For investors who spent the past decade treating size as a safety blanket, the market’s latest message is becoming harder to ignore: small and micro cap stocks are no longer sitting quietly in the cheap seats. “Come for the valuation, stay for the alpha,” Chris Tessin, managing partner, chief investment officer and co-founder of Acuitas Investments, said in an interview with AInvest’s Capital & Power.

Tessin warned investors to think big by “not ignoring small and micro-cap stocks,” a corner of the market that he said has been overshadowed by largecap dominance for more than 15 years.

“I think we’re at a pretty notable inflection point,” Tessin told Capital & Power. “People are becoming aware of and taking note of the rise of smallcap... They’d have been well rewarded, incredibly well rewarded over the past year by investing in small and micro-cap stocks.”

_c8940cd71780087260840.jpg?format=webp&width=700)

Recent market performance has strengthened that argument. Reuters reported in February that the Russell 2000 had significantly outperformed the S&P 500 and Nasdaq so far in 2026, while also noting gains in chipmakers and AI-related companies. Barron’s reported Friday that the Russell 2000 was up 17% year to date and 41% over the past 12 months, compared with gains of 11% and 29%, respectively, for the S&P 500.

For Tessin, the opportunity is not simply that smaller stocks have rallied. It is that the market remains inefficient enough for skilled managers to find businesses that larger institutions often overlook.

“Our view is that active investment is a better stance than passive investment because the richest place for active management is down in small and microcap,” Tessin told Capital & Power. “You’re simply not trying to duke it out with as many institutional investors.”

Micro-cap investing, Tessin said, is often misunderstood. He said Acuitas views microcap more in line with the Russell Microcap index, where companies can include businesses near or above $1 billion in market value, rather than only speculative startups or tiny local companies.

“True microcap is a lot more expansive than I think people are thinking about,” Tessin said. “It’s not the corner bodega. It is companies with billions of dollars in many cases of revenue and a notable footprint, sometimes an international footprint.”

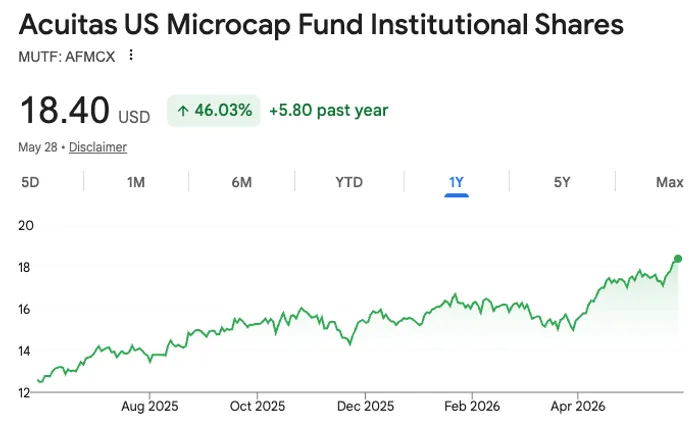

Acuitas has tried to package that opportunity through active, multi-manager products. Tessin said the firm’s U.S. microcap mutual fund, ticker AFMCX, uses a multi-manager structure in which Acuitas researches institutional investment managers, allocates capital among them and balances the overall portfolio.

In small caps, Tessin said Acuitas recently launched the Acuitas Small Cap Active ETF, ticker AIMS, on Nasdaq, using six underlying managers across growth, core and value styles.

The case rests partly on valuation. Tessin said smallcaps have traded at “a significant discount” and still lag largecaps over a 10-year period, even after their recent run. He also pointed to smaller chipmakers, power generation, materials, energy, biotechnology, healthcare and software as areas where active managers are finding opportunities tied to broader market themes, including artificial-intelligence infrastructure and healthcare deal activity.

Tessin said that Acuitas views small cap as “the richest pond for someone to fish in.”

The opportunity comes with risk. Smaller companies can be more volatile, less liquid and more sensitive to changes in credit conditions than larger companies. Tessin did not present a guaranteed return target and said Acuitas’ goal is to outperform small-cap benchmarks such as the Russell 2000 over time.

Still, the recent broadening of the market has given investors a reason to revisit an asset class many had written off. As Tessin put it, “Not every company goes public at a trillion dollars.”