Nvidia's May 20 earnings have become the cleanest test of whether the AI rally can still outrun the bond market. Reuters reported that U.S. stocks pulled back on Friday as oil and Treasury yields rose, with the 10-year yield touching 4.58% and the Philadelphia Semiconductor Index falling sharply. The question for Nvidia is no longer just whether AI demand is strong. It is whether the next guide can lift earnings expectations enough to absorb a higher valuation hurdle.

Nvidia says it will report first-quarter fiscal 2027 results on Wednesday, May 20, at 2 p.m. Pacific time. That makes the report a market-wide checkpoint: yields are pressing high-multiple technology shares, oil has revived inflation concern, and the semiconductor tape has already shown where a discount-rate shock can land first.

Sources: Reuters via Global Banking & Finance Review for Friday NVDA, SOX and Nasdaq moves; Reuters via MarketScreener for the 10-year Treasury yield. Values are reported market snapshots, not a live OpenBB series.

The Operating Bar Is Data Center Revenue Plus Margin Quality

Official company numbers set a demanding baseline. Nvidia said fiscal fourth-quarter revenue was $68.1 billion, while Data Center revenue was $62.3 billion, up 75% from a year earlier. It also guided fiscal first-quarter revenue to $78.0 billion, plus or minus 2%, with GAAP and non-GAAP gross margins expected at 75.0%, plus or minus 50 basis points.

Those metrics also separate durable demand from a looser capex narrative. Cloud spending can remain high while investors still question whether it becomes Nvidia revenue at the same margin rate. That is why Blackwell supply visibility, customer breadth and gross-margin commentary may matter more than another statement that AI demand is strong.

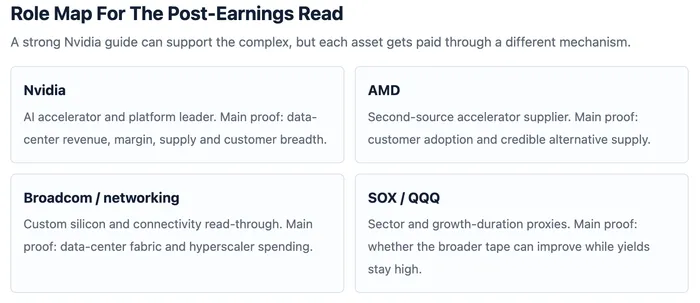

The AI Tape Needs A Role Map, Not A Ticker List

Nvidia is the platform leader and the cleanest single-stock read on AI accelerator demand, but the sector is not one trade. AMD is closer to the second-source accelerator role. Broadcom and networking names carry a different exposure around custom silicon, connectivity and the data-center fabric. SOX is the semiconductor proxy, while is the broader Nasdaq-100 growth-duration proxy.

Role separation matters after a rates shock. GPU supply, second-source adoption, custom silicon, networking demand and index duration do not have identical earnings sensitivity. The post-report tape should therefore be read by function: which parts of the AI chain get a real earnings revision, and which parts are only getting sentiment support from Nvidia's scale.

Customer Breadth Is The Quiet Risk Behind A Strong Guide

Demand visibility can remain high and still face a concentration question. In its fiscal 2026 Form 10-K, Nvidia reported that one customer accounted for 26% of total revenue and another for 13%. That does not weaken the AI demand case by itself, but it raises the value of management commentary on whether demand is broadening beyond the largest buyers.

The valuation risk is subtler than a simple demand slowdown. A report can beat expectations and still disappoint if investors decide the next dollar of revenue is too dependent on a narrow group of cloud customers, if gross-margin guidance slips, or if China restrictions continue to cap contribution. In that case, the issue would not be whether AI spending exists. It would be whether the market has already priced too much of that spending into one stock and its closest proxies.

The Report Needs A Clean Confirmation Sequence

A constructive sequence would be specific: a data-center guide that raises the revenue path, gross margin that stays near Nvidia's prior 75.0% framework, supply commentary that links Blackwell availability to shipments, and a SOX reaction that improves even if the 10-year yield remains elevated.

- Confirming signal: stronger forward data-center guide, stable gross-margin language and broader customer commentary.

- Giveback signal: in-line guide, margin pressure, narrow customer concentration, China drag or fading SOX reaction while yields stay high.

- Market signal: Nvidia and SOX outperforming Nasdaq despite the higher 10-year yield would show earnings revisions still carrying the trade.

A weaker sequence would turn the report from an AI-demand event into a valuation-burden event. The bond market does not need to disprove AI for that outcome to matter. It only has to make the earnings bar higher than the next guide can clear.