Nvidia (NASDAQ: NVDA) reports fiscal first-quarter earnings Wednesday after the close, and the setup around the report feels almost absurd in scale. The company is now worth more than the GDP of nearly every nation on Earth outside of the United States and China, turning Nvidia from a semiconductor company into something closer to a global economic force. The AI boom has effectively placed CEO Jensen Huang at the center of the modern tech arms race, with hyperscalers, sovereign governments, startups, and enterprise customers all fighting for compute power. Investors are no longer debating whether Nvidia is winning AI. The debate now centers on how long the company can maintain this level of dominance, whether competitors or custom silicon can slow it down, and how much larger a company already worth roughly $5 trillion can realistically become.

Wall Street expects another monster quarter. Consensus estimates call for revenue of roughly $79 billion, representing around 80% year-over-year growth, while adjusted earnings per share are expected around $1.78 to $1.81. Data center revenue, which has become the heartbeat of the AI infrastructure trade, is expected to come in near $73 billion. Importantly, investors are not simply looking for Nvidia to beat those numbers. Nvidia has conditioned the market to expect significant upside. Several firms, including Morgan Stanley, UBS, and Wells Fargo, believe the company could once again deliver its familiar “beat-and-raise” pattern, potentially topping revenue expectations by $3 billion or more while guiding the July quarter above consensus.

The biggest driver remains hyperscaler spending. Amazon, Alphabet, Microsoft, and Meta are projected to spend nearly $700 billion combined on AI infrastructure in 2026, up dramatically from estimates earlier this year. Nvidia remains the primary beneficiary of that spending cycle. Analysts at RBC noted that AI compute demand continues to outpace supply, with visibility now stretching well into 2027. Morgan Stanley reiterated Nvidia as its top semiconductor pick ahead of earnings, arguing that the market has become overly focused on secondary AI beneficiaries while underestimating the staying power of Nvidia’s dominance in accelerated computing.

Much of the attention on this report will revolve around the transition from Blackwell to Rubin. Blackwell demand remains extremely strong, but investors increasingly want clarity on how quickly Rubin production ramps and whether Nvidia can sustain its pricing power into the next architecture cycle. UBS said Rubin chip production appears on track this quarter, although rack-level cooling adjustments may slightly delay broader production into the September or October timeframe. KeyBanc expects Rubin to contribute an initial $3 billion to $4 billion in revenue guidance, while also forecasting Rubin GPU shipments could reach 1.7 million to 1.8 million units this year.

CFRA analyst Angelo Zino believes Rubin could represent the next major evolution for Nvidia as the AI industry shifts toward agentic AI. In an interview ahead of earnings with AINvest's Adam Shapiro, Zino said Rubin is “extremely important” because Nvidia is expanding beyond GPUs into broader compute and networking opportunities. According to Zino, Nvidia’s integration of Groq LPUs and its growing CPU strategy could create additional content growth opportunities outside traditional GPUs, particularly as AI agents require increasingly complex infrastructure. Zino also highlighted networking as a major opportunity, arguing that Nvidia’s growth trajectory increasingly depends on broader AI system architecture rather than GPUs alone.

China remains one of the largest uncertainties surrounding the stock. Nvidia’s guidance previously assumed essentially zero contribution from China data center compute revenue, even as the Trump administration has reportedly approved limited H200 shipments to select Chinese firms including Alibaba, Tencent, and ByteDance. The problem is that approvals have not translated into actual shipments. Reuters reported that no H200 deliveries have occurred so far, leaving investors uncertain about how much of the China opportunity is real versus theoretical.

The longer-term concern is that China is rapidly developing domestic alternatives. Huawei now reportedly controls approximately 41% of China’s AI chip market, while Nvidia’s share has fallen significantly from prior peak levels. Several analysts believe Nvidia eventually regains traction in China because developers still overwhelmingly prefer Nvidia’s ecosystem and CUDA software stack. However, others increasingly view China as “out of the numbers” entirely. DADA explicitly told investors to “forget China” for now, arguing that Nvidia’s growth story no longer depends on that market.

Margins will also be closely watched. Nvidia’s gross margins have remained astonishingly resilient despite rising memory costs and enormous production complexity tied to Blackwell systems. Analysts broadly expect gross margins to remain in the mid-70% range. RBC specifically said management is likely to maintain its mid-70% gross margin outlook even amid higher HBM memory pricing. CFRA’s Angelo Zino said investors should focus on whether Nvidia can sustain approximately 75% gross margins over the next several quarters as Rubin ramps and component costs increase.

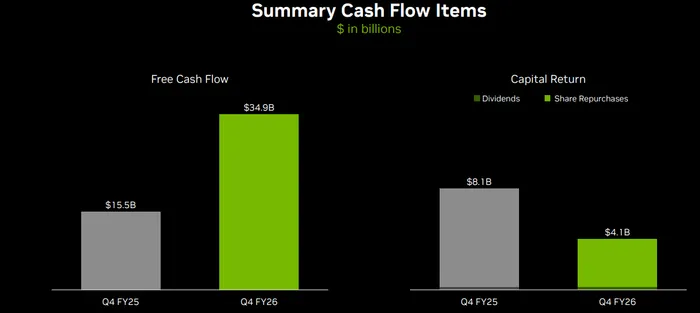

Free cash flow generation has become another critical pillar of the bull case. Zino noted that Nvidia could generate more than $400 billion in combined free cash flow over the next two years, which fundamentally changes how investors should view the valuation. Rather than focusing on the company’s enormous market capitalization, bulls increasingly frame Nvidia as a cash flow machine trading at a surprisingly reasonable earnings multiple relative to its growth rate. Nvidia currently trades around 20-24 times forward earnings estimates depending on the forecast used, which is actually below historical levels and near or even below parts of the broader semiconductor sector.

Capital return could emerge as a surprise catalyst. UBS believes Nvidia could announce a share repurchase authorization approaching $150 billion over the next 12 months. Cantor Fitzgerald also pointed toward potential multi-year buyback commitments similar to Apple’s massive capital return strategy from the prior decade. Investors increasingly view buybacks as important because Nvidia’s free cash flow profile is becoming so large that the company may struggle to deploy all of it organically.

Valuation remains one of the most fascinating aspects of the Nvidia story. The company’s market capitalization sounds extreme, yet many analysts still argue the stock is relatively cheap given the growth trajectory. CFRA’s Angelo Zino said Nvidia trades around 20 times CFRA’s 2027 estimates, which he believes remains compelling relative to both historical valuation levels and other semiconductor names that have already experienced significant rerating rallies. Zino added that Nvidia may actually offer a better risk-reward profile than many secondary AI beneficiaries after the recent semiconductor rally.

Price targets continue moving higher across Wall Street. Cantor Fitzgerald recently raised its target to $350, Bank of America boosted its target to $320, Wells Fargo increased its target to $315, and several firms continue describing Nvidia as their top semiconductor pick. The argument from bulls is increasingly straightforward: AI demand is not slowing, hyperscaler spending continues accelerating, networking and inference workloads are becoming major incremental growth drivers, and Nvidia still owns the dominant software ecosystem.

Still, expectations remain extraordinarily high. Nvidia is no longer simply required to beat estimates. It must reassure investors that AI spending remains durable, that Rubin production stays on schedule, that margins remain stable, and that competition from custom ASICs and rival accelerators remains manageable. In many ways, Nvidia earnings have become less about semiconductors and more about the health of the entire AI trade. Wednesday’s report will likely determine whether investors continue treating Nvidia as the undisputed king of AI infrastructure — or whether cracks finally begin appearing in one of the most dominant growth stories Wall Street has ever seen.