Memory Became the Semiconductor Trade

Micron closed up 11.06% at $640.20 on May 5, but the rally was less a single-stock story than a signal for the whole memory chain. Western Digital rose 5.18% to $465.26, while Barron's said Sandisk gained 12% to $1,406.32. The rally is no longer just pricing a cyclical memory recovery; it is pricing memory as the next bottleneck in AI infrastructure.

IDC gave investors the data to make that shift explicit. The firm said total semiconductor revenue could reach $1.29 trillion in 2026, up 52.8% from $842.8 billion in 2025, with AI infrastructure reshaping demand across the chip market. Micron remains the cleanest U.S. ticker for the argument, but the trade now reaches DRAM pricing, HBM allocations, NAND storage demand, Sandisk and Western Digital, and the supply constraints that can affect Nvidia and AMD accelerator platforms.

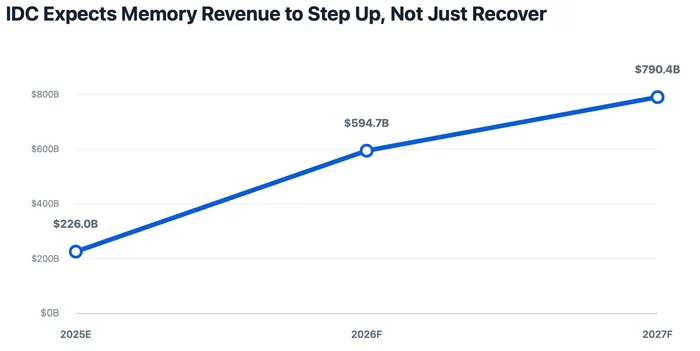

Source: IDC Semiconductor & Semiconductor Applications Forecast, April 2026, as summarized by IDC. Values are total memory revenue forecasts in billions of dollars.

The Rally Is Pricing a Bottleneck

Investors are no longer valuing memory suppliers only as cyclical beneficiaries of better spot and contract prices. The stronger claim is that suppliers can earn closer to scarce-infrastructure economics while AI customers compete for capacity, and IDC's forecast gives that argument scale: total memory revenue rising from $226 billion in 2025 to $594.7 billion in 2026, then to $790.4 billion in 2027.

DRAM carries the clearest earnings implication. IDC expects $418.6 billion of DRAM revenue in 2026, up 177% year over year, driven by high-bandwidth memory and DDR demand from hyperscalers and AI infrastructure providers. High-bandwidth memory is the tightest version of that story, with IDC saying most HBM capacity is already pre-committed through 2026 and forward allocations extending into 2027.

HBM also changes the economics of the rest of the portfolio. Advanced packaging, stacking and higher silicon-area requirements can tighten standard DRAM availability even when consumer-device demand is weak, which is why investors need to separate bit-volume growth from value growth.

Scarcity Still Has a Consumer Offset

A cleaner bottleneck narrative can hide a messier end-market split. TrendForce expects conventional DRAM contract prices to rise 58% to 63% quarter over quarter in 2Q26, and NAND Flash contract prices to rise 70% to 75%, but those gains come partly from capacity being pulled away from weaker consumer channels.

IDC's device-market work shows the cost transfer is already visible. The firm forecast the PC market to decline 11.3% in 2026 while revenue rises 1.6% because of higher average selling prices, and it expects smartphones to decline 12.9% in units. That mix matters for stock selection: memory makers benefit when hyperscalers lock in scarce supply, but PC, smartphone and device OEMs can face margin pressure, weaker unit demand or lower memory configurations if they cannot pass costs through.

NAND Broadens the Asset Map

NAND gives the memory rally a broader data-center angle. IDC forecasts NAND Flash revenue of $174.1 billion in 2026, up 138.5% from 2025, with AI training datasets, checkpoint storage and high-performance inference environments driving demand. Micron reinforced that point on the product side, saying on May 5 that it is shipping the 245TB Micron 6600 ION SSD for AI, cloud, enterprise and hyperscale workloads.

Storage is not the same trade as HBM, but it strengthens the thesis that AI infrastructure is pulling memory deeper into system design. If data lakes, inference workloads and object storage keep absorbing enterprise SSD capacity, NAND pricing can remain more resilient than a normal consumer-cycle recovery would imply.

Micron is the most direct U.S. stock expression of the DRAM and NAND repricing argument. Sandisk adds higher beta NAND exposure after its Western Digital separation, while Western Digital remains tied to storage demand and data-center capacity choices. Nvidia and AMD sit on the other side of the constraint: tight HBM supply can support allocation discipline and accelerator pricing, but it can also limit platform shipments if memory supply becomes the gating item rather than compute silicon.

What Could Break the Memory Rally

AI infrastructure is repricing memory from a background component into a strategic constraint. The trade can keep working if forward allocations, contract pricing, Micron margin guidance and enterprise SSD demand stay tight. It becomes more fragile if new capacity arrives faster, consumer-device weakness spreads, or Nvidia and AMD stop talking about HBM as a limiting factor.