Marvell Technology jumped more than 9% Monday after S&P Dow Jones Indices set MRVL for S&P 500 inclusion before the June 22 open, according to Reuters. Shares had already gained about 59% since May 27 after the company forecast a custom-chip business above $10 billion in fiscal 2029, so the index addition turns a fast AI infrastructure rally into a passive-demand event.

Eligibility was the first hurdle, not the whole story. Reuters said Marvell's addition followed GAAP profit in the December quarter and positive results over the latest four-quarter sum, while the official index announcement put the effective date before the June 22 open. The benchmark decision lowers one ownership barrier, but it also moves the debate from whether MRVL is eligible for the S&P 500 to whether the AI revenue base can justify a larger forced-holder audience after a sharp run.

Index demand is real, but it arrives after the stock already moved

S&P Dow Jones Indices said Marvell and Flex will join the S&P 500 to coincide with the quarterly rebalance and that the changes keep each index more representative of its market-cap range. The key market effect is not mysterious. Reuters said the move would trigger buying from index funds and ETFs required to hold constituents according to benchmark weights, creating a near-term demand source that does not depend on a fresh earnings surprise.

Passive demand can help absorb shares into June 22, but it arrives after the stock had already gained about 59% since May 27 and after a more than 9% Monday reaction. That sequence raises the evidence burden. A stock entering benchmark portfolios after a large AI-driven move is not being discovered from scratch; it is being handed to a broader holder base at a higher expectation level. The index bid can support ownership, but it cannot by itself show that the custom-chip target, data-center mix and margin path are still underpriced.

Effective-date mechanics matter less as a finish line than as a transfer of responsibility. Before inclusion, MRVL could trade mainly as a high-beta AI infrastructure supplier with a custom-silicon story. After inclusion, the same story sits inside S&P 500 funds, ETF models and benchmark-aware portfolios. Strong operating disclosures would make forced ownership look like a confirmation amplifier. Merely in-line numbers would make the same forced ownership look more like future evidence pulled into the current price.

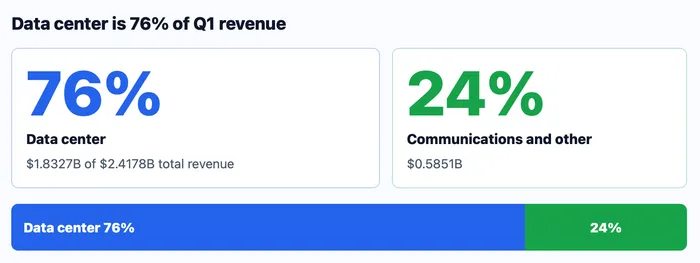

Data center concentration carries both upside and risk

Marvell's official release showed Q1 fiscal 2027 net revenue of $2.4178 billion, up 28% year over year, with data center revenue at $1.8327 billion, or 76% of total revenue. That mix is the key operating fact because it shows why the S&P addition is not only a liquidity event. MRVL is entering the index with most of its reported revenue already tied to data-center demand, so the market is effectively asking one segment to carry both the AI narrative and the new benchmark ownership base.

Source scope is Marvell official Q1 fiscal 2027 results for chart values. Symbol MRVL. Date range Q1 fiscal 2027 ended May 2 2026. Interval fiscal quarter. Basis reported revenue by end market. Context links include Marvell release, S&P Dow Jones Indices and Reuters via Investing.com.

Management guided Q2 revenue to $2.7 billion at the midpoint and said growth should accelerate through fiscal 2027, driven by data center strength. That guidance gives the growth argument a specific operating checkpoint, but it also narrows the margin for narrative error. If data-center sequential growth, gross-margin guidance or bookings commentary weakens, the issue would not be a small side business missing a plan. It would strike the segment now carrying three-quarters of revenue and most of the stock's AI valuation argument.

A 76% data-center share makes Marvell more directly exposed to AI infrastructure spending than a diversified chip supplier, which is why index inclusion can feel like benchmark recognition of a real business shift. The same number also means communications and other revenue can no longer cushion a data-center disappointment in the way a broader mix might. The stock is being added to the index at the moment when its operating identity has become more focused, not less.

Custom silicon must turn passive demand into operating evidence

Reuters linked the rally since May 27 to a forecast for custom-chip revenue above $10 billion in fiscal 2029.Marvell's own release pointed to demand across optics, switches, scale-up optical solutions, datacenter interconnect modules and custom XPU and XPU-attach solutions as reasons for stronger fiscal 2027 and fiscal 2028 outlooks. The optimistic case is therefore not just that Marvell sells into AI data centers; it is that custom compute, connectivity and optical attach become a larger, more durable part of cloud infrastructure budgets.

Competitive context needs precision. Reuters described Marvell and Broadcom as custom-chip designers for cloud-computing companies, while Nvidia remains the GPU platform benchmark those customers are trying to rely on less. MRVL is not the same AI signal as NVDA, and it is not simply a smaller version of Broadcom. Its read-through is narrower and depends on custom silicon, optical interconnect, switching and customer-specific data-center demand. That role can be attractive when hyperscalers keep diversifying compute architectures, but it also makes customer timing and program concentration much more important.

Marvell's own risk language already points to the weak spot. Marvell warned that major customers can become a significant portion of revenue and that customers may develop in-house or third-party alternatives. That does not negate the custom-chip opportunity, but it changes how the index event should be interpreted. Passive buying can create demand for MRVL shares; only customer orders, margin guidance and sustained data-center growth can show the business deserves that demand.

Useful checkpoints are concrete. June 22 index execution and post-inclusion volume will show how much mechanical demand was pulled into the rebalance. The upcoming fiscal Q2 result, data-center sequential growth, gross-margin guidance and any update to fiscal 2027 or fiscal 2028 AI bookings will show whether the operating story kept pace. A giveback would be easier to justify if index buying fades before management shows that $2.7 billion Q2 revenue guidance is still conservative, or if custom-chip commentary points to customer timing rather than broad demand.