The copper supply story continues to dominate investor thinking, and Hudbay Minerals is positioning itself as a pure-play copper developer with a disciplined roadmap. At the Canaccord Global Metals and Mining Conference, the company reinforced a growth narrative built around three pillars: a clear strategic framework, proven project execution, and financial strength.

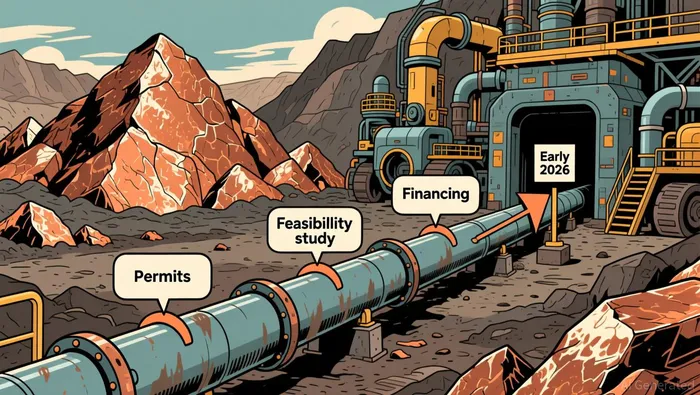

The core of Hudbay's thesis rests on what management calls a "Clear, Disciplined Growth Strategy." This isn't just marketing language-it's a filter for every growth opportunity the company pursues. According to the presentation, any asset must meet specific criteria: low-cost, long-life, meaningful scale potential, situated in mining-friendly jurisdictions, and capable of delivering per-share appreciation. Copper World project, Hudbay added another layer of rigor through its 3-P plan. This framework requires three prerequisites before any project advances: securing all necessary permits, completing a robust feasibility study, and developing a prudent financing strategy.

The 3-P plan is where strategy meets execution. By 2024, Copper World had already secured all required permits-the first "P" checked off. In 2025, entered a $600 million joint-venture partnership with Mitsubishi Corporation, addressing the financing prerequisite. The project is now advancing through definitive feasibility studies, with management expecting to make a final sanctioning decision early in 2026. That timeline is the critical metric for investors watching this pipeline.

Beyond Copper World, the presentation outlined growth options at existing operations. In Peru, Hudbay is evaluating a pebble crusher to increase mill throughput at Constancia, plus drilling at prospective Maria Reyna and Caballito properties. In Manitoba, the company continues exploration at Snow Lake targeting discoveries to utilize excess capacity at the Stall mill, while advancing economic studies for reprocessing tailings at Flin Flon. These are incremental plays, but they demonstrate the company is thinking about growth across its entire portfolio, not betting everything on a single project.

What stands out is the discipline. The company isn't rushing to sanction Copper World-it's following the 3-P plan methodically. The Mitsubishi JV provides financial credibility and reduces execution risk. For investors focused on copper supply, the question becomes whether this disciplined approach will translate into timely production growth, or whether the timeline remains vulnerable to execution delays. The early 2026 sanctioning decision will provide the next clear signal.

Copper Supply Dynamics: Why Hudbay's Pipeline Matters

The broader copper supply story is one of tightening margins and rising demand, making any credible new production pipeline increasingly valuable. Hudbay's operational scale positions it meaningfully within this context. The company employs 3,080 employees and generates substantial revenue-CAD $3.02 billion annually-with a net income of CAD $794 million. These aren't just size metrics; they reflect a mature operating footprint capable of delivering consistent cash flow while new projects like Copper World move toward sanction.

What matters for the supply narrative is what that scale represents in market terms. Hudbay's market capitalization sits around $11.53 billion, placing it firmly in large-cap territory. That valuation signals investor confidence in the company's copper-focused growth trajectory-it's the market pricing in the expectation that new production will materialize on schedule and at cost. For a commodity as critically undersupplied as copper, that confidence isn't trivial; it's the financial fuel that turns project plans into actual metal.

The analyst community's alignment reinforces this reading. Of 13 analysts covering the stock, 12 have issued buy ratings, with just one hold. The average price target stands at C$39.10, implying roughly 14% upside from current levels. That consensus isn't driven by short-term price moves-it's anchored in the fundamental supply story. Analysts are betting that Hudbay's disciplined approach to adding copper production, particularly through Copper World, will translate into meaningful earnings growth as the supply gap persists.

The implication for investors is straightforward: in a market where copper supply is expected to lag demand for years, Hudbay's combination of operational scale, funded growth pipeline, and analyst support creates a credible play on the structural deficit. The early 2026 sanctioning decision remains the key inflection point-but the numbers suggest the market is already leaning toward the project moving forward.

Valuation and Price Action: What's Priced In

The stock opened at $20.71 following a 5.75% pullback, placing it roughly in the middle of its 52-week range. That positioning is telling-it suggests the market isn't pricing in either a best-case or worst-case scenario for Copper World, but rather a probability-weighted expectation that the project moves forward on something close to schedule.

The valuation metrics support that reading. At a P/E of 14.35 with EPS of $1.67, Hudbay is trading at a modest multiple for a copper developer with a sanctioned pipeline ahead. That multiple isn't cheap-it reflects confidence that Copper World will reach sanction in early 2026 and begin adding production within the next few years. But it's not exorbitant either, which means the market is leaving room for execution risk. If the project were delayed or cancelled, the multiple would likely compress. If it proceeds on schedule, there's upside.

The analyst price targets make that upside explicit. The average target sits at C$39.10, implying roughly 14% upside from current levels, while Bank of America's target of C$44.50 suggests nearly 28% upside. Those targets aren't based on current earnings alone-they embed assumptions about Copper World reaching sanction and beginning to contribute production. The fact that 12 of 13 analysts rate the stock a buy reinforces that the consensus view is constructive on execution.

For investors, the key question is whether the current price adequately compensates for the timeline risk. The early 2026 sanctioning decision is the next material catalyst. If Copper World gets the green light, the stock has room to run toward those analyst targets. If there's a delay, the valuation could compress as the market reprices the timeline. For now, the numbers suggest the market is fairly priced-neither overly optimistic nor discounting the project entirely. It's betting on execution, and at these levels, the risk-reward appears balanced for investors who believe the 3-P plan will deliver.

Catalysts and Risks: What to Watch Next

The disciplined 3-P plan that has guided Hudbay's approach to Copper World now sets up a clear calendar of catalysts and risks for investors. The pivotal event remains the definitive feasibility study results and final sanctioning decision expected early in 2026. That decision will either validate the multi-year buildout or force a recalibration of the growth timeline.

The financing prerequisite has been addressed through the $600 million joint-venture partnership with Mitsubishi Corporation, which significantly de-risks the project from a capital perspective. This isn't to say financing won't matter-any escalation in project costs or shift in commodity prices could re-open that conversation-but the Mitsubishi partnership provides a substantial buffer. What remains is execution on the feasibility study and maintaining the permit approvals already secured in 2024.

On the near-term calendar, earnings date (est.) Jul 31, 2026 will provide a mid-year check-in on operational performance and cost discipline at the existing operations that fund the growth pipeline. The ex-dividend date Jun 9, 2026 is a minor catalyst for income-focused investors, though the modest forward dividend & yield of 0.03 (0.12%) signals this is primarily a growth play, not an income story.

The key risk remains copper price volatility. Hudbay's valuation assumes new production will come online on schedule and at cost, but a sustained drop in copper prices could pressure margins at existing operations and complicate the economic case for Copper World. The stock's beta of 2.15 reflects that sensitivity-it's a leveraged play on copper prices, for better or worse. Conversely, a sustained price rally would improve the economics of the project and potentially accelerate the path to sanction.

For investors tracking the supply story, the early 2026 decision is the critical inflection point. If Copper World proceeds, Hudbay's contribution to global copper supply will begin materializing within the next few years-a meaningful addition in a market where supply is expected to lag demand. If delayed, the market will need to reassess whether the company's disciplined approach is too cautious, or whether the timeline was always optimistic. The risk-reward at current levels hinges on that binary outcome, and the market appears to be pricing in a probability-weighted expectation that the project moves forward.