Modine Manufacturing suddenly has a more explicit AI infrastructure revenue lane. Investing.com reported MOD shares jumped 14% Tuesday after Modine said a strategic data center customer will receive guaranteed Airedale by Modine cooling capacity for more than $4 billion of products during calendar years 2027 through 2029.

Capacity for sale is still not recognized sales. Modine said the customer paid $165 million upfront in cash to support construction costs, while the company's fiscal 2026 release showed fiscal 2026 net sales of $3.181 billion and Climate Solutions net sales of $2.062 billion. Market enthusiasm is therefore shifting toward physical AI capacity, but the new agreement still has to convert into shipments, margin and free cash flow.

Capacity Agreement Pulls Cooling Into AI Capex

The agreement moves data center cooling from background equipment into a scheduled capacity commitment. The customer is unnamed, the products will run through Modine's Airedale cooling platform, and the more-than-$4 billion figure covers product supply over three calendar years, not a single year of revenue recognition.

A $165 million upfront payment is the clearest operating detail. Customer-funded cash lowers some expansion strain, yet it also tells readers that capacity is the bottleneck being purchased. Prior assumptions treated AI infrastructure upside as mostly a chip, power and cloud-platform story. Modine's announcement pushes part of that spending map into thermal management hardware.

Execution risk sits inside the same fact pattern. Guaranteed capacity can support growth only if facilities ramp, costs stay controlled and shipment timing matches the customer's buildout. The deal changes Modine's opportunity set, but it does not remove construction, utilization or customer concentration risk.

Source scope uses Modine's official FY2026 results for asset MOD, date range fiscal year ended March 31, 2026, interval annual, basis reported segment net sales in billions of dollars from Modine.

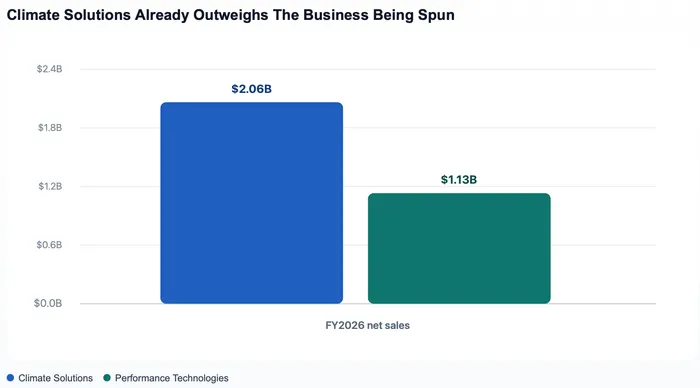

Climate Solutions Already Carries The Revenue Weight

Fiscal 2026 results show why the capacity agreement lands on a company that has already been reshaped. Modine reported total net sales rose 23% to $3.181 billion, while Climate Solutions net sales rose 42% to $2.062 billion. Performance Technologies net sales were $1.132 billion, making the cooling-heavy segment the larger revenue base before the latest Airedale agreement starts contributing.

Climate Solutions also delivered adjusted EBITDA of $377.1 million in fiscal 2026, compared with $156.5 million for Performance Technologies. Modine has announced a pending spin-off of Performance Technologies, so the revenue base left behind is tilted toward data center cooling, indoor air quality and heat-transfer systems.

Segment scale is the mechanism behind the stock reaction. A diversified industrial thermal company can get valued on machinery cycles; a company with visible data center cooling capacity can get valued on AI infrastructure duration. Modine still has to earn that shift through delivery, but the revenue base no longer makes cooling a small side note.

Margin And Cash Flow Keep The Rally Honest

Gross margin kept the announcement from becoming a one-direction story. The same release said fourth-quarter gross margin declined 320 basis points to 22.5%, with tariff impacts, higher material costs and manufacturing costs tied to Data Centers expansion among the pressures. Data center growth is useful only if scale absorbs those costs rather than pushing them forward.

Free cash flow added the second hurdle. Modine reported fiscal 2026 free cash flow of $105.4 million, down from $129.3 million a year earlier, because higher working capital and capital spending tied to Data Centers growth outweighed part of the benefit from customer deposits. The $165 million upfront payment is helpful, but it is not the same as effortless cash conversion.

That balance explains why the stock move still has an earnings hurdle. A large customer commitment expands the Climate Solutions revenue opportunity; margin compression and capital needs decide how much of that opportunity reaches operating income and free cash flow.

Future Filings Need Shipments, Not Just Capacity

Modine's fiscal 2027 outlook gives the first checkpoint. Management projected fiscal 2027 net sales growth of 20% to 35% and adjusted EBITDA of $650 million to $680 million, citing a strong order book and capacity expansion that remains on track. Those guideposts now carry more weight because they have to bridge reported fiscal 2026 results with the 2027 through 2029 Airedale capacity window.

Confirmation should show up in shipment cadence, gross margin recovery, working-capital discipline and any disclosure that broadens the customer base. A delay in capacity buildout, another step-down in gross margin or persistent cash drag would make the $4 billion figure look more like headline capacity than economic throughput.

MOD's next reports will decide whether that rerating can hold. Cooling has moved from background equipment to capacity reserved years in advance, and useful confirmation will be Airedale shipment cadence, Climate Solutions margin recovery and free cash flow that rises with the capacity base. Without those disclosures, the sourced $4 billion path remains a capacity promise instead of delivered economic throughput.