President Donald Trump arrived in Beijing on May 13 for talks with Chinese President Xi Jinping, and Nvidia CEO Jensen Huang was part of the business delegation. For markets, Huang's presence puts H200 export rules near the center of the trip. It makes Nvidia's China access the cleanest test of whether U.S.-China technology tensions are shifting from a hard ban to negotiated access.

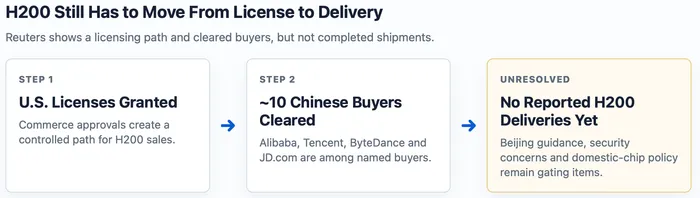

Investors are not pricing a finished sale yet. Reuters reported on May 14 that the U.S. had cleared around 10 Chinese firms to buy Nvidia's H200 chips, while no delivery had been made so far. That is the repricing gap: H200 is back in the policy conversation, but it is not yet back in revenue.

The market reaction already shows why the story matters. Nvidia advanced 2.3% on May 13 as the S&P 500 gained 0.58% and the Nasdaq Composite rose 1.20%, with AI-linked technology shares helping indexes look past hotter inflation data. The rally was not only about one chip license. It was about whether China can again become a source of upside for the AI hardware trade.

Source: Reuters reporting on May 14, 2026. Counts reflect reported approvals and delivery status, not chip volumes, revenue or market returns.

Licenses Have Replaced Ban Risk

Earlier in the chip-control cycle, the market's main assumption was simple: advanced Nvidia data-center chips could not reach China in commercially meaningful volume. Current reporting changes that setup. U.S. approval for about 10 buyers means Washington has created a route, even if the route is narrow and conditional.

That matters for Nvidia because the stock has already been valued as the central vehicle for global AI compute demand. A potential China reopening does not need to dominate the revenue model to move the shares. It only needs to convince investors that an excluded market could become a source of estimate upside.

Still, the distinction between license and delivery is the article's core market issue. Permission from Washington lowers one barrier. It does not settle Chinese import approval, customer willingness, shipment timing, inventory allocation or revenue recognition.

Beijing Still Controls the Gate

Approved buyers include Alibaba, Tencent, ByteDance and JD.com, while Lenovo and Foxconn were approved as intermediaries. The same report said each approved customer can buy up to 75,000 chips under U.S. license terms. Those details are large enough to matter, but they also explain why the transaction is politically sensitive.

The H200 path is constrained by security procedures, military-use limits, U.S. inventory certification and a 25% U.S. revenue-share arrangement. Reuters also reported that Chinese firms pulled back after guidance from Beijing and that pressure is mounting inside China to block or tightly vet orders.

That makes H200 a visible policy lever, not a completed bargain. Washington can point to regulated commercial access and a revenue-share structure. Beijing can still slow the path through regulatory guidance, security reviews and support for domestic chips.

Nvidia Gets Optionality, Not Guidance Yet

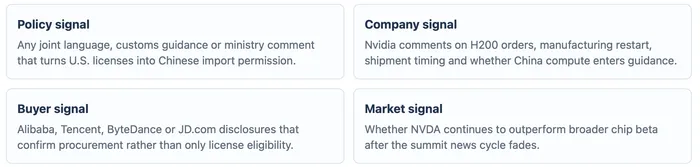

Nvidia's own outlook explains why the setup can move estimates. The company guided first-quarter fiscal 2027 revenue to $78.0 billion, plus or minus 2%, and said it was not assuming any Data Center compute revenue from China. If shipments restart in size, investors would have a reason to revisit that zero-China assumption.

The base business is already huge. Nvidia reported fiscal 2026 revenue of $215.9 billion, up 65%, and fourth-quarter Data Center revenue of $62.3 billion. Against that scale, early H200 shipments would probably be treated first as incremental upside and strategic relief, not as a complete reset of the model.

H200 also sits in a specific product lane. It is not the newest Blackwell or Rubin platform. But Reuters previously reported that H200 delivers roughly six times the performance of Nvidia's China-oriented H20 chip. That makes it meaningful for Chinese AI buyers and meaningful for Nvidia's attempt to defend its ecosystem.

Chinese AI Buyers Need Capacity, but Beijing Needs Leverage

Alibaba, Tencent, ByteDance and JD.com all sit in markets where AI models, cloud workloads, recommendation systems and consumer applications compete on access to compute. Faster accelerators can lower training and inference constraints, especially for companies trying to narrow gaps with U.S. AI platforms.

Beijing has a different calculation. Allowing H200 imports could relieve near-term compute bottlenecks, but it may also slow the domestic substitution push around Huawei and other local chip suppliers. Regulatory guidance, security concerns and domestic-chip policy are therefore not side issues. They are the gap between a U.S. license and a delivered H200.

The summit therefore matters less as a ceremonial meeting than as a venue for sequencing. If China wants leverage, it can allow a limited batch, attach domestic-chip conditions or delay customs flow. If Washington wants sales without looking soft on security, it can keep licenses narrow and compliance-heavy.

The Read-Through Is Wider Than Nvidia

Nvidia is the first-order trade because the H200 is its product and Huang is in Beijing. AMD and other accelerator suppliers may also get attention if investors believe U.S. chip policy is moving toward controlled commercial access rather than blanket exclusion. Today's verified reporting, though, is Nvidia-specific.

Chinese internet stocks are a second-order channel. If H200 imports actually clear, the market may revisit AI infrastructure constraints for Alibaba, Tencent, ByteDance and JD.com. If Beijing keeps pressure on buyers to favor domestic alternatives, the benefit shifts toward local chip suppliers and away from U.S. exporters.

Semiconductor ETFs can rally on the optics, but the quality of the move matters. A broad chip bid based only on summit headlines is less durable than one supported by named licenses, import approvals, shipment schedules and a visible change in Nvidia's China revenue assumption.

Delivery Is the Confirmation Point

The clean confirmation is not another summit headline. It is a sequence of harder evidence: public Chinese import clearance, customer purchase orders, Nvidia shipment timing, inventory allocation and eventual revenue recognition. Without those steps, H200 remains an option in the share price rather than a line in the income statement.

For now, Huang's trip tells investors that AI chips are on the negotiating table. It does not prove that H200 units are crossing the border. That distinction should define the trade: a stronger China option for Nvidia, but one that still needs delivery evidence before it deserves to become earnings upside.