Situational Awareness LP's latest 13F shows 42 reportable entries with a total information-table value of about $13.68 billion for the quarter ended March 31, 2026. The surface read is dramatic: the largest disclosed line items are puts on the semiconductor ETF SMH, Nvidia, Oracle, Broadcom and AMD. The more useful read is subtler. The filing shows an AI-focused manager owning the physical layer of the buildout while carrying downside cover on the most crowded chip exposure.

The distinction matters because a 13F filing is not a live strategy dashboard. It is a delayed, partial disclosure of certain U.S.-listed securities and listed options. The SEC's Form 13F FAQ says institutional managers report issuer names, security class, shares owned and fair-market value. It does not disclose option premium, strike price, expiration date, delta, swaps, short sales, private holdings or cash. That makes the filing useful as a theme map, but weak as a profit-and-loss statement.

The Put Lines Are Big, But They Are Not The Whole Trade

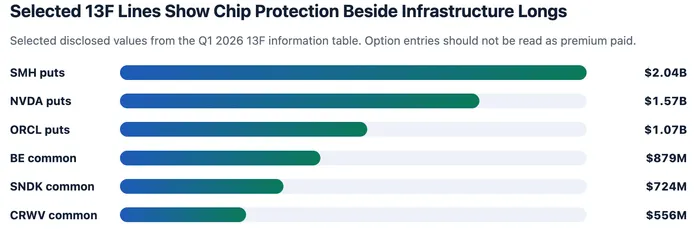

The SEC information table lists roughly $2.04 billion of SMH puts, $1.57 billion of Nvidia puts, $1.07 billion of Oracle puts, $1.01 billion of Broadcom puts and $969 million of AMD puts. It also lists put exposure tied to Micron, TSMC, ASML, Intel and Corning. Those are large numbers, but the reported value is tied to the underlying securities reported in the 13F table; it should not be read as the cash premium paid for options.

There are at least three cleaner interpretations than "he is short AI." The puts could be portfolio insurance against the same semiconductor beta that lifts AI infrastructure longs. They could protect against a rate-driven valuation reset in the most visible AI winners. They could also be event protection around chip earnings, Nvidia guidance or a crowded unwind in SMH. Without strike and expiry, the filing cannot tell which version is right.

Source: SEC Form 13F information table, quarter ended March 31, 2026. Chart uses selected entries only.

The Long Book Points To The Physical AI Stack

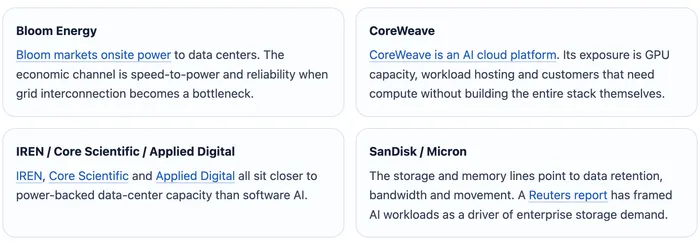

The common-stock side of the filing says something different. Situational Awareness reported about $879 million in Bloom Energy common stock, $724 million in SanDisk, $556 million in CoreWeave, $401 million in IREN, $389 million in Core Scientific and $320 million in Applied Digital. Those holdings are not just a generic "AI" basket. They point to the parts of the stack where physical scarcity can matter: electricity, data-center sites, GPU hosting, storage and memory-adjacent data movement.

The point is not that every infrastructure name has the same risk. Bloom is a power-availability trade. CoreWeave is a GPU cloud and financing trade. IREN, Core Scientific and Applied Digital are about turning energy-heavy sites into AI hosting capacity. SanDisk and Micron are exposed to a different lane: the memory, storage and data-movement load created by training and inference. That is a more informative structure than a one-line "long AI infrastructure" label.

Storage And Memory Are Their Own AI Profit Pool

SanDisk and Micron make the filing less like a pure GPU story. The Q1 table lists SanDisk common stock and calls, plus both Micron calls and puts. That combination is hard to reduce to a single bullish or bearish view. It suggests the manager is treating data storage and memory bandwidth as a separate AI profit pool, not merely as a derivative of Nvidia demand.

The economic channel is different from accelerators. GPU suppliers get paid when customers buy compute. Storage and memory suppliers get paid when AI workloads require larger data sets, faster retrieval, more enterprise SSD capacity, high-bandwidth memory and more movement across the data-center stack. The risk is also different: storage and memory can remain cyclical, and pricing power can fade if supply catches up. That makes the SanDisk and Micron lines a useful reminder that the AI buildout has several bottlenecks, not one.

The Filing Size And Intel Exit Are Reasons To Slow The Narrative

The size of the filing also needs discipline. 13F.info lists the Q1 2026 13F value at about $13.68 billion, up from about $5.52 billion in the Q4 2025 filing. That jump is eye-catching, but it should not be read as a clean quarterly investment return. A 13F value can grow because positions appreciate, because outside capital comes in, because more reportable securities are added, or because option notional values change.

The prior-quarter filing adds the same caution on timing. The Q4 2025 summary listed Intel calls among Situational Awareness' top holdings. The Q1 2026 SEC table no longer shows Intel calls; it shows a small Intel common position and a put position. That does not prove a bad trade or a missed trade. It simply shows why a 13F is a delayed theme map, not a real-time trading signal.

What The 13F Really Says About The AI Trade

One side of the filing owns physical bottlenecks: power, compute hosting, storage, memory and data-center capacity. The other side carries disclosed downside exposure on the most visible chip leaders and semiconductor beta. That is not a buy list, a short list or a complete portfolio. It is a partial map of how one manager split AI exposure between infrastructure scarcity and valuation risk.

The next useful question is not whether one put line went up or down after March 31. It is whether capital continues to chase the physical constraints behind AI: power availability, GPU hosting, storage intensity and memory bandwidth. If those bottlenecks keep tightening, the long book has a clear logic. If chip valuations reset faster than infrastructure economics improve, the disclosed puts look less like a contradiction and more like portfolio construction.