By mid-May 2026, the S&P 500 and Nasdaq Composite have repeatedly established new all-time highs, with the Philadelphia Semiconductor Index (SOX) significantly outperforming the broader market. This surge reflects deep investor optimism regarding artificial intelligence commercialization. However, the macroeconomic foundation contradicts this equity rally. The April Consumer Price Index (CPI) rose 3.8% year-over-year, marking the highest level since May 2023. Furthermore, the Producer Price Index (PPI) surged 6.0% annually, indicating severe price pressures at the wholesale level. The divergence between market valuations and economic reality is widening rapidly. Based on these conflicting signals, investors must immediately reassess three critical macroeconomic risks before adding further exposure to long-duration equity assets.

The Inflation Resurgence and the New Federal Reserve Era

The primary risk factor is the clear secondary wave of inflation colliding with a leadership transition at the Federal Reserve. The April inflation data eliminated the narrative of a linear path back to the central bank's target. The 3.8% headline CPI reading was heavily driven by a 17.9% year-over-year jump in energy costs, with gasoline prices specifically soaring 28.4%. Concurrently, the core CPI remains elevated at 2.8%. The data also contained negative signals for the broader economy, as real average hourly wages slipped 0.5% for the month.

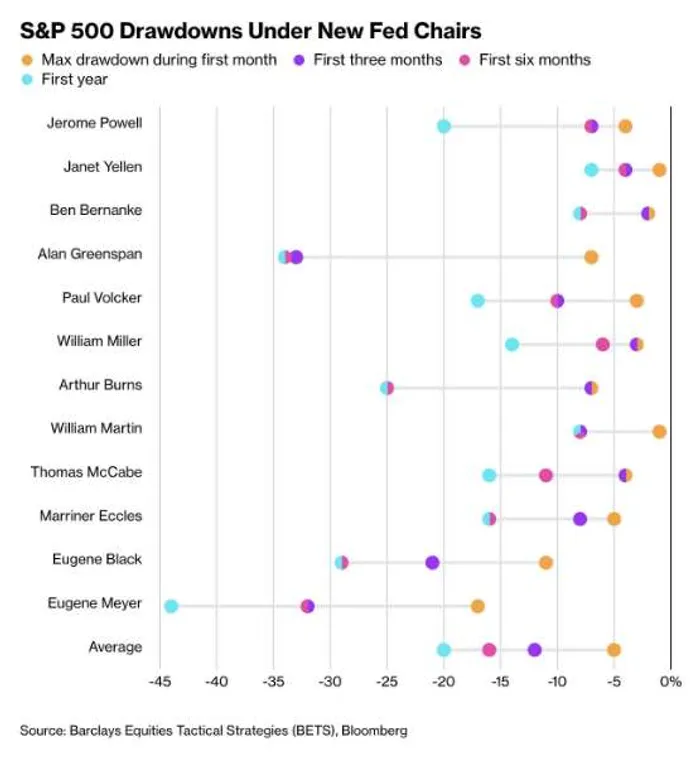

This data arrives just as the U.S. Senate confirmed Kevin Warsh to succeed Jerome Powell as Federal Reserve Chair with a 54-45 vote. Warsh assumes control in a highly constrained environment. On one side, he faces intense pressure from the Trump administration for accelerated rate cuts to stimulate the economy. On the other, the 6.0% annual PPI growth, driven by a 7.8% monthly spike in energy costs, removes any data-driven justification for aggressive easing. According to Ainvest analysis, historical data tracking S&P 500 drawdowns under new Fed Chairs indicates that leadership changes often introduce elevated market volatility. Consequently, markets are rapidly repricing the probability of 2026 rate cuts, which applies immediate downward pressure on the valuations of growth equities that rely heavily on a dovish monetary policy framework.

The 30-Year Treasury Yield Returns to 5%

The second major headwind is the persistent upward shift in the long-term interest rate structure. In mid-May, the yield on the 30-year U.S. Treasury bond returned to the 5% threshold, reaching approximately 5.03%. This is substantially higher than the 4.74% long-term average and marks a notable increase from the 4.89% level recorded a year prior. A recent sale of $25 billion in 30-year bonds demonstrated steady demand, with investors submitting bids for 2.3 times the amount offered. For long-term investors, such as insurers and pension funds, a 5% risk-free rate presents a highly attractive alternative to the equity market.

In the context of equity valuation, this upward shift in the risk-free rate directly compresses the equity risk premium. High-beta assets, particularly artificial intelligence and semiconductor stocks tracked by the SOX, are extremely sensitive to discount rate assumptions. Even a marginal increase in the 30-year yield from 4.5% to 5.0% mathematically forces a double-digit percentage contraction in the intrinsic value of these long-duration cash flow assets. The April PPI and CPI reports have reinforced the higher-for-longer rate narrative, sharply contrasting with the aggressive rate cut expectations held by the consensus earlier this year.

Energy Shocks and Midterm Election Volatility

The third risk factor combines severe geopolitical energy disruptions with the inherent instability of the 2026 midterm election cycle. The geopolitical landscape fractured in late February 2026, following U.S. and Israeli airstrikes and the assassination of Iran's supreme leader. This triggered an Iranian blockade of the Strait of Hormuz, instantly threatening approximately one-quarter of global seaborne crude oil and one-fifth of liquefied natural gas shipments. Consequently, Brent crude oil prices breached the $100 per barrel mark, peaking near $126 and establishing the highest levels in four years.

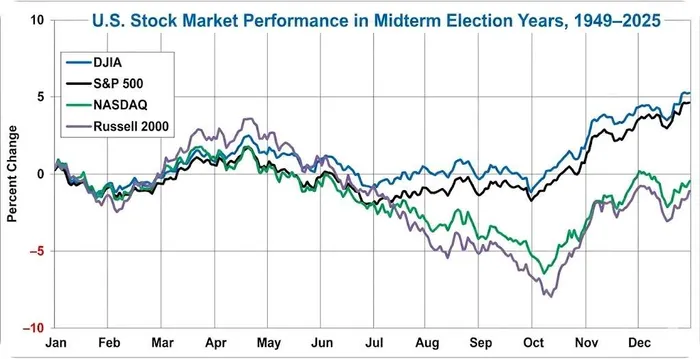

This energy shock is a direct catalyst for the current inflation spike and threatens corporate profit margins, particularly in energy-intensive sectors like aviation, transportation, and chemical manufacturing. Furthermore, 2026 is a midterm election year in the United States. According to Ainvest analysis detailing U.S. stock market performance in midterm election years from 1949 to 2025, the months leading up to the third quarter typically exhibit the weakest average returns of the four-year presidential cycle, often characterized by drawdowns of 2% to 8%. The convergence of the Hormuz crisis and the political polarization of the midterms suggests that heightened downside volatility is highly probable in the coming months.

Profitability and Trade Negotiations Provide a Buffer

Despite these significant macroeconomic pressures, the equity market retains foundational support from tangible artificial intelligence monetization and potential trade developments. Unlike previous technological cycles, AI is generating substantial, verifiable cash flows. For example, Anthropic achieved an Annual Recurring Revenue of approximately $5 billion in 2025, a massive acceleration from roughly $200 million in 2024, supporting its $183 billion valuation. Major technology corporations are also explicitly quantifying the revenue and profit contributions from generative AI integration within their software divisions, proving the commercialization phase is actively materializing.

Additionally, President Trump and President Xi Jinping are scheduled to meet in Beijing from May 14 to 15. The agenda includes discussions on AI chip export controls, agricultural purchases, and large aircraft acquisitions. If these negotiations produce a phased procurement agreement, particularly involving Boeing aircraft and agricultural products, the resulting influx of export orders could partially insulate the U.S. manufacturing sector from the dual headwinds of high interest rates and global supply chain disruptions.

Conclusion

The combination of a 3.8% CPI, a new Federal Reserve Chair, 5% long-term bond yields, and severe geopolitical energy shocks acts as a strict stress test for the current technology bull market. However, authentic AI monetization and pending U.S.-China trade developments offer downside protection. Investors should avoid binary portfolio decisions, instead focusing on adjusting duration exposure to navigate the structural volatility inherent in the 2026 market environment.