The most important story in the U.S. stock market was not the daily move in the major indexes. It was Nvidia's earnings report after the close. The company once again delivered a quarter that most businesses would call extraordinary: record revenue, explosive data-center growth, high margins and a revenue outlook above Wall Street's forecast. Yet the stock slipped slightly in after-hours trading. That tension is the real story.

The beat was real

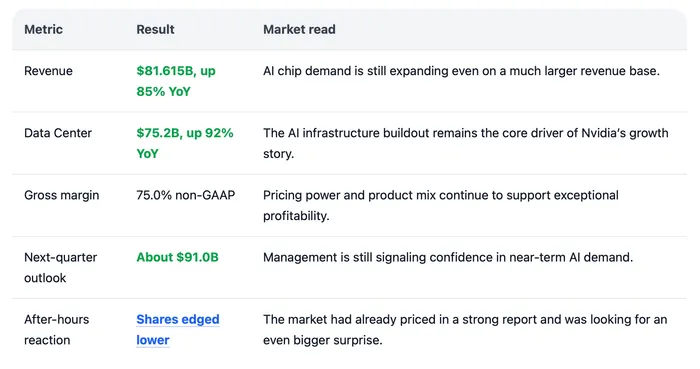

Nvidia reported revenue of $81.615 billion for the quarter ended April 26, 2026, a 20% increase from the previous quarter and an 85% increase from a year earlier. Data Center revenue reached $75.2 billion, up 21% sequentially and 92% year over year, showing that demand for AI infrastructure remains the compan's central growth engine.

Profitability also stayed at a level that few large-cap companies can match. Nvidia said GAAP diluted earnings per share were $2.39, while non-GAAP diluted earnings per share were $1.87. Non-GAAP gross margin was 75.0%. The company also guided for roughly $91.0 billion in revenue for the next quarter, with management noting that the outlook does not assume Data Center compute revenue from China.

A note on EPS: Nvidia's own release reported non-GAAP diluted EPS of $1.87. The Associated Press, using a different adjusted-earnings convention tied to FactSet comparisons, reported EPS excluding one-time items of $1.76, slightly above the $1.75 analyst estimate. The difference is about reporting methodology rather than a contradiction in the business result.

The stock reaction was not a contradiction

For many companies, a revenue beat and a stronger-than-expected outlook would be enough to push the stock higher. Nvidia is not being treated like an ordinary company. It has become the pricing anchor for the AI trade, the company investors look to when they want to judge whether the spending boom behind artificial intelligence is still alive.

Investors were not simply asking whether Nvidia is growing. They were asking whether it can keep compounding at a pace that justifies one of the most demanding valuation narratives in the market. A strong quarter can still feel fully priced when the market has already assumed strength.

The AI trade is maturing

The early AI debate centered on whether large language models and generative AI tools would create a durable need for computing power. Nvidia's Data Center results have largely answered that question. Cloud providers, internet platforms, AI-native companies and enterprises are still building the infrastructure needed to train, deploy and scale advanced models.

The market's attention is moving to a harder question: how quickly that spending turns into revenue, margins and productivity for Nvidia's customers. Hyperscalers can keep buying chips for a long time, but public-market investors will increasingly want to see the return on that capital expenditure. The stronger Nvidia becomes, the more the market will also watch for pressure from custom chips, inference-focused alternatives, export restrictions and shifts in customer spending cycles.

None of those risks removes Nvidia's leadership position today. They do, however, shape the valuation premium investors are willing to pay. Nvidia's earnings release is no longer just a company update. It has become a stress test for the entire AI supply chain.

What matters after the report

Nvidia's latest quarter reinforced its position at the center of AI infrastructure. The Data Center line remains the clearest signal: if that business keeps expanding at a high rate, the broader AI infrastructure story remains intact. The real question is no longer whether demand exists, but how much growth remains after the revenue base has become enormous.

Margins will carry almost as much weight. Nvidia's elevated gross margin reflects the value of the full platform — GPUs, networking, systems, software and the ecosystem customers are willing to pay for. Any sustained pressure would tell the market that competition, product transitions or customer bargaining power is starting to matter more.

Guidance is likely to be the most sensitive part of future reports. The stock's slight after-hours decline is better read as a valuation signal than an earnings disappointment: Nvidia remains strong, but the market has become more demanding.

For the AI trade to keep working, investors will need evidence that massive infrastructure spending can keep translating into durable profits, cloud revenue and real productivity gains. Nvidia delivered another exceptional quarter, but investors have moved past asking whether the company is exceptional. They now want proof that exceptional can continue to scale.