, with a 21.6% operating profit margin. The internal mix also mattered: Campus and Branch revenue was $1.3 billion, Data Center Networking was $320 million, Security was $273 million and Routing was $775 million. Management also said HPE was running ahead of schedule on Juniper Networks and Catalyst cost synergies.

This is the part of the story that can separate HPE from a pure server-cycle trade. AI workloads need compute, but enterprise deployments also need switching, routing, security, connectivity and management. If Juniper gives HPE more ways to attach higher-margin networking revenue to AI infrastructure projects, the market can value the business as an enterprise stack provider. If Networking growth fades or integration costs rise, the AI thesis becomes more dependent on lower-margin hardware volume.

Backlog Quality Matters More Than Backlog Size

HPE's backlog signal was strong, but the mix is what gave it analytical weight. Reuters reported more than $6.3 billion of total AI backlog, with 61% secured from government and large business clients. Myers also told Reuters that the strength of the quarter was largely driven by HPE's traditional server business focused on enterprise customers and that enterprises had significantly adopted agentic AI as a core workload.

That supports an enterprise-led interpretation rather than a single hyperscaler story. It also creates a sharper conversion test. Government and large enterprise orders can be durable, but they can be tied to budget cycles, security reviews, deployment windows and customization. The next phase is therefore not only backlog growth. It is the pace, margin and cash profile of backlog conversion. Reuters said HPE expects to ship and convert significantly more AI revenue in the back half of the year, with conversion expected to peak in the fourth quarter.

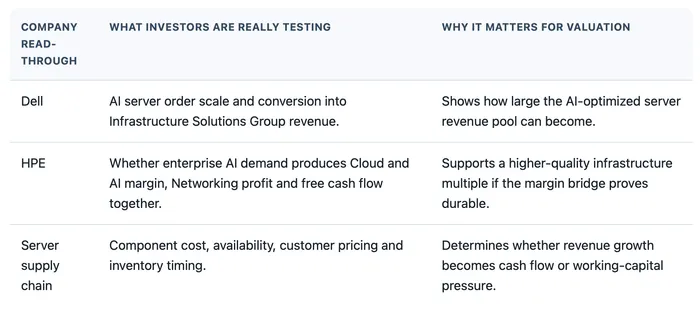

Dell Is The Scale Benchmark; HPE Is The Margin-Bridge Trade

Dell's latest results show the scale of the AI server benchmark. Dell reported $24.4 billion of AI orders and $16.1 billion of AI-optimized server revenue in its fiscal first quarter, and raised its full-year AI-optimized server revenue expectation to roughly $60 billion. Dell's Infrastructure Solutions Group generated $29.0 billion of revenue and $3.1 billion of operating income, or 10.5% of ISG revenue.

That comparison is useful because it prevents investors from applying one generic AI-server multiple to every supplier. Dell is the scale benchmark. HPE's argument is different: a smaller but potentially higher-quality enterprise infrastructure bridge, built around Cloud and AI margin, networking attach and free cash flow. The stock's 36% surge implies that investors are willing to pay for that bridge, but only if the next quarters show the bridge is repeatable.

The Broader AI Infrastructure Market Is Becoming A Financing Market

A separate private-credit story shows why investors are becoming more focused on cash-flow structure than headline AI demand. Bloomberg reported that Apollo Global Management and Blackstone were working to syndicate a roughly $36 billion debt financing to buy Google's TPUs for Anthropic. In that transaction, a special-purpose vehicle would buy chips, Anthropic would lease them, and senior debt investors would rely on lease payments and residual value support tied to Broadcom's credit profile.

HPE is not a direct party to that deal, but the logic is relevant. AI infrastructure is so capital-heavy that the market is asking the same questions across the stack: who funds the equipment, who owns the residual value risk, who receives the recurring economics, and who converts deployment into cash? For HPE, those questions translate into supplier terms, pricing discipline, networking attach and working-capital control.

The Guidance Raises The Bar

HPE's guide turned the quarter from a backward-looking beat into a forward-looking test. The company guided fiscal third-quarter revenue to $11.5 billion to $12.1 billion and non-GAAP EPS to $0.88 to $0.93. It raised fiscal 2026 revenue growth guidance to 29% to 33%, lifted non-GAAP EPS guidance to $3.35 to $3.45, and said free cash flow should be at least $3.5 billion.

The 2027 framework is even more important for the durability question. HPE now expects 8% to 12% revenue growth, 12% to 16% non-GAAP diluted EPS growth, 12% to 16% non-GAAP operating margin and at least $4.5 billion of free cash flow. Those targets imply that AI demand, Juniper synergies and cost discipline have to show up beyond one strong quarter.

What Could Break The Thesis

The downside case is not that AI demand disappears. The more realistic risk is that demand remains strong while economics thin out. After a 36% post-earnings move, the market will have less patience for revenue that does not carry through to operating margin and cash flow.

- Cloud and AI margin reversal: If Server revenue grows but Cloud and AI margin falls meaningfully from 12.4%, the market may treat the quarter as mix-driven rather than durable.

- Backlog conversion without cash: A large AI backlog can still disappoint if inventory and receivables absorb the benefit before free cash flow appears.

- Pricing lag: Higher memory or accelerator costs could pressure gross margin if HPE cannot pass through increases quickly enough.

- Juniper integration risk: The networking thesis depends on synergy capture and profitable attach, not just larger reported Networking revenue after the acquisition.

- Customer concentration and deployment timing: Government and large-enterprise demand can be attractive, but procurement cycles and installation windows can make revenue recognition lumpy.

- Valuation reset: The post-earnings surge prices in more than a beat; it prices in confidence that the 2026 and 2027 frameworks are achievable.

HPE's quarter changed the AI-server debate because it paired demand with margin, networking profit and cash generation. The stock reaction will be easier to defend if four indicators continue to move together: Cloud and AI margin near the new level, AI backlog converting into profitable Server revenue, Juniper synergies showing up in Networking profit, and free cash flow tracking the raised guide. Without those links, AI demand remains real, but the earnings bridge behind the 36% move becomes thinner.