The headline is that NuScale Power added a former Nuclear Regulatory Commission chairman to its board and the nuclear theme is back. The headline does not mention that the stock is down roughly 80% from its 2025 highs, that revenue collapsed from $13.4 million to $0.6 million in the latest quarter, or that the company's estimated cash runway - approximately 2.44 years - is shorter than the timeline to first commercial reactor delivery.

The question isn't whether the board hire is impressive. It's whether a governance upgrade changes the math for a company that burns cash faster than it generates it.

NuScale Power (NYSE: SMR) announced on May 29 that it welcomed two new directors at its annual meeting, which wrapped June 2. Dr. Dale E. Klein served as NRC chairman from 2006 to 2009, appointed by President George W. Bush, and is a professor emeritus at the University of Texas. Stuart Harshaw brings mining and metals leadership, most recently as CEO of Nickel Creek Platinum, a company that extracts platinum group metals - materials used in nuclear reactor components.

The market narrative is clear: regulatory credibility plus commodity expertise equals de-risked commercialization. The counter-narrative, which the quarterly numbers support, is that neither director brings revenue, and the runway clock is already ticking.

Here is the factor stack that matters more than the press release.

Valuation: No revenue, $4.7 billion market cap. SMR trades at roughly $13 per share for a $4.7 billion market capitalization. That is the valuation of a company generating actual cash flow, not one that reported $0.6 million in quarterly revenue - a 95.5% drop from the same quarter a year ago. In nuclear peer terms, NuScale is the only small modular reactor company with an NRC-certified design, which gives it a structural edge. It also means it is the most expensive one to hold while waiting for that edge to monetize. A first-mover advantage is valuable until it is the only thing you have.

Growth: Revenue contraction, not pre-revenue patience. Q1 2026 came in at a loss of $0.14 per share, wider than the consensus estimate of $0.11. Revenue and cost of sales both dropped - by $12.8 million and $5.8 million respectively versus the prior-year quarter. The cost discipline is real, but revenue of $600,000 in a quarter means the business model is still a slide deck, not a cash register. You can cut costs down to a skeleton, but you cannot scale a skeleton into a business.

Momentum: The sector is hot, the stock is cold. The nuclear theme has been the most durable rally of 2026, buoyed by AI data center power demand, IEA reports pushing SMRs as the next era of nuclear, and sector-wide event flow. SMR popped 7% on May 26 and jumped 11.6% on May 6 on DOE loan and deal news. But the 52-week range - $8.85 to $57.42 - tells the real story. The stock has spent most of 2026 grinding lower, and the rallies have been quick, shallow, and bought by momentum traders who sell on the first sign of weakness. Sector momentum helps, but it does not replace earnings. A tailwind lifts all boats until you realize yours has a hole in it.

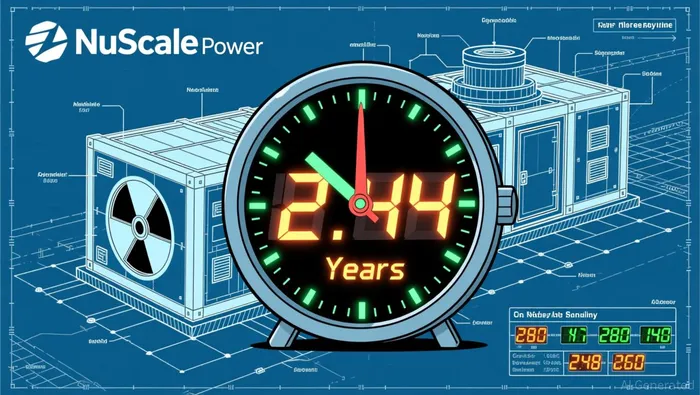

Liquidity: The 2.44-year clock. This is the number the board announcement does not address. A roughly 2.44-year cash runway means NuScale will need another capital raise - dilutive, because the company has no revenue to support a debt offering - well before its first reactor reaches commercial operation. One analyst noted earlier this year that cash runway relative to the commercialization timeline is the single most important metric for SMR stocks. The comparison is unforgiving: Nano Nuclear Energy, a smaller player, was cited at 14.5 years of runway versus NuScale's 2.44. That is not a slight difference. That is a difference between breathing and suffocating.

Governance: The board hires are real, but they are not a thesis. Klein's NRC background matters for regulatory navigation - the path from certified design to operating license is where NuScale now lives. Harshaw's mining background matters for the supply chain - fuel fabrication and materials sourcing are non-trivial for a company building its first plants. But governance upgrades do not print revenue. They reduce the risk of catastrophic missteps. That is valuable. It is not the same as being investable today.

What changes the story: A binding customer contract with a utility or data center operator, a confirmed DOE loan guarantee closing with attached milestones, or a capital raise structure that extends the runway to 4+ years without excessive dilution. Until one of those three appears, the factor stack reads as a governance improvement on a fundamentally deteriorating balance sheet.

The nuclear theme is real. The AI-power-demand narrative has legs. But NuScale is the wrong part of the story to hold while waiting for it to play out - unless you are comfortable with the risk that the capital raise comes, the shares dilute, and the stock reprices lower despite better headlines. A better-positioned name in the same theme would be one with contracts, revenue, or a longer runway. NuScale has the certification and the board. It does not yet have the cash.

If you are already in SMR, the Klein and Harshaw appointments are not a reason to add. They are a reason to keep watching - and to watch the cash number with the same intensity you would watch a commercial contract announcement. The former NRC chairman makes the board look better. He does not make the balance sheet look safer. Those are two different things, and the market will eventually price the difference.