JPMorgan Chase (JPM) delivered a strong set of first-quarter results , beating expectations across nearly every major metric, but the market reaction has been more muted—if not outright negative. Shares are under pressure in early trading, weighed down by a combination of guidance that came in at the low end of prior expectations and a valuation backdrop that leaves little room for error. At roughly 2.5x book value, JPMorgan is trading at a premium relative to both peers and its own history, and even a “great but not perfect” quarter appears to be enough to trigger some profit-taking.

At the firmwide level , JPMorgan posted net income of $16.5 billion, up 13% year-over-year, translating to earnings per share of $5.94, comfortably ahead of consensus estimates. Revenue came in at $49.8 billion (or $50.5 billion on a managed basis), also topping expectations and rising 10% year-over-year. The strength was broad-based, with net interest income increasing 9% to $25.5 billion and noninterest revenue climbing 11% to $25.1 billion. Notably, markets revenue surged 20% to a record $11.6 billion, underscoring the firm’s ability to monetize volatility across asset classes.

Balance sheet growth remained solid, with average loans rising 11% year-over-year and deposits increasing 7%, reinforcing the view that JPMorgan continues to capture share across both consumer and institutional channels. However, expenses grew 14% to $26.9 billion, driven largely by higher compensation, marketing, and continued investment in growth initiatives. While this reflects a business operating at scale, it also highlights the cost of maintaining leadership in a competitive environment.

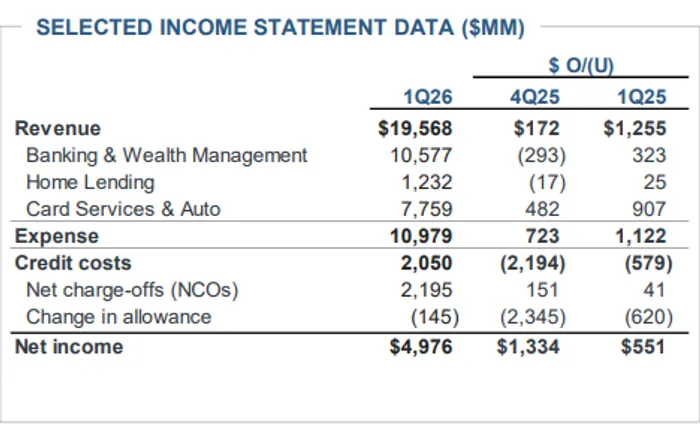

Breaking down the segments, the Consumer & Community Banking (CCB) division delivered steady, if unspectacular, growth. Net income rose 12% to $5.0 billion, while revenue increased 7% to $19.6 billion. The key driver here was Card Services, where higher revolving balances supported net interest income growth, alongside strength in auto lease income. Spending trends remained healthy, with debit and credit card volumes up 9% year-over-year, and mobile users continuing to grow. However, there were some signs of normalization beneath the surface, particularly in credit costs, where net charge-offs ticked higher, driven primarily by the card portfolio.

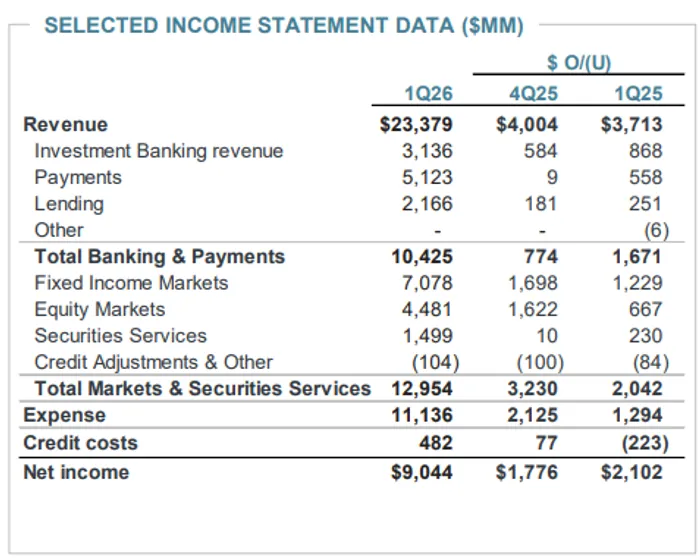

The Corporate & Investment Bank (CIB) was the clear standout this quarter. Net income surged 30% to $9.0 billion, with revenue up 19% to $23.4 billion. Investment banking fees jumped 28%, fueled by stronger advisory and equity underwriting activity, suggesting a rebound in capital markets engagement. Markets revenue was the headline driver, with fixed income trading up 21% and equities up 17%, reflecting strong client activity across commodities, credit, currencies, and emerging markets. This segment continues to benefit from elevated volatility, and the quarter reinforced JPMorgan’s dominant positioning in global trading and advisory.

Asset & Wealth Management (AWM) also contributed meaningfully, with revenue rising 11% and assets under management reaching $4.8 trillion, up 16% year-over-year. Net inflows remained robust, with $54 billion of long-term inflows, highlighting continued demand for both traditional and alternative investment products. Fee-based revenue growth in this segment remains a key structural driver for the firm, providing diversification away from rate-sensitive income streams.

On the credit side, the picture remains relatively stable but is showing early signs of normalization. The firm reported total credit costs of $2.5 billion, including $2.3 billion in net charge-offs and a modest $191 million reserve build. Importantly, reserve dynamics were mixed, with a build in wholesale portfolios offset by a release in consumer, suggesting divergent trends across lending categories. Net charge-offs were largely stable year-over-year, though consumer charge-offs—particularly in credit cards—continue to drift higher, a trend the market is watching closely.

Within CCB specifically, credit costs were $2.1 billion, with net charge-offs of $2.2 billion, up slightly year-over-year, again driven by card balances. However, the segment also saw a reserve release tied to improved housing conditions, providing some offset. In the CIB segment, credit costs were more contained, though reserve builds reflected some deterioration in select exposures, particularly in a more uncertain macro backdrop.

Jamie Dimon’s commentary largely reinforced themes that the market has already digested, particularly following his widely read annual letter released last week. He emphasized that the U.S. economy remains resilient, supported by strong consumer spending, fiscal stimulus, and ongoing investment in areas like artificial intelligence. At the same time, he reiterated a growing list of risks, including geopolitical tensions, energy price volatility, trade uncertainty, and elevated asset valuations. None of this is new, but it serves as a reminder that JPMorgan is operating in a late-cycle environment with increasing crosscurrents.

On the outlook, the key point of contention is net interest income. The firm now expects full-year NII of approximately $103 billion, which sits at the low end of its prior guidance range of $103 billion to $104.5 billion. While not a dramatic revision, the direction of change matters, particularly given that NII has been a primary earnings driver in recent quarters. The guidance reflects a combination of lower rate expectations, deposit mix shifts, and a more uncertain loan growth trajectory.

Elsewhere, JPMorgan reaffirmed its expectation for card services net charge-offs of around 3.4% and maintained its expense outlook at approximately $105 billion, signaling continued investment but also limited near-term operating leverage.

Ultimately, this was a high-quality quarter from an operational standpoint, with strength across nearly all business lines and continued evidence of franchise momentum. However, the stock reaction underscores a more nuanced reality: expectations were already high, valuation is stretched, and incremental positives are becoming harder to find. The combination of slightly softer NII guidance and a complex macro backdrop is enough to shift the risk-reward profile, at least in the near term.

For investors, the key question is less about what JPMorgan delivered this quarter and more about what it can deliver next. With the stock trading at a premium multiple and the macro environment becoming more uncertain, the bar remains elevated—and clearing it may require not just strong execution, but also a more supportive backdrop.