Marvell pushed the AI-chip debate beyond GPUs on May 27. The company reported record first-quarter fiscal 2027 revenue, guided the second quarter above consensus and, according to Reuters, said custom-chip revenue should top $10 billion in fiscal 2029.

The market had already rewarded AI silicon scarcity, but the prior assumption still centered on GPU platforms. Marvell's new target shifts attention toward custom XPUs, optical connectivity and data-center switching, where cloud customers try to tune AI infrastructure around power, bandwidth and cost.

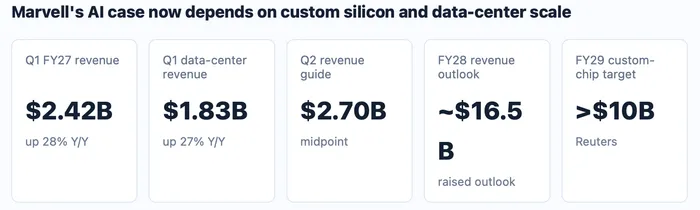

Provider and source are Marvell company releases, Marvell financial PDFs and Reuters via KELO-AM. This stitched comparison card uses Marvell's Q1 FY27 release, Marvell's financial and business results PDF, Marvell's additional earnings information PDF and Reuters via KELO-AM.

Data Center Revenue Is Now The Operating Proof

Marvell's operating base is no longer a small AI adjacency. The company reported $2.418 billion of Q1 revenue, up 28% from a year earlier, while its financial presentation said data-center revenue reached $1.833 billion, up 27% year over year and 11% sequentially.

That mix matters because the data-center line is where custom silicon, optical modules, Ethernet switching and interconnect demand meet hyperscaler AI spending. Marvell also said fiscal 2027 data-center revenue should grow about 50%, led by interconnect revenue growing more than 70%.

The counterpoint is concentration of expectations. If the data-center business slows, the custom-chip target becomes a longer-duration promise rather than current operating leverage. The next check is whether Q2 revenue, gross margin and order commentary confirm that the Q1 run rate is not just a front-loaded AI buildout.

The Custom-Chip Target Changes The Nvidia Read

Reuters reported that Marvell expects custom-chip revenue to exceed $10 billion in fiscal 2029, as cloud companies expand AI data centers and use custom chips to reduce reliance on Nvidia's processors. That does not make Marvell a GPU substitute; it makes the company a beneficiary of a broader architecture shift.

Custom ASICs and XPU-attach products matter when hyperscalers want workloads tuned to their own software, power budgets and network designs. Reuters also noted that Marvell and larger rival Broadcom help cloud-computing companies design custom chips for specific data-center needs. The read-through is therefore more disciplined than simply adding another AI ticker. Marvell needs design wins, attachment content and interconnect volume to turn the custom-chip target into revenue.

Guidance Raises The Bar For FY28

Management's near-term guide supports the longer target. Marvell guided second-quarter fiscal 2027 revenue to $2.700 billion plus or minus 5%, while Reuters said the midpoint was above the LSEG estimate of $2.60 billion and adjusted EPS guidance of $0.93 topped the $0.90 estimate.

The bigger change is the next fiscal year. Marvell's presentation said fiscal 2028 revenue is expected to grow about 45% to roughly $16.5 billion, about $1.5 billion higher than its prior outlook. That raises the burden from beating one quarter to showing that AI bookings can convert across several product lines.

Broadcom Remains The Benchmark, Not The Same Trade

Broadcom is the comparison point because it already frames custom silicon as a major AI revenue channel. Reuters described Broadcom as Marvell's larger rival in cloud custom-chip design, but the roles differ. Broadcom is the established scale benchmark; Marvell is the higher-duration catch-up case tied to new custom engagements, optical interconnects and switching content.

The distinction protects the analysis from lumping every semiconductor supplier into one AI basket. Nvidia remains the GPU platform leader, Broadcom is the ASIC scale reference and Marvell still needs custom XPU, XPU-attach and optical connectivity to become a multi-year revenue layer. Any miss in design-win timing or customer concentration would hit Marvell harder than a mature platform leader.

Cash Flow And Margins Decide Whether Bookings Become Quality

Marvell's Q1 showed more than top-line acceleration. The company reported $638.8 million of operating cash flow, a record high, and Q1 non-GAAP gross margin of 58.9%. The second-quarter outlook calls for non-GAAP gross margin of 58.25% to 59.25%.

Those figures are the validation path. Strong AI bookings help explain the raised outlook, but the market still needs revenue conversion, stable gross margin, operating cash flow and customer breadth. A stronger Q2 print and continued data-center guidance would support the repricing. Weaker margin quality, slower hyperscaler commitments or evidence that custom-chip demand is tied to too few customers would pull the story back toward execution risk.