Executive Summary

Marvell has moved from "AI optionality" into an index-scale, valuation-sensitive custom silicon and interconnect story. The near-term catalyst is clear: S&P Dow Jones Indices said Marvell will enter the S&P 500 before the June 22, 2026 open, and Reuters reported the move would force benchmark-tracking vehicles to hold the stock. The deeper investment question is whether index demand is arriving after fundamentals have already justified a step-change valuation, or before the FY2028 proof is visible enough.

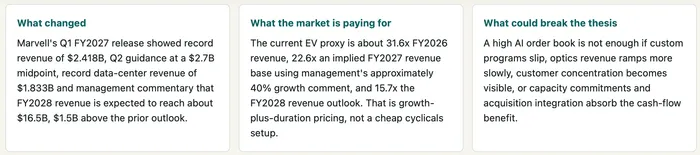

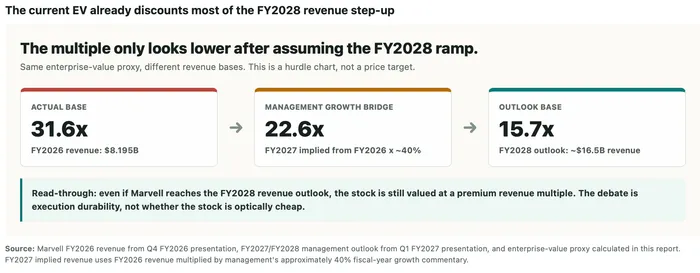

- Conclusion: the stock is no longer pricing a simple earnings beat. At roughly 15.7x management's FY2028 revenue outlook of about $16.5B, the current enterprise-value proxy already assumes that Marvell can convert AI bookings, custom XPU ramps, optics, switching and NVLink Fusion relevance into multi-year revenue acceleration. That can still work, but the falsification bar is now concrete: Q2 FY2027 revenue must land near or above the $2.7B guide midpoint, data-center growth must accelerate through fiscal 2027, and FY2028 visibility must improve rather than merely repeat the new $16.5B outlook.

Business And Catalyst Setup

Marvell describes itself in its latest Form 10-Q as a fabless supplier of data infrastructure semiconductor solutions spanning the data-center core to the network edge, with strengths in complex system-on-chip architecture, analog, mixed-signal and digital signal processing. That matters because the stock's AI identity is not simply "chip exposure." The economic role is narrower and more valuation-relevant: custom XPUs, electro-optics, switching, storage and interconnect products that help hyperscale data centers move compute and data across racks, accelerators and networks.

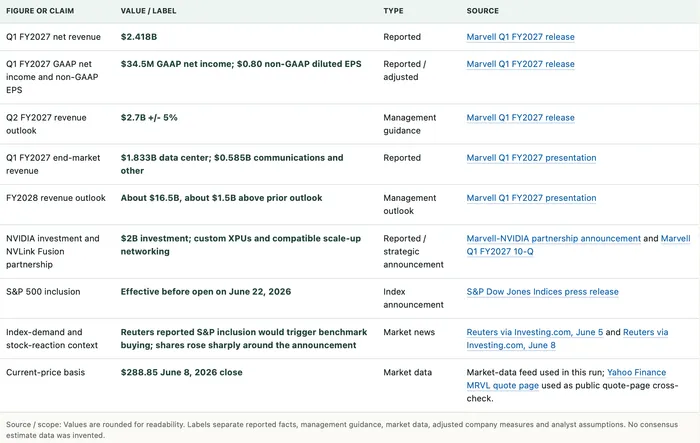

The recent catalyst stack is unusually dense. On March 31, 2026, Marvell and NVIDIA announced a partnership connecting Marvell custom XPUs and scale-up networking to NVIDIA's NVLink Fusion ecosystem, and NVIDIA invested $2B in Marvell. On May 27, Marvell reported Q1 FY2027 results and raised its multi-year outlook. On June 5, S&P Dow Jones Indices announced Marvell's S&P 500 inclusion effective before June 22 trading. Reuters then reported that the inclusion came after Marvell cleared a profitability hurdle and that the stock had rallied sharply on AI demand and index expectations.

Financial Analysis

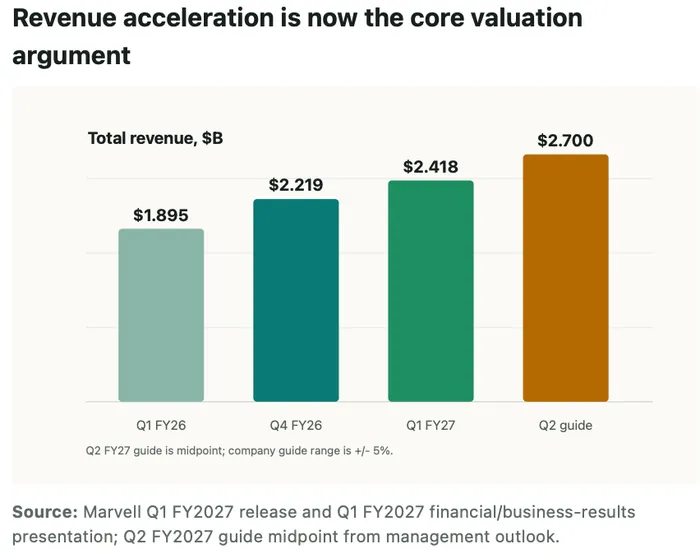

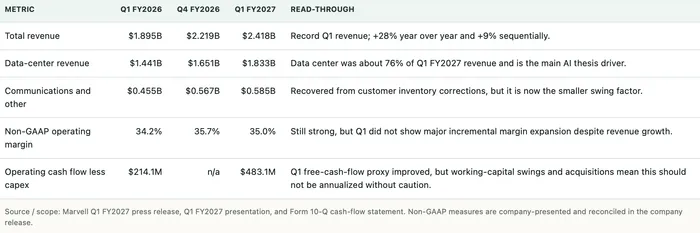

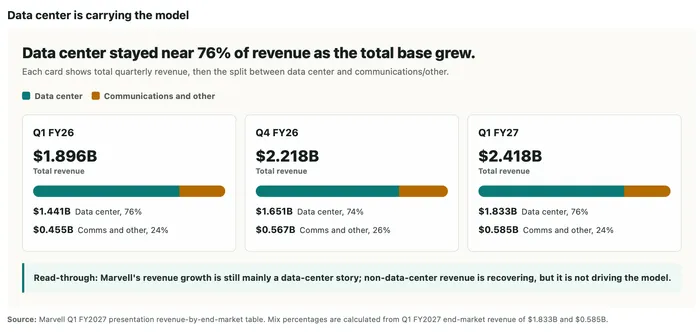

Q1 FY2027 was a clean acceleration quarter on revenue, but less clean on GAAP earnings because acquisition-related items, contingent consideration fair-value changes and preferred-stock mechanics complicate the earnings bridge. For valuation, the more useful operating facts are revenue growth, data-center mix, non-GAAP operating margin, free-cash-flow conversion and the multi-year revenue guide.

The non-GAAP margin profile supports the bull case but also defines the next proof point. Q1 non-GAAP operating income of $846.9M represented 35.0% of revenue, compared with 34.2% one year earlier and 35.7% in Q4 FY2026. That means the market cannot rely only on margin expansion to justify the new valuation; the primary support must come from sustained revenue growth and a path to stronger absolute cash generation.

Investment Thesis

1. The AI role is specific enough to analyze, not just a label.

Management says the improved outlook is driven by 800G and 1.6T scale-out optics, 51.2T Ethernet switches, scale-up optical solutions for NPO and CPO, scale-across data-center interconnect modules, and custom XPU and XPU-attach solutions. The NVIDIA partnership strengthens the ecosystem argument because Marvell can contribute custom XPUs and scale-up networking while NVIDIA provides the rack-scale architecture around Vera CPU, ConnectX NICs, BlueField DPUs, NVLink interconnect and Spectrum-X switches. That places Marvell in the high-speed plumbing and custom compute layer of AI infrastructure, a role that can compound if hyperscalers diversify beyond standard GPU-only clusters.

2. Index inclusion adds demand, but it does not lower the operating hurdle.

S&P 500 entry can create mechanical demand from passive managers. Reuters explicitly framed this as benchmark-tracking vehicles needing to hold constituents in line with benchmark weights. But the same flow also risks pulling valuation forward. Marvell is entering the index after a sharp AI rally, after clearing GAAP profitability criteria, and after management raised long-term revenue expectations. That makes the inclusion a catalyst for ownership, not proof that the FY2028 model is already de-risked.

3. The valuation is now a revenue-duration test.

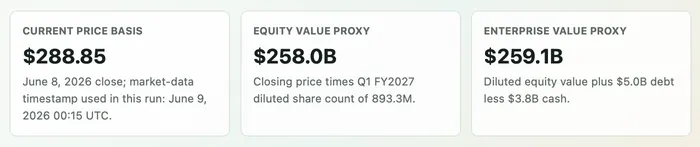

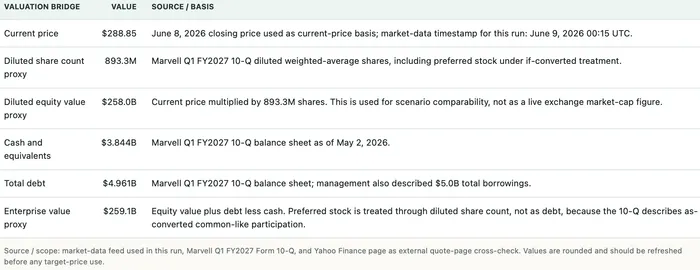

Marvell's FY2026 revenue was $8.195B, with data-center revenue of $6.100B. Management said FY2027 revenue growth is expected to be about 40%, data-center revenue about 50%, and FY2028 revenue about $16.5B. Using the current diluted enterprise-value proxy, the market is paying roughly 15.7x that FY2028 revenue outlook. For that to be fair rather than stretched, Marvell likely needs to show that FY2028 is not a peak-ramp year but part of a durable multi-year AI infrastructure cycle.

Disconfirming evidence to watch

- Q2 FY2027 revenue misses the $2.7B midpoint or guidance implies less acceleration in the second half of fiscal 2027.

- Data-center revenue growth does not move toward management's fiscal-year commentary, especially if communications and other revenue softens.

- Custom XPU programs ramp with lower gross margin than expected, pressuring the non-GAAP margin framework.

- Capacity deposits, acquisitions or preferred-stock conversion complexity absorb cash-flow improvement or dilute per-share economics.

Valuation

The sensitivity table explains why this is a high-quality but high-hurdle setup. At $16.5B FY2028 revenue, a 15.0x EV/revenue multiple implies $248B of enterprise value, below the current EV proxy. To create meaningful upside, Marvell either needs revenue above the new outlook or a market willing to continue paying 18.0x revenue for the FY2028 base case. That is possible in a constrained AI interconnect cycle, but it is not a conservative assumption.

Catalysts, Risks And Monitoring Framework

Source And Fact Ledger

What To Watch Next

The next reportable proof point is not whether Marvell remains an AI beneficiary; the current share price already answers that. The proof point is whether the Q2 guide, second-half acceleration and FY2028 revenue bridge can withstand public-market ownership after index inclusion. If Q2 revenue is near the guide midpoint and management raises or tightens FY2028 visibility around custom programs, optics and switching, the market can keep underwriting a premium multiple. If the next update merely repeats "strong AI bookings" without stronger segment proof, the stock may have to digest index demand at a lower revenue multiple.

Appendix: Model Notes

- Valuation method: scenario EV/revenue framework plus cash-flow sanity check. DCF and formal target-price work were not used because independently verified long-term consensus estimates, segment-level margin forecasts, capex and working-capital assumptions were not available for this run.

- FY2027 revenue bridge: FY2026 revenue of $8.195B multiplied by management's approximately 40% FY2027 growth commentary, producing an implied $11.47B revenue base for multiple context only.

- Cash-flow proxy: Q1 FY2027 operating cash flow of $638.8M less $155.7M of property-and-equipment purchases equals $483.1M. This is not treated as a forecast because working capital, acquisitions and capacity deposits can change materially.

- Preferred stock: NVIDIA's Series A Convertible Preferred Stock is modeled through diluted share count rather than as debt because the 10-Q describes as-converted participation and no redemption rights; this treatment should be revisited for formal target-price work.