After several weeks of rising anxiety surrounding inflation, interest rates, and Federal Reserve policy, investors finally received a report that was better than feared.

The May Consumer Price Index showed inflation continuing to run above the Federal Reserve's long-term target, but the details beneath the surface offered enough evidence of moderation to spark a relief rally across financial markets. Stocks moved higher immediately following the release while Treasury yields eased and expectations for additional Federal Reserve tightening were pushed out slightly.

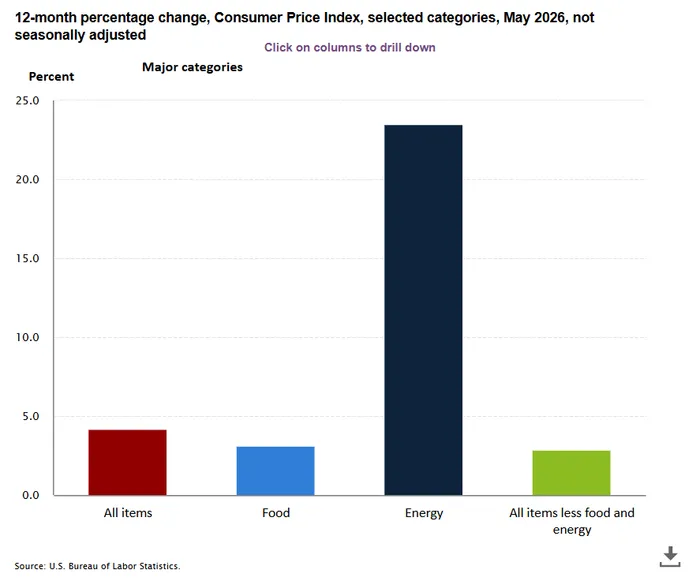

The headline numbers matched consensus forecasts. Consumer prices rose 0.5% in May and were up 4.2% from a year ago, marking the highest annual inflation rate since May 2023. Core CPI, which excludes food and energy, increased 0.2% during the month and 2.9% year-over-year. While the annual core figure ticked higher from April's 2.8% reading, the monthly increase came in below expectations and represented a meaningful slowdown from April's 0.4% pace.

That distinction is important.

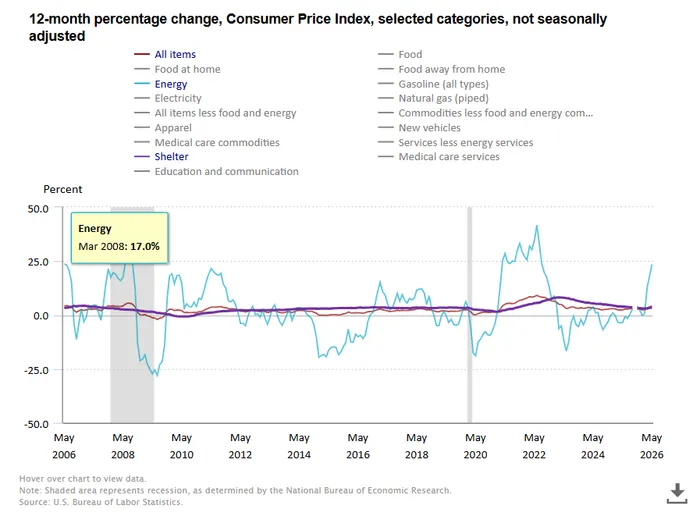

Markets had become increasingly concerned that the inflation pressures created by the ongoing conflict involving Iran and the resulting surge in oil prices would begin spreading broadly throughout the economy. Instead, the report suggested much of the inflation acceleration remains concentrated in energy-related categories rather than representing a broad-based reacceleration in pricing pressures.

Energy was once again the primary culprit.

The energy index rose 3.9% in May and accounted for more than 60% of the monthly increase in the overall CPI. Gasoline prices jumped 7.0% during the month and are now up more than 40% over the past year. The broader energy index has climbed 23.5% over the last twelve months as higher oil prices continue to work their way through the economy.

While those numbers are concerning, they were also largely anticipated.

Perhaps more encouraging was what happened outside of energy.

Core goods prices actually declined 0.1% during May, marking the first outright monthly decline since May 2025. Supercore inflation, one of the Federal Reserve's preferred measures that excludes housing and energy, also showed signs of moderation. These figures suggest that while higher oil prices are creating inflation pressures, they have not yet triggered a broad inflation spiral throughout the economy.

Housing inflation, another critical component of the report, also provided some encouraging signs.

The shelter index increased 0.3% during May, slowing from April's 0.6% increase. Owners' Equivalent Rent, which represents the largest component of CPI, rose 0.3% compared to 0.5% in April. Rent inflation also moderated slightly. Since housing costs account for more than one-third of the CPI basket, continued easing in shelter inflation remains one of the most important developments for policymakers.

Food inflation similarly moved in the right direction.

Food prices increased 0.2% during May compared with a 0.5% increase in April. Grocery prices rose just 0.1%, helping ease fears that higher energy costs were beginning to feed aggressively into food supply chains. Food inflation remains elevated on an annual basis, but the monthly trend suggests the oil shock has not yet become deeply embedded in consumer prices.

That does not mean inflation concerns have disappeared.

Several categories continue to show persistent upward pressure. Airline fares rose another 2.7% during May and are now up nearly 27% from a year ago. Personal care products, apparel, recreation, and certain tariff-sensitive categories also posted increases. Medical care costs moved higher as well, highlighting that some areas of the economy continue to experience price pressures.

The broader message from the report is that inflation remains elevated, but the situation is not deteriorating as rapidly as many investors feared.

That distinction is particularly important given the global central bank backdrop.

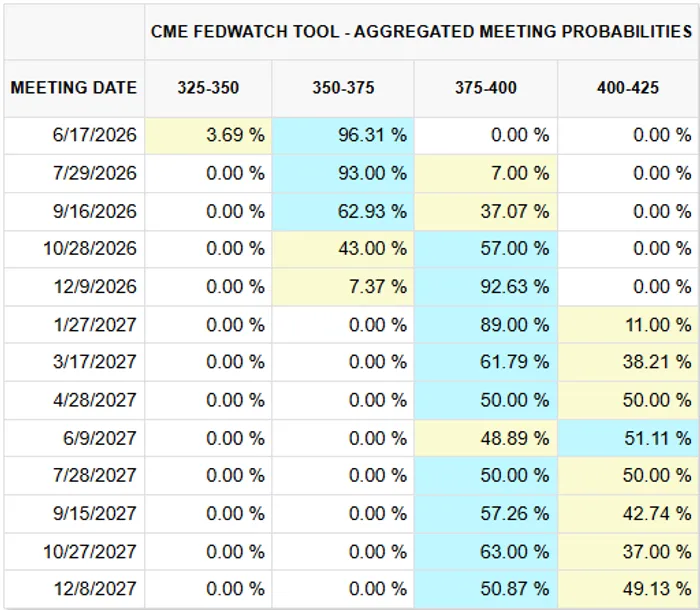

The European Central Bank is expected to raise interest rates by 25 basis points tomorrow, while the Bank of Japan is widely expected to deliver another rate increase next Monday. Both decisions will occur ahead of the Federal Reserve's June 17 policy meeting and underscore that policymakers around the world remain focused on inflation risks.

For Federal Reserve Chair Kevin Warsh, however, today's report likely reduces any pressure to consider a more aggressive stance next week.

Markets never expected the Fed to raise rates at the June meeting, and this report further reinforces that outlook. Instead, policymakers are likely to maintain their wait-and-see approach while monitoring whether energy-driven inflation begins spilling into broader areas of the economy.

Investors quickly adjusted their expectations following the report.

According to CME Fed Fund futures , expectations for the next Federal Reserve rate hike have now shifted back toward the December meeting. Just as importantly, markets do not currently assign a greater than 50% probability to a second rate increase until the middle of 2027. That represents a meaningful moderation from some of the more hawkish expectations that emerged following last week's stronger-than-expected employment report.

The market reaction reflects that change in thinking.

Stocks are rallying not because inflation is low, but because inflation did not come in worse than expected. After weeks of rising Treasury yields, concerns about another Fed hike, escalating geopolitical tensions, and heavy selling in technology stocks, investors were positioned defensively heading into the report. The CPI release removed one of the market's biggest near-term fears and triggered a relief rally across risk assets.

Still, declaring victory over inflation would be premature.

Energy prices remain elevated. The geopolitical situation involving Iran remains fluid. The ECB and Bank of Japan are both tightening policy. And inflation remains more than double the Federal Reserve's long-term target.

The May report was undoubtedly a positive development for markets. It was better than feared, supportive of a Fed pause, and suggests the oil shock remains relatively contained.

But while today's data may buy policymakers some time, it does not end the inflation debate.

Instead, it simply shifts the conversation from whether inflation is spiraling higher to whether policymakers can successfully navigate the next phase of the battle without needing to become more aggressive.